Identifying and Predicting the Credit Risk of Small and Medium-Sized Enterprises in Sustainable Supply Chain Finance: Evidence from China

Abstract

:1. Introduction

2. Literature Review

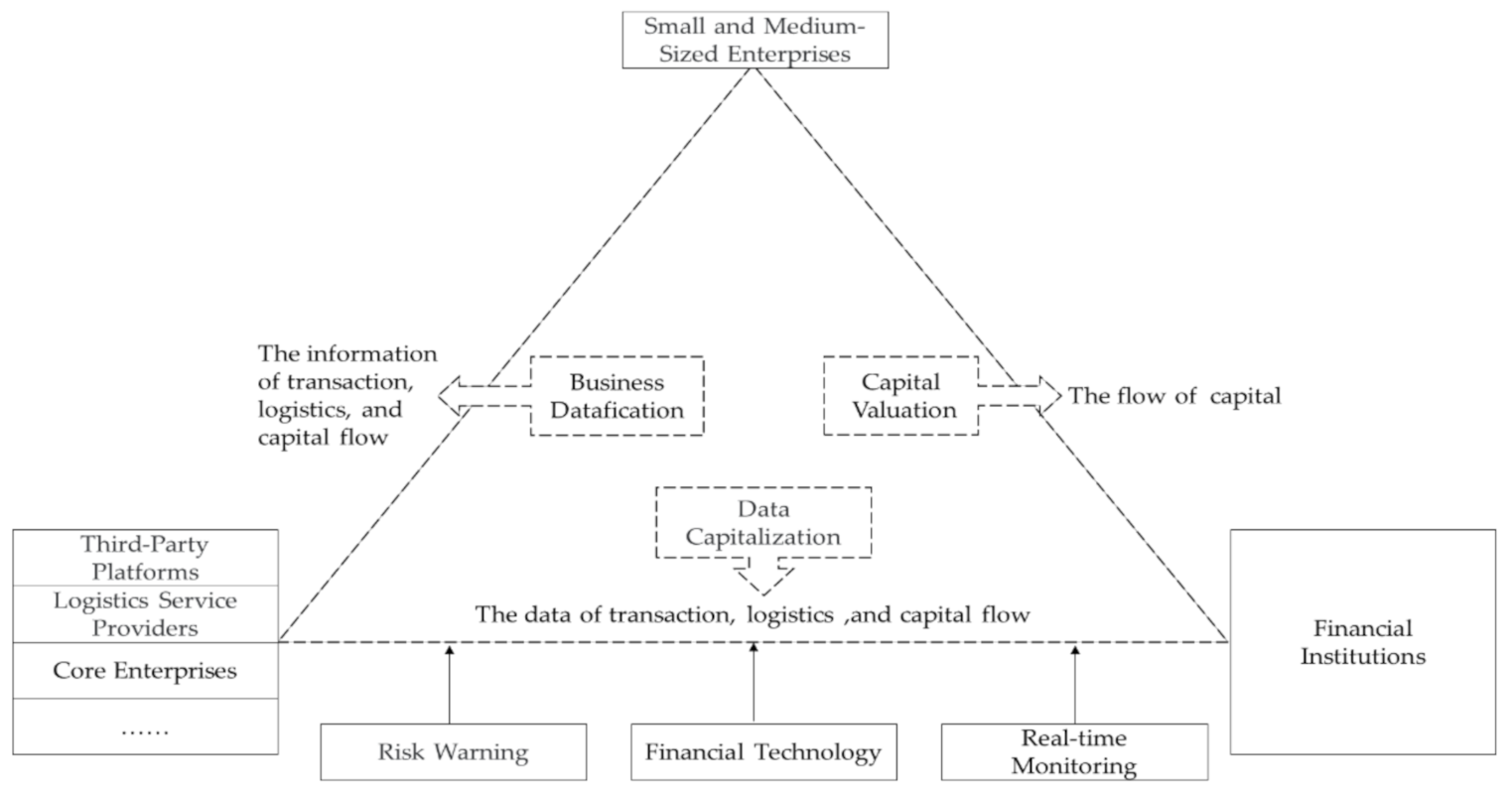

2.1. Sustainable Supply Chain Finance

2.2. Influencing Factors and Prediction Models of Credit Risk in SCF

3. Research Methodology

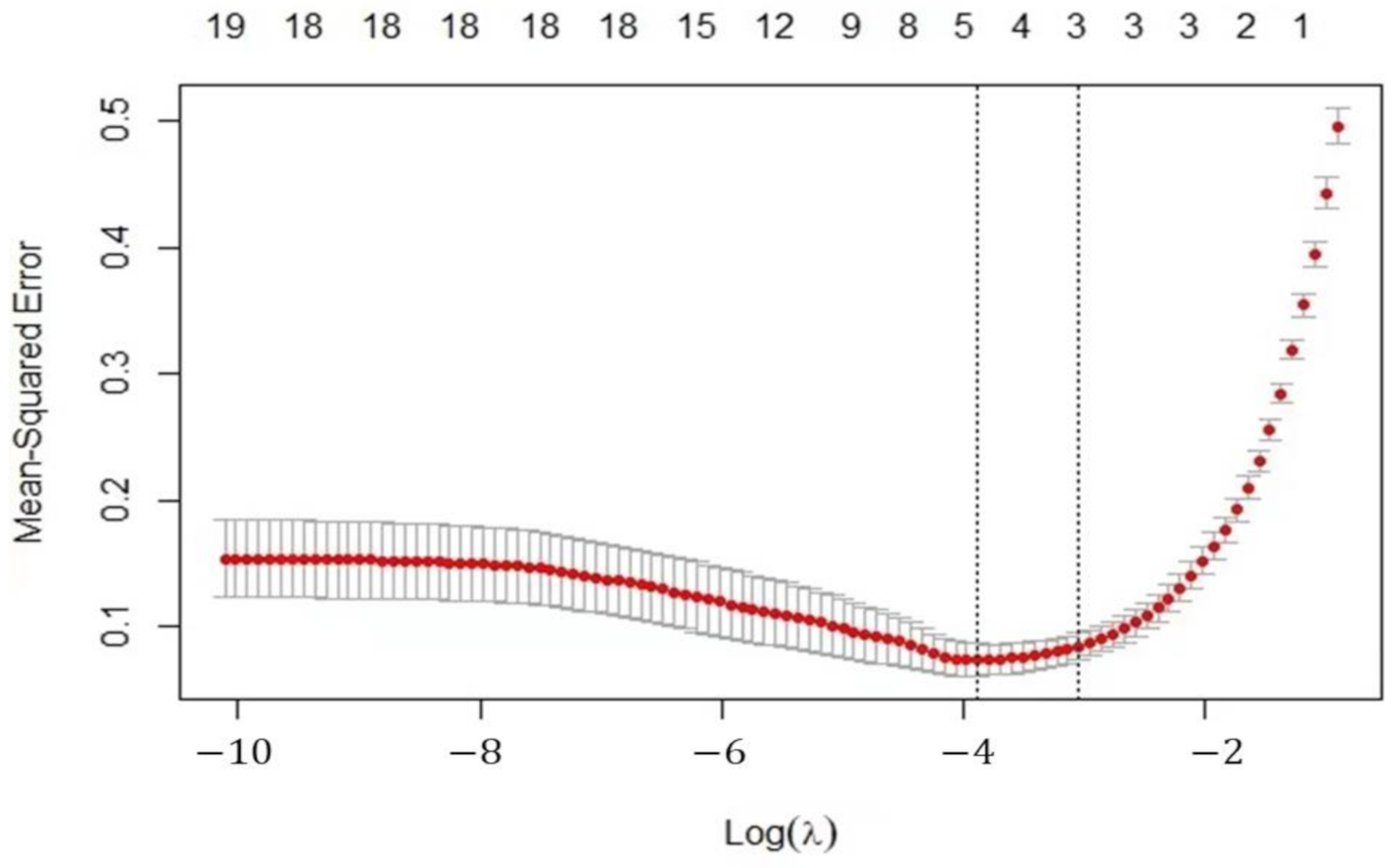

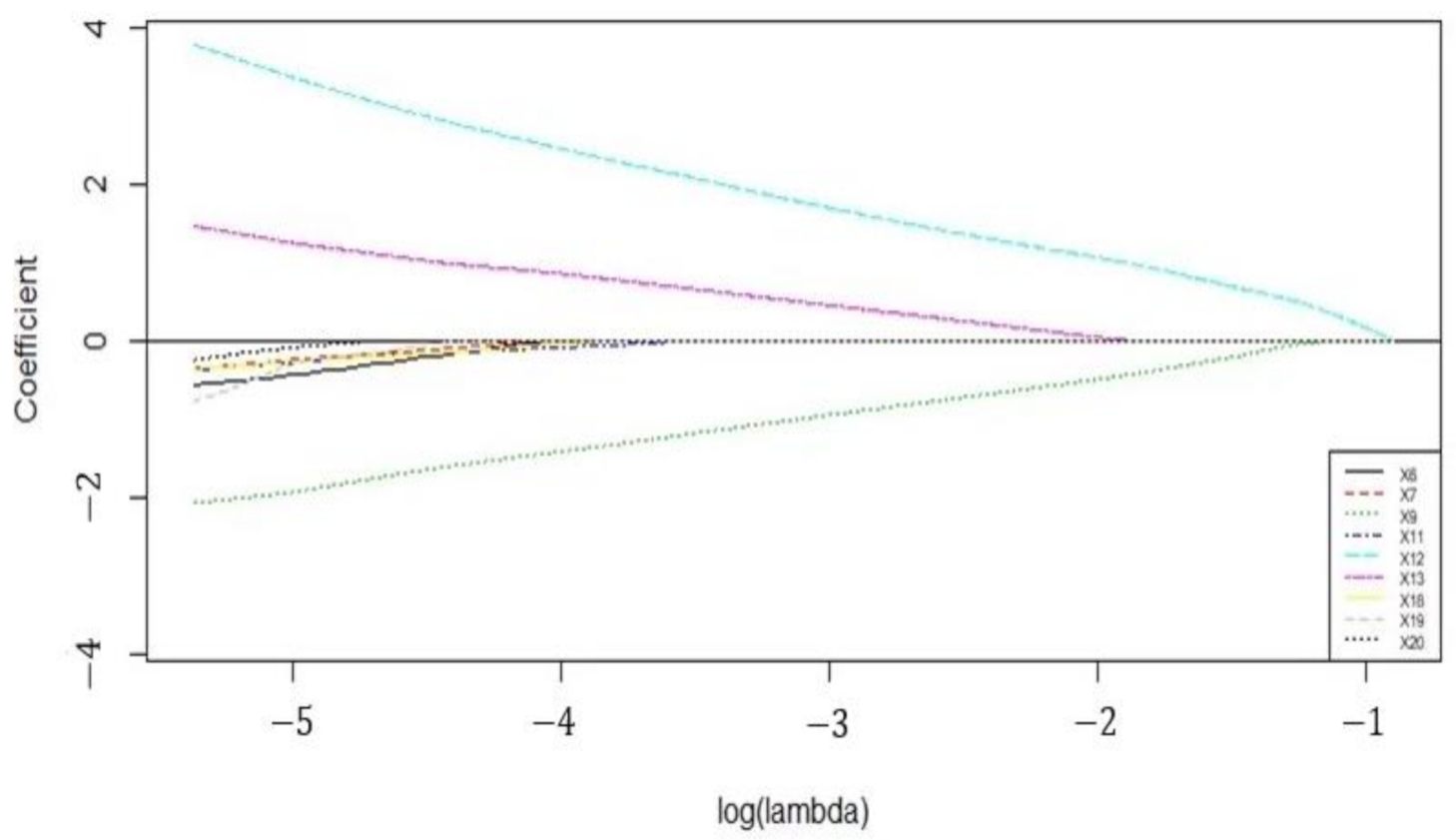

3.1. Lasso Model

3.2. Lasso-Logistic Model

3.3. Model Evaluation

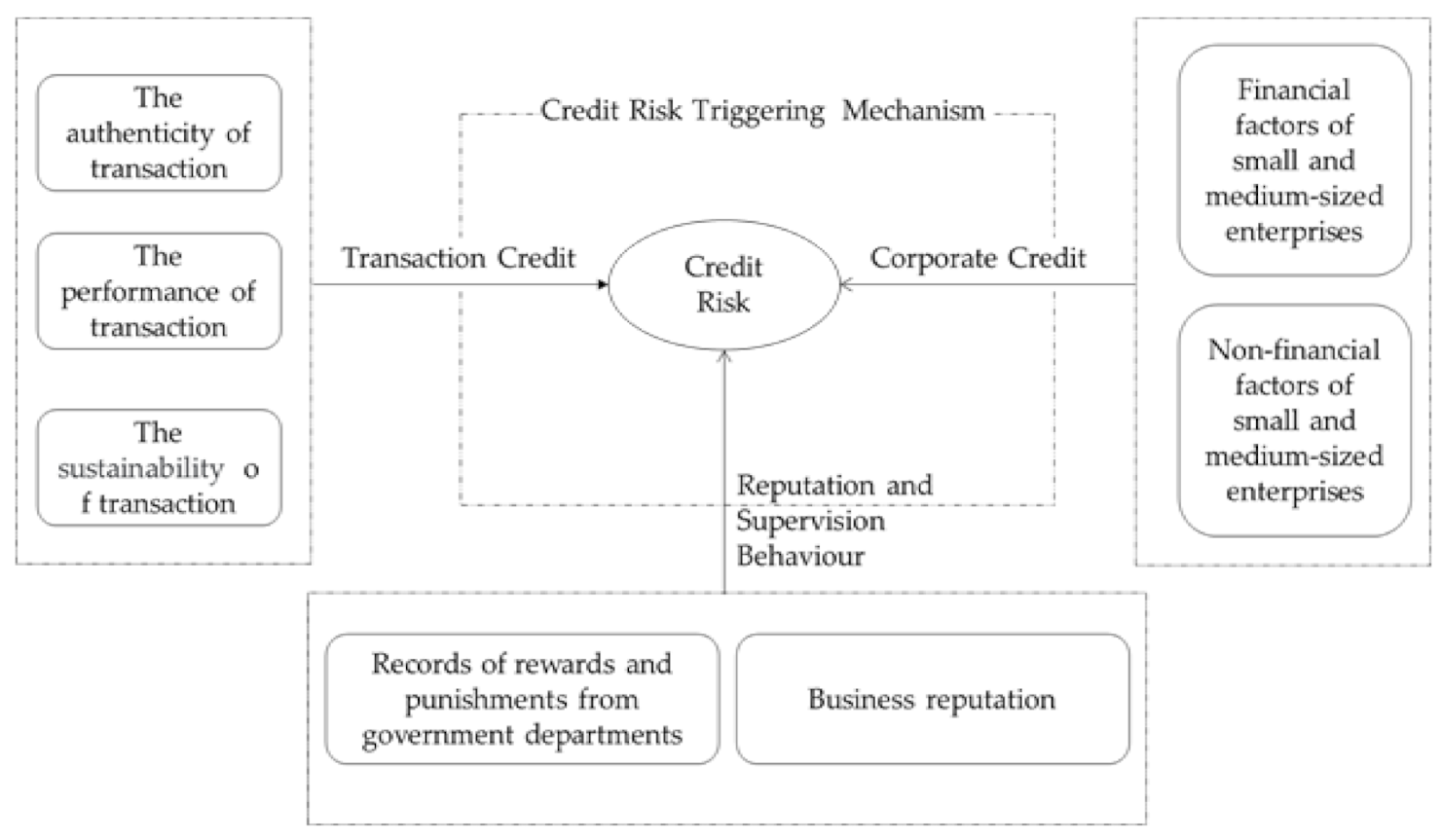

4. Credit Risk Triggering Mechanism and Variable Definition

4.1. Credit Risk Triggering Mechanism

4.2. Variable Definitions

4.3. Data Sources and Pre-Processing

5. Simulations

6. Experimental Results and Analysis

6.1. Identification of the Factors Influencing the Credit Risk of SMEs

6.2. Evaluation of the Lasso-Logistic Model

7. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Zhan, J.; Li, S.; Chen, X. The impact of financing mechanism on supply chain sustainability and efficiency. J. Clean Prod. 2018, 205, 407–418. [Google Scholar] [CrossRef]

- Zhou, Q.; Chen, X.; Li, S. Innovative financial approach for agricultural sustainability: A case study of Alibaba. Sustainability 2018, 10, 891. [Google Scholar] [CrossRef] [Green Version]

- Rajeev, A.; Pati, R.K.; Padhi, S.S.; Govindan, K. Evolution of sustainability in supply chain management: A literature review. J. Clean Prod. 2017, 162, 299–314. [Google Scholar] [CrossRef]

- Abe, M.; Troilo, M.; Batsaikhan, O. Financing small and medium enterprises in Asia and the Pacific. J. Entrep. Public Pol. 2016, 4, 2–32. [Google Scholar] [CrossRef]

- Harish, A.R.; Liu, X.L.; Zhong, R.Y.; Huang, Q.G. Log-flock: A blockchain-enabled platform for digital asset valuation and risk assessment in E-commerce logistics financing. Comput. Ind. Eng. 2021, 151, 107001. [Google Scholar] [CrossRef]

- Yan, N.; Sun, B.; Zhang, H.; Liu, C. A partial credit guarantee contract in a capital-constrained supply chain: Financing equilibrium and coordinating strategy. Int. J. Prod. Econ. 2016, 173, 122–133. [Google Scholar] [CrossRef]

- Wuttke, D.A.; Blome, C.; Heese, H.S.; Protopappa-Sieke, M. Supply chain finance: Optimal introduction and adoption decisions. Int. J. Prod. Econ. 2016, 178, 72–81. [Google Scholar] [CrossRef]

- Tseng, M.L.; Wu, K.J.; Hu, J.; Wang, C.H. Decision-making model for sustainable supply chain finance under uncertainties. Int. J. Prod. Econ. 2018, 205, 30–36. [Google Scholar] [CrossRef]

- Li, J.; Wang, Y.J.; Feng, G.Z.; Wang, S.Y.; Song, Y.G. Supply chain finance review: Current situation and future trend. Syst. Eng. Theory Pract. 2020, 40, 1977–1995. [Google Scholar]

- Mou, W.; Wong, W.K.; McAleer, M. Financial credit risk evaluation based on core enterprise supply chains. Sustainability 2018, 10, 3699–3715. [Google Scholar] [CrossRef] [Green Version]

- Tao, Z.; Li, X.; Liu, X.; Feng, N. Analysis of signal game for supply chain finance (SCF) of MSEs and banks based on incomplete information model. Discret. Dyn. Nat. Soc. 2019, 2019, 1–6. [Google Scholar] [CrossRef]

- Chen, X.; Liu, C.; Shuting, L. The role of supply chain finance in improving the competitive advantage of online retailing enterprises. Electron. Commer. Res. Appl. 2019, 33, 100821. [Google Scholar] [CrossRef]

- Yao, Z.; Hu, M.; Ye, M. Research on the mechanism of social network promoting financing availability of small and micro enterprises. Manag. World. 2013, 4, 135–147. [Google Scholar]

- Glover, J.L.; Champion, D.; Daniels, K.J.; Dainty, A.J.D. An institutional theory perspective on sustainable practices across the dairy supply chain. Int. J. Prod. Econ. 2014, 152, 102–111. [Google Scholar] [CrossRef] [Green Version]

- Zhao, Z.; Chen, D.; Wang, L.; Han, C. Credit risk diffusion in supply chain finance: A complex networks perspective. Sustainability 2018, 10, 4608. [Google Scholar] [CrossRef] [Green Version]

