Abstract

Today, we are in the midst of an undesirable mix of tight economic and financial conditions. Opaque derivative products which include among others Collateralized-Debt-Obligations and Exchange-Traded Funds continue to shape the markets. Economists need to rethink certain economic concepts and relationships. Actually, fiscal stimulus spending is not stimulating anything. The deadly embrace between over-indebted sovereigns and over-leveraged banks has created a vicious cycle. Faced with these new economic and financial market imbalances, portfolio management has become much more difficult. We need to arm ourselves with how to manage tail risks against the inevitable and recurring loss of confidence which comes from market instability. We must adapt continuously along with the market whatever the pressure. Acknowledging errors and adjusting to them is crucial. Understanding market events and their effects on the market system is an essential element toward building a financial warning system. To this end, we need to identify all pre-switching points; implement them in algorithms that can trigger a warning signal. If we think of Keynes levels, the sixth level would be to have a drummer like mind … to be ahead of the beat. In the end what we achieve by understanding markets’ fractality is more than a tool; it is a way of thinking.

Access this chapter

Tax calculation will be finalised at checkout

Purchases are for personal use only

Notes

- 1.

Brokerage firms encourage this type of aggressive management because they significantly increase the volume of daily transactions and consequently, their fees.

- 2.

This is similar to the purchase of a put except that CDS are bilateral contracts.

- 3.

The amount of the premiums (or spreads) paid to a given issuer gives an indication of the market appreciation and the quality of this issuer.

- 4.

iShares began recently in 2011 to publish a detailed quarterly report outlining all its ETFs’ securities lending activities.

- 5.

Especially european regulations. In the USA, the US 1940 Investment Act, require an ETF to own the constituent assets of the index it is tracking to be classified as a fund.

- 6.

Same principle applies in religion: religious laws have to be taken as general guiding rules but should not ordinarily intrude in an individuals’ daily life. Once a society reaches the level of detailed governmental guidance, it is on its way to servitude and can then be easily manipulated into extremism.

- 7.

Questions persist regarding governments’ ability to control financial activities given the difficulties of evaluating and accounting for complex derivative products or illiquid assets.

- 8.

Some activities cannot be regulated by the market place as they can cause damage to third parties or negative economic outcomes known as negative externalities.

- 9.

Jerome L. Stein’s paper on Stochastic Optimal Control (SOC) (Stein, 2010) Analysis focused on the question: What is an optimal debt or leverage that maximizes the expected growth of net worth and is based upon significant risk aversion? The Stochastic Optimal Control Analysis provides another tool of analysis and derives the time varying optimal debt ratio.

-

1.

The optimum debt ratio or leverage maximizes the expected growth of net worth.

-

2.

As the debt ratio rises above the optimum, the expected growth of net worth declines and the risk rises.

-

3.

The probability of a crisis is positively related to excess debt, equal to the difference between the actual and optimal debt ratio, measured in standard deviations.

-

4.

An unambiguous early warning signal (EWS) of a debt crisis would be that the leverage f(t) = L(t)/X(t) exceeds f-max, so that the expected growth of net worth is negative and the risk is high.

-

1.

- 10.

Since the beginning of the mortgage crisis in 2007, Central banks have injected liquidity (through bank loans, at very short terms), in vain.

- 11.

These agencies have, since 2000, lightened their rating criteria and modified their evaluation models.

- 12.

This pertains to the greed of portfolio managers and all other control cells (such as the case of Kerviel of the Société Générale bank and many other management platforms who registered heavy losses from the failure of risk follow-up either at the level of internal information procedures or of calculations). It should also be noted that the investments in internal technology systems and platforms in financial institutions have not been sufficient.

- 13.

During the real estate boom, debtors refinanced their mortgages under the best of conditions given the over-valuing of their mortgages, or sold at inflated prices. This was no longer possible after the bursting of the real estate bubble.

- 14.

In the process, however, these nations forgot about other companies in need.

- 15.

In 1990, Sweden nationalized several banks and created a “bad bank” which bought toxic assets after discount, leaving the financial institutions to manage their more liquid assets.

Author information

Authors and Affiliations

Corresponding author

Appendix D: 2007 Meltdown (Hayek 2010)

Appendix D: 2007 Meltdown (Hayek 2010)

In the following, we will see how the greed of financial agents, the pure laissez faire of authorities regarding leverage and their inability to understand complex financial operations and the indifference of the masses, combined to bring about the financial meltdown of 2007, the effects of which continued to be felt across the globe at the time of this book going to press.

