Abstract

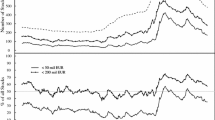

Over the last 25 years there have been numerous studies that have identified various market anomalies, many of which have given rise to a new quantitative investment strategy. This paper concentrates on the two most prolific of these strategies: value investing and momentum investing, whose performance is evaluated in the major European markets over the intersesting period from January 1990 to June 2002. The first decade of the sample period was characterised by a consistently rising market, with the European markets rising on average by 12.5 per cent per annum but this period was followed by a rapid (still on-going) market correction, with the European markets falling on average by 12 per cent per annum over the first two and a half years of the new millennium.1

Access this chapter

Tax calculation will be finalised at checkout

Purchases are for personal use only

Preview

Unable to display preview. Download preview PDF.

Similar content being viewed by others

References

Arshanapalli, B., Coggin, T. and Doukas, J. (1998) ‘Multifactor Asset Pricing Analysis of International Value Investment Strategies’, The Journal of Portfolio Management, 24, 4.

Bachelier, L. (1900) ‘Theory of Speculation’, reprinted in The Random Character of Stock Market Prices, P. Cootner (Ed.), (1964), MIT Press, Cambridge, MA.

Ball, R. and Brown, P. (1968) ‘An empirical evaluation of accounting income numbers’, Journal of Accounting Research, 6, 2.

Basu, S. (1977) ‘Investment Performance of Common Stocks in Relation to Their Price Earnings Ratios: A Test of the Efficient Market Hypothesis’, Journal of Pinance, 32, 3.

Bernard, V., Thomas, J. and Wahlen, J. (1997) ‘Accounting-based Stock Price Anomalies: Separating Market Inefficiencies From Risk’, Contemporary Accounting Research, 14, 2.

Bird, R. and Gerlach, R. (2003) A Bayesian Approach to Enhancing a Value Strategy: Evidence from the US, UK and Australia, UTS Working Paper.

Chan, L., Hamao, Y. and Lakonishok, J. (1991) ‘Fundamentals and Stock Returns in Japan’, Journal of Finance, 46, 5.

Chan, L., Jegadeesh N. and Lakonishok, J. (1996) ‘Momentum Strategies’, Journal of Finance, December, 51, 5.

Chopra, N, Lakonishok, J. and Ritter, J. (1992) ‘Measuring Abnormal Performance: Do Stocks Overreact?’ Journal of Financial Economics, 31, 2.

DeBondt, W. and Thaler, R. (1985) ‘Does the Stock Market Overreact?’ Journal of Finance, 40, 3.

DeBondt, W. and Thaler, R. (1987) ‘Further Evidence on Investor Overreaction and Stock Market Seasonality’ Journal of Finance, 42, 3.

Dreman, D. and Berry, M.A. (1995) ‘Analysts’ Forecasting Errors and Their Implications lor Security Analysis’, Financial Analysts Journal, May-June, 51, 3.

Elton, E., Gruber, M., Brown, S. and Goetzman, W. (2003) Modern Portfolio Theory and Investment Analysis, 6th edition, John Wiley & Sons, New York.

Farma, E. (1998) ‘Market Efficiency Long-Term Returns and Behavioral Finance’, Journal of Financial Economics, 39, 3.

Fama, E. and French, K. (1993) ‘Common Risk Factors in the Returns on Stocks and Bonds,’ Journal of Financial Economics, 33, 1.

Givoly D. and Lakinishok, J. (1979) ‘The Information Content of Financial Analysts’ Forecasts of Earnings’, Journal of Accounting and Economics, 1, 3.

Graham, B. and Dodd, D. (1934) Security Analysis, McGraw Hill, New York.

Grundy, B. and Martin, S. (2001) ‘Understanding the Nature of the Risks and the Source of Rewards to Momentum Investing’, Review of Financial Studies, 14, 1.

Jegadeesh, N. and Titman, S. (1993) ‘Returns to Buying Winners and Losers: Implications for Stock Market Efficiency’, Journal of Finance, 48, 1.

Jegadeesh, N. and Titman, S. (2001) ‘Profitability of Momentum Strategies: An Evaluation of Alternative Explanations’, Journal of Finance, 56, 2.

Kadiyala, P. and Rau, P. (2001) It’s All Under-Reaction, Purdue University Working Paper.

Lakonishok, J., Shleiler, A. and Vihny, R. (1994) ‘Contrarian Investment, Extrapolation and Risk,’ Journal of Finance, 49, 5.

La Porta, R., Lakonishok, J., Shleifer, A. and Vishny, R. (1997) ‘Good News for Value Stocks: Further Evidence on Market Efficiency’, Journal of Finance, 52, 2.

Newey, W. and West, N. (1987) ‘A Simple Positive Semi-Definite, Heteroskedasticity and Autocorrelation Consistent Covariance Matrix’, Econometrica, 55, 3.

Richardson, S., Teoh, S. and Wysocki, P. (2002) ‘The Walkdown to Beatable Analyst Forecasts: The Role of Equity Issuance and Inside Trading Incentives’, University of Pennsylvania Working Paper.

Rosenberg, B., Reid, K. and Lanstein, R. (1985) ‘Persuasive Evidence of Market Inefficiency’, Journal of Portfolio Management, 11, 3.

Rouwenhorst, K. (1998) ‘International Momentum Strategies’, Journal of Finance, 53, 1.

Rouwenhorst, K. (1999) ‘Local Return Factors and Turnover in Emerging Markets’, Journal of Finance, 54, 4.

Softer, L. and Walther, B. (2000) Return Momentum, Return Reversals and Earnings Surprise, Northwestern Graduate School of Management Working Paper.

Author information

Authors and Affiliations

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2016 The Editor(s)

About this chapter

Cite this chapter

Bird, R., Whitaker, J. (2016). The Performance of Value and Momentum Investment Portfolios: Recent Experience in the Major European Markets. In: Satchell, S. (eds) Asset Management. Palgrave Macmillan, Cham. https://doi.org/10.1007/978-3-319-30794-7_7

Download citation

DOI: https://doi.org/10.1007/978-3-319-30794-7_7

Publisher Name: Palgrave Macmillan, Cham

Print ISBN: 978-3-319-30793-0

Online ISBN: 978-3-319-30794-7

eBook Packages: Economics and FinanceEconomics and Finance (R0)