- Zhu, Y.; Xie, C.; Sun, B.; Wang, G.; Yan, X. Predicting China’s SME credit risk in supply chain financing by logistic regression. Artificial neural network and hybrid models. Sustainability 2016, 8, 433. [Google Scholar] [CrossRef] [Green Version]

- Song, H. The development trend of China’s supply chain finance. China Bus. Mark. 2020, 33, 3–9. [Google Scholar]

- Wu, X.; Liao, H. Utility-based hybrid fuzzy axiomatic design and its application in supply chain finance decision making with credit risk assessments. Comput. Ind. 2020, 114, 103144. [Google Scholar]

- Gelsomino, L.M.; Mangiaracina, R.; Perego, A.; Tumino, A. Supply chain finance: A literature review. Int. J. Phys. Distrib. Logist. Manag. 2016, 46, 348–366. [Google Scholar] [CrossRef]

- Camerinelli, E. Supply chain finance. J. Paym. Str. Syst. 2009, 3, 114–128. [Google Scholar]

- Hofmann, E. Supply chain finance: Some conceptual insights. Logist. Manag. 2005, 1, 203–214. [Google Scholar]

- Pfohl, H.C.; Gomm, M. Supply chain finance: Optimizing financial flows in supply chains. Logist. Res. 2009, 1, 149–161. [Google Scholar] [CrossRef]

- Lu, Q.; Liu, B.; Song, H. The impact of SME’s capability on its supply chain financing performance: A study based on information perspective. Nankai. Bus. Rev. 2019, 22, 122–136. [Google Scholar]

- Liu, X.; Zhou, L.; Wu, Y. Supply chain finance in China: Business innovation and theory development. Sustainability 2015, 7, 14689–14709. [Google Scholar] [CrossRef] [Green Version]

- Caniato, F.; Gelsomino, L.M.; Perego, A.; Ronchi, S. Does finance solve the supply chain financing problem? Supply Chain Manag. 2016, 21, 534–549. [Google Scholar] [CrossRef]

- Song, H.; Yu, K.; Ganguly, A.; Turson, R. Supply chain network, information sharing and SME credit quality. Ind. Manag. Data Syst. 2016, 116, 740–758. [Google Scholar] [CrossRef]

- Zhu, Y.; Zhou, L.; Xie, C.; Wang, G.V.; Nguyen, T. Forecasting SMEs’ credit risk in supply chain finance with an enhanced hybrid ensemble machine learning approach. Int. J. Prod. Econ. 2019, 211, 22–33. [Google Scholar] [CrossRef] [Green Version]

- Su, Y.; Lu, N. Simulation of game model for supply chain finance credit risk based on multi-agent. Open J. Soc. Sci. 2015, 3, 31–36. [Google Scholar] [CrossRef] [Green Version]

- Abdel-Basset, M.; Mohamed, R.; Sallam, K.; Elhoseny, M. A novel decision-making model for sustainable supply chain finance under uncertainty environment. J. Clean Prod. 2020, 269, 122324. [Google Scholar] [CrossRef]

- Bruntland, G. Our common future: UN world commission on environment and development. Environment 1987, 29, 25–29. [Google Scholar]

- Feng, J.; Yuan, B.; Li, X.; Tian, D.; Mu, W. Evaluation on risks of sustainable supply chain based on optimized BP neural networks in fresh grape industry. Comput. Electron. Agric. 2021, 183, 105988. [Google Scholar]

- Barbier, E.B. The concept of sustainable economic development. Environ. Conserv. 1987, 14, 101–110. [Google Scholar] [CrossRef]

- Liang, X.; Zhao, X.; Wang, M.; Li, Z. Small and medium-sized enterprises sustainable supply chain financing decision based on triple bottom line theory. Sustainability 2018, 10, 4242. [Google Scholar] [CrossRef] [Green Version]

- Tseng, M.L.; Lim, M.K.; Wu, K.J. Improving the benefits and costs on sustainable supply chain finance under uncertainty. Int. J. Prod. Econ. 2019, 218, 308–321. [Google Scholar] [CrossRef]

- Sung, H.C.; Ho, S.J. Supply chain finance and impacts of consumers’ sustainability awareness. N. Am. Econ. Financ. 2020, 54, 100962. [Google Scholar] [CrossRef]

- Li, X.; Zheng, X.; Liu, J. How sustainable supply chain finance affects the financing performance of SMEs—An environmental regulation perspective. Financ. Regul. Res. 2020, 3, 70–85. [Google Scholar]

- Jia, F.; Zhang, T.; Chen, L. Sustainable supply chain finance: Towards a research agenda. J. Clean Prod. 2020, 243, 118680. [Google Scholar] [CrossRef]

- Mcdermott, T.; Stainer, A.; Stainer, L. Contaminated land: Bank credit risk for small and medium size UK enterprises. Int. J. Environ. Technol. Manag. 2015, 5. [Google Scholar] [CrossRef]