The bankruptcies seen in 2008 were only a symptom of the difficulties that business banks had been dealing with since 2007. These signals, largely ignored or camouflaged by the financial communityFootnote 10, were comprised of the following:

-

Monetary and leverage laxity;

-

A surge in toxic assets which arose from real estate loans given to households with modest incomes;

-

unfaithful rating agencies, apparently concerned only with increasing their profitability and consequently losing their objectivityFootnote 11; and

-

deficient risk management systems, based on the neoclassical school of thought that proposes easy but ineffective methods of forecasting risks.Footnote 12 Specifically in the case of CDOs; these were based on Li’s Gaussian copula function put forward in early 2000 which assumed that correlation was a single constant number. Rating agencies and banks grabbed the opportunity and shaped their assessments based on this function. While the formula was new and complicated for non-mathematicians, banks were happy to classify their products according to this single risk measure and as such sell their CDO products without much effort. It is impossible for professionals at the time not to have been aware of the danger of this function’s limitation as correlation cannot be stable over time.

When the subprime mortgage loan bubble burst, it led to a banking crisis. As of January 2010, defaults on mortgages that had been given to the least credit-worthy borrowers drove financial institutions worldwide to undertake $1.8 trillion in write downs and losses. The following section outlines the significant events during the 2007–2009 market crash.

2007

-

5 March: First signs that the speculative real estate bubble had burst was seen at HSBC, the largest European bank in terms of equity market price, which declared large losses in the U.S. mortgage credit market following repayment defaults.

-

2 April: New Century Financial Corporation declared bankruptcy; they were the second largest U.S. subprime lenders, specializing in providing credit to the most disadvantaged.

-

17 July: Investment bank Bear Stearns Companies, Inc. announced the failure of two of its speculative subprime funds.

-

19 July: The Governor of the U.S. Federal Reserve, Ben S. Bernanke, announced in front of the U.S. Senate that losses arising from subprime products were close to $100 billion.

-

9 August: French bank BNP Paribas announced the freezing of three of its investment funds exposed to the subprime market as the bank was no longer able to evaluate them. The equity markets fell and several days later, the U.S. Federal Reserve lowered key interest rates.

-

14 September: The Bank of England provides an emergency loan to Northern Rock Plc to prevent its bankruptcy.

-

October: UBS and Citigroup announced they had been affected by the crisis. American International Group (AIG), the largest global insurer, announced that it was in great difficulty and that it could no longer cover its obligation to guarantee credit defaults. It had sold $441 billion of unsecured coverage without enough reserves.

2008

During the first half of 2008, financial agents speculated on raw materials, penalizing companies and consumers. In the U.S., the increase in interest rates from only 1 % in 2004 to 5.25 % in 2008 and the progressive decrease in real estate prices placed many individuals in difficult times as they were no longer able to repay their loans.Footnote 13

-

16 March: Under pressure from the U.S. government, JP Morgan Chase bought Bear Stearns Companies, Inc.

-

12 August: UBS AG, the largest Swiss bank, experiences massive withdrawals of deposits. The bank then announced its plan to separate its investment entity from its portfolio or wealth management entity.

-

July and August: The equity market prices of Freddie Mac and of Fannie Mae, two U.S. quasi-government mortgage refinancing firms, collapsed.

-

7 September: The U.S. Treasury guaranteed the debts of Freddie Mac and Fannie Mae up to $100 billion.

-

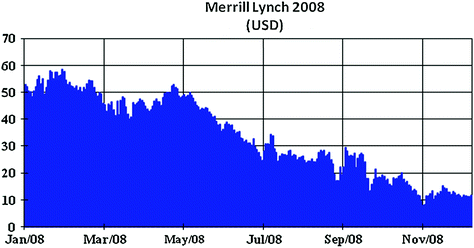

15 September: Lehman Brothers, the fourth largest U.S. investment bank, went bankrupt, while Merrill Lynch (Fig. 6.1) was purchased by Bank of America to avoid bankruptcy.

Fig. 6.1

Merrill Lynch stock price falls from $50 to $10 in 2008 (Source Bloomberg)

-

16 September: AIG was rescued by the U.S. government who granted it $85 billion in assistance in exchange for 80 % of their capital.

Table 6.1 shows the collapse in equity prices of some financial companies between January 2007 and 2009. Globally, central banks reacted by lowering their key rates and injecting liquidity in an attempt to revive the credit market.

-

End of September: Bankruptcy risks spread to Europe. Fortis, Dexia, and l’Hypo Real Estate were among the affected banks.

-

October: The US Federal Reserve accepted to exchange risky securities from banks for liquidity. A U.S. rescue plan named the Troubled Asset Relief Program (TARP) was put into place.

During the course of the rest of the year, the equity markets around the world continued to collapse; Iceland declared bankruptcy; the ruble was devalued; the IMF granted huge loans to Pakistan; Great Britain announced a rescue plan for banks in the amount of GBP 250 billion which was further increased by GBP 100 billion in January 2009. The G-7 committed to help to prevent any bank from going bankrupt, while large EU countries developed national rescue plans worth EUR1.7 trillion to refinance banksFootnote 14.