- Fantazzini, D.; Figini, S. Random survival forests models for SME credit risk measurement. Methodol. Comput. Appl. Probab. 2009, 11, 29–45. [Google Scholar] [CrossRef]

- Zhang, M.; He, Y.; Zhou, Z. Study on the influence factors of high-tech enterprise credit risk: Empirical evidence from China’s listed companies. Proc. Comput. Sci. 2013, 17, 901–910. [Google Scholar] [CrossRef] [Green Version]

- Angilella, S.; Mazzù, S. The financing of innovative SMEs: A multicriteria credit rating model. Eur. J. Oper. Res. 2015, 244, 540–554. [Google Scholar] [CrossRef] [Green Version]

- Cao, Y.; Xiong, S. A sustainable financing credit rating model for China’s small- and medium-sized enterprises. Math. Probl. Eng. 2014, 2014, 1–5. [Google Scholar] [CrossRef] [Green Version]

- Xiong, X.; Ma, J.; Zhao, W.; Wang, X.; Zhang, J. Credit risk analysis of supply chain finance. Nankai Bus. Rev. 2009, 12, 92–98. [Google Scholar]

- Zhang, L.; Hu, H.; Zhang, D. A credit risk assessment model based on SVM for small and medium enterprises in supply chain finance. Financ. Innov. 2015, 1, 1–21. [Google Scholar] [CrossRef] [Green Version]

- Tang, L.; Cai, F.; Ouyang, Y. Applying a nonparametric random forest algorithm to assess the credit risk of the energy industry in China. Technol. Forecast. Soc. Chang. 2019, 144, 563–572. [Google Scholar] [CrossRef]

- Zhang, W.; Wang, C.; Zhang, Y.; Wang, J. Credit risk evaluation model with textual features from loan descriptions for P2P lending. Electron. Commer. Res. Appl. 2020, 42, 100989. [Google Scholar] [CrossRef]

- Kuang, N.; Zhang, G.; Zhang, H. Individual credit risk prediction method: Application of a lasso-logistic mode. J. Quant. Tech. Econ. 2014, 31, 125–136. [Google Scholar]

- Jiang, C.; Huang, Y.; Xu, Q. Credit evaluation of listed companies via Lasso binary quantile regression approach. Syst. Eng. 2017, 35, 16–24. [Google Scholar]

- Wang, Y.; Nie, G.; Shi, Y. Research on customers default rate of commercial banks in China based on credit scoring models. Manag. Rev. 2012, 24, 78–87. [Google Scholar]

- Lahkani, M.J.; Wang, S.; Urbański, M.; Egorova, M. Sustainable B2B E-commerce and blockchain-based supply chain finance. Sustainability 2020, 12, 3968. [Google Scholar] [CrossRef]

- Tibshirani, R. Regression shrinkage and selection via the Lasso. J. R. Stat. Soc. Ser. B. 1996, 58, 267–288. [Google Scholar] [CrossRef]

- Efron, B.; Hastie, T.; Johnstone, I.; Tibshirani, R. Least angle regression. Ann. Stat. 2004, 32, 407–499. [Google Scholar] [CrossRef] [Green Version]

- Fawcett, T. An introduction to ROC analysis. Pattern Recognit. Lett. 2006, 27, 861–874. [Google Scholar] [CrossRef]

- He, X.; Tang, L. Exploration on building of visualization platform to innovate business operation pattern of supply chain finance. Phys. Procedia 2012, 33, 1886–1893. [Google Scholar] [CrossRef] [Green Version]

- Raub, W.; Weesie, R.J. Reputation and efficiency in social interactions: An example of network effects. Am. J. Sociol. 1990, 96, 626–654. [Google Scholar] [CrossRef]

- Granovetter, M. The impact of social structure on economic outcomes. J. Econ. Perspect. 2005, 19, 33–50. [Google Scholar] [CrossRef]

- Hermes, N.; Lensink, R.; Mehrteab, H.T. Peer monitoring, social ties and moral hazard in group lending programs: Evidence from Eritrea. World Dev. 2005, 33, 149–169. [Google Scholar] [CrossRef]

- Chu, X.; Qin, X.; Liu, F. Research on credit risk assessment of transport supply chain based on entropy-TOPSIS model. Financ. Theory Pract. 2018, 1, 57–62. [Google Scholar]

- Chi, G.; Li, H.; Pan, M. Small enterprises credit rating based on default identification ability of combination weighting: Based on an empirical analysis of small industrial enterprises. Chin. J. Manag. Sci. 2018, 21, 105–126. [Google Scholar]

- Lee, H.L.; Shen, Z. Supply chain and logistics innovations with the belt and road initiative. J. Manag. Sci. Eng. 2020, 5, 77–86. [Google Scholar] [CrossRef]

- Chen, Y.; Yang, D.; Lian, P.; Wan, Z.; Yang, Y. Will structure-environment-fit result in better port performance?—An empirical test on the validity of Matching Framework Theory. Transp. Policy 2020, 86, 23–33. [Google Scholar] [CrossRef]

- Li, C. Research on the financial credit risk of online supply chain based on system dynamics. Popul. Sci. Tech. 2016, 8, 125–128. [Google Scholar]

- Li, Z.; Huang, J. A dynamic game analysis on financing difficulties of small and micro businesses in China. East. China. Econ. Manag. 2016, 30, 1–8. [Google Scholar]

- Li, H.; Li, D.; Wang, D. Reputation effects of big customers on debt financing: Evidence from supplier-customer relationships in China. J. Financ. Res. 2018, 6, 138–154. [Google Scholar]

- Luo, W.; Fang, M.; Liu, Z.; Pan, Q. Research on cooperation evolution of E-commerce logistics platform from the perspective of business ecology—A case of Cainiao logistics platform. China Bus. Mark. 2016, 21, 534–549. [Google Scholar]

- Wang, S.; Ji, B.; Zhao, J.; Liu, W.; Xu, T. Predicting ship fuel consumption based on LASSO regression. Transport. Res. Part. D Transport. Environ. 2018, 65, 817–824. [Google Scholar] [CrossRef]

- Meng, B.; Niu, E.; Kuang, H.; Luo, J. An evaluation model and empirical research on CSR based on cloud model. Sci. Res. Manag. 2018, 39, 139–150. [Google Scholar]

- Zheng, Z.; Bao, X. A research on check rate and punishment mechanism of accounts receivable mode in supply chain finance. Econ. Rev. 2014, 6, 149–158. [Google Scholar]

- Jiang, W.; Yao, W. The enforcement of the property law and supply chain finance: Empirical evidence from bank loans pledged by accounts receivable. Econ. Res. J. 2016, 51, 141–154. [Google Scholar]

- Altman, E.I. Commercial bank lending: Process, credit scoring and costs of errors in lending. J. Financ. Quant. Anal. 1980, 15, 813–832. [Google Scholar] [CrossRef]

- Hu, H.; Lang, Z.; Zhang, D. Research on SMEs credit risk assessment from the perspective of supply chain finance–A comparative study on the SVM model and BP model. Manag. Rev. 2012, 24, 70–80. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Actual Value | Predicted Value | Total | |

|---|---|---|---|

| 0 (Non-Default) | 1 (Default) | ||

| 0 (Non-default) | a | b | a + b |

| 1 (Default) | c | d | c + d |

| Total | a + c | b + d | a + b + c + d |

| First Level Variables | Second Level Variables | Third Level Variables | Indexes | Variables Description |

|---|---|---|---|---|

| Corporate Credit | Non-financial factors of SMEs | Registered capital | X1 | Registered capital of SME |

| Number of employees | X2 | Number of employees | ||

| Time of establishment | X3 | Time of establishment | ||

| Financial factors of SMEs | Return on equity | X4 | Net margin divided by total net assets | |

| Operating profit ratio | X5 | Operating profit divided by sales revenue | ||

| Current assets turnover ratio | X6 | Net income from main business divided by average total current assets | ||

| Operating growth rate | X7 | Growth of current operating income divided by operating income of last year | ||

| Debt asset ratio | X8 | Total l debt divided by total assets | ||

| Transaction Credit | The authenticity of transaction | Matching degree of order data | X9 | Matching degree of order flow, tax flow and capital flow for cross validation, which is divided into 5 grades |

| The performance of transaction | Ratio of on-time delivery | X10 | Ratio of on-time delivery according to the contract | |

| Ratio of contract enforcement | X11 | Actual delivery divided by contractual delivery | ||

| Number of contract defaults | X12 | Number of contract defaults | ||

| The sustainability of transaction | Degree of business concentration | X13 | Degree of business concentration, which is divided into 5 grades. | |

| The social relations of SMEs | X14 | Number of managers holding positions in other enterprises | ||

| Reputation and Supervision Behavior | Records of rewards and punishments from government departments | History of litigation | X15 | The value of 1 indicates that there is a history of litigation; The value of 0 means no litigation history |

| Number of being listed on credit blacklists | X16 | Number of being listed on credit blacklists | ||

| Tax incentive record | X17 | Number of tax rating as A | ||

| Number of administrative penalties | X18 | Number of administrative penalties | ||

| Number of abnormal operations | X19 | Number of abnormal operations | ||

| Business reputation | Industry recognition | X20 | Dynamic evaluation from the relevant website, which is divided into five grades. |

| Model | Sample Size | The Number of Non-Zero Coefficients Estimated | The Number of Correctly Estimated Zero Coefficients | The Number of Correctly Estimated Non-Zero Coefficients | Prediction Accuracy | AUC | ||

|---|---|---|---|---|---|---|---|---|

| The Training Set | The Test Set | The Training Set | The Test Set | |||||

| Lasso- logistic model | 100 | 4.050 | 3.950 | 3.000 | 0.996 | 0.978 | 0.999 | 0.998 |

| 200 | 4.250 | 3.700 | 3.000 | 0.989 | 0.979 | 0.999 | 0.999 | |

| 500 | 4.800 | 3.200 | 3.000 | 0.994 | 0.982 | 0.999 | 0.999 | |

| Ridge regression model | 100 | 3.800 | 4.200 | 3.000 | 0.964 | 0.930 | 0.996 | 0.989 |

| 200 | 4.150 | 3.850 | 3.000 | 0.980 | 0.961 | 0.998 | 0.995 | |

| 500 | 3.750 | 4.150 | 3.000 | 0.968 | 0.952 | 0.997 | 0.993 | |

| Logistic regression model | 100 | 2.000 | 5.000 | 2.000 | 0.936 | 0.925 | 0.983 | 0.973 |

| 200 | 2.000 | 5.000 | 2.000 | 0.920 | 0.892 | 0.977 | 0.960 | |

| 500 | 2.000 | 5.000 | 2.000 | 0.901 | 0.900 | 0.973 | 0.974 | |

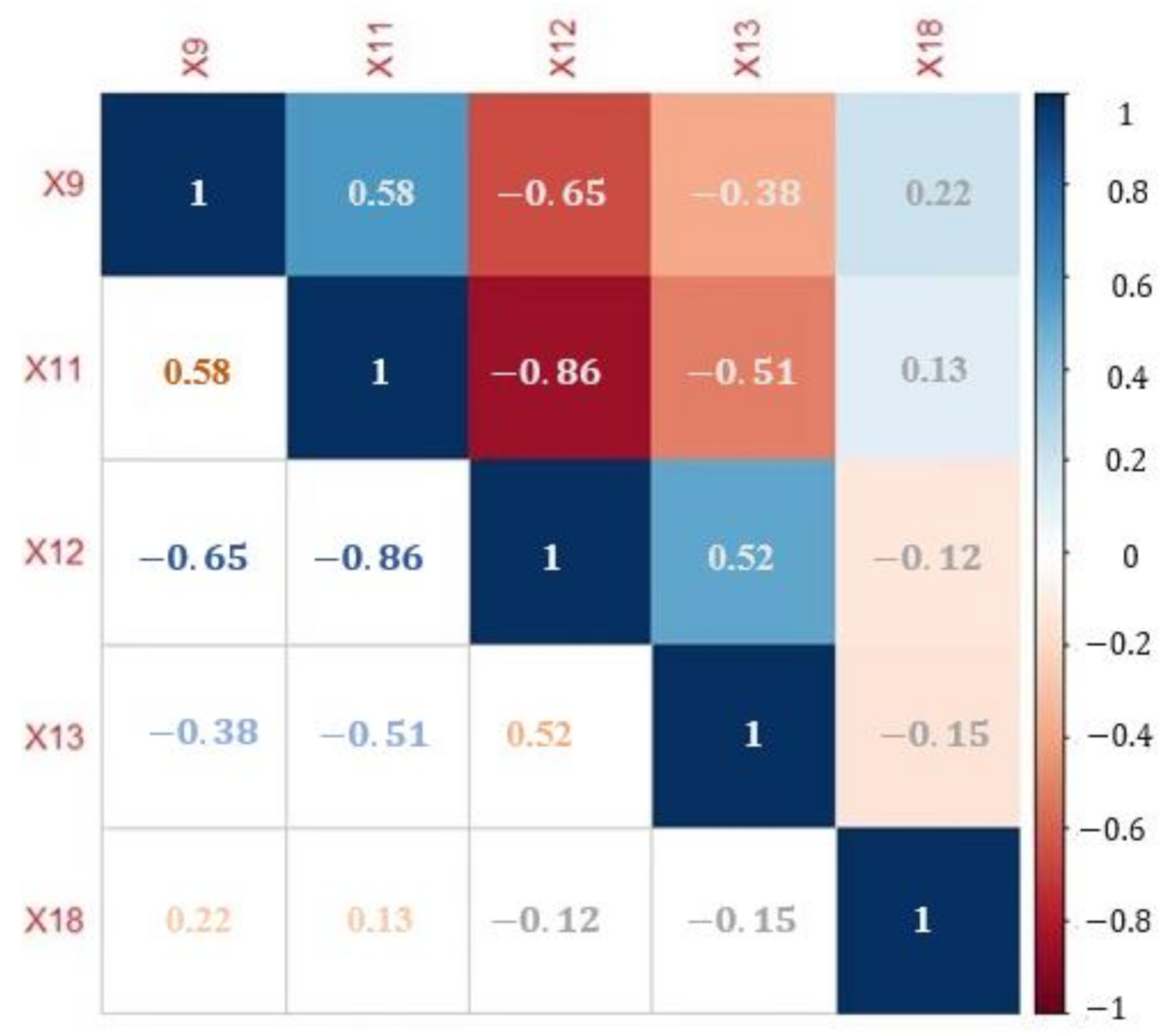

| Explanatory Variables | βj | VIF | Explanatory Variables | βj | VIF |

|---|---|---|---|---|---|

| X9 | −1.355 | 1.805 | X13 | 0.809 | 1.416 |

| X11 | −0.063 | 3.865 | X18 | −0.018 | 1.060 |

| X12 | 2.351 | 4.556 | / | / | / |