Despite all the help that they received, banks remained cautious with regard to extending credit lines. As such, central banks picked up the slack by lending at longer terms (such as, for instance, up to 6 months instead of the usual three) and accepting non-liquid and badly-valued assets as security. In the end, central banks found themselves with “bad” assets, in a market where in the words of Michel Aglietta:

…capitalism functions as usual, a privatization of profits and a socialization of losses (Michel Aglietta 2008).

Some countries considered the possibility of guaranteeing all interbank loans, while others such as France opted to create a refinancing bank that would lend to the banks on the markets, guaranteed by the state, for long durations between 1 and 5 years, while using wide margins of credit as a collateral. Other countries such as the U.S. repurchased commercial bills from companies for their daily operations in order to fulfill their operating funding needs. These measures, however, did not prevent equity prices from deteriorating and liquidity from staying frozen. In 2008, the world equity market capitalization was reduced by 50 % from US$60 to US$30 trillion Fig. 6.2.

World capitalization (Source Bloomberg)

Financial companies lost more than US$1 trillion in the credit market following the burst of the subprime bubble (Table 6.2).

Equity markets got into a spiral dominated by the short-term and distorted by the weight of the number of players, specificity of computer programs and margin calls. Figure 6.1 shows how volatility reached new highs during the crisis Fig. 6.3 .

SPX volatility index (VIX) (Source Bloomberg)

2009

Companies with enormous needs for operating capital such as General Motors went bankrupt. Meanwhile, individual consumers’ financial situations were also deteriorating, as evidenced by high default rates on credit card payments.

-

January 2009: the assimilation of information in prices was high. The market enters a bear phase where economic data was immediately taken into consideration. The system was moving toward its economic attractor. While the economic indicators remained pessimistic and uncertain, the market remained in a bearish consolidation where severe declines were registered and rebounds were confined within a technical margin of consolidation. Trading strategies inside the bear channel were very profitable because the rebounds that followed after several days of decline were often large and vice versa. In short, the gambler’s fallacy approach during this time was profitable. Market players wondered whether they were entering into a depression phase and whether they would suffer a fate similar to or worse than that of Japan or the Scandinavian countries in the 1990s.Footnote 15 At the beginning of 2009, the hedge fund industry, much like the banking industry, knew it had a lot of work to do to regain investors’ confidence, following the large losses of the majority of funds’ fraud cases such as the Ponzi scheme of Bernie Madoff and the restrictions imposed to prevent withdrawals by investors in 2008.

-

March 2009: Government injections of liquidity reached US$1.6 trillion in September 2009 and signs indicating that a depression had been avoided led to a surge in equity prices. Still, the rate of unemployment in the U.S. and E.U. was 9.5 %, compared to 18.5 % in Spain. In a deflationary environment with USD LIBOR close to 0 %, it was absolutely necessary for the bullish trend to be validated by new market data, lest the market put itself at risk again with another crisis. Indeed, the enormous injections of liquidity had allowed us to avoid a worldwide economic depression, but the economic recovery was slow and without vigor. Until employment figures return to normal, the world economy will remain stagnant and governments vulnerable to social disturbances. In September 2009, the GNP for the U.S., E.U., China, and India were −3.90,−4.70, 7.90, and 6.10 %, respectively. During this period, governments had to deal with enormous budgetary deficits; and with the level of interest rates as low as they were, governments no longer had any tangible means for rescuing markets.

-

Between March and October 2009, the S&P500 and EUROSTOXX600 indices increased by 51 and 48 %, respectively, on the back of signs of economic rebounds including the return of consumer confidence and stabilization of real estate prices. The market, however, was still plagued with uncertainty regarding how the market deals with this euphoria; the outlook for the coming months; and how forecasts are affected by the newly-established rules and laws that were exogenous or endogenous to the system. Due to these remaining uncertainties, some governments went so far as to forbid the short-selling of some classes of shares to control speculation which prejudiced funds that use coverage strategies.

Rights and permissions

Copyright information

© 2013 The Author(s)

About this chapter

Cite this chapter

Hayek Kobeissi, Y. (2013). The Latest “Normal”. In: Multifractal Financial Markets. SpringerBriefs in Finance. Springer, New York, NY. https://doi.org/10.1007/978-1-4614-4490-9_6

Download citation

DOI: https://doi.org/10.1007/978-1-4614-4490-9_6

Published:

Publisher Name: Springer, New York, NY

Print ISBN: 978-1-4614-4489-3

Online ISBN: 978-1-4614-4490-9

eBook Packages: Business and EconomicsEconomics and Finance (R0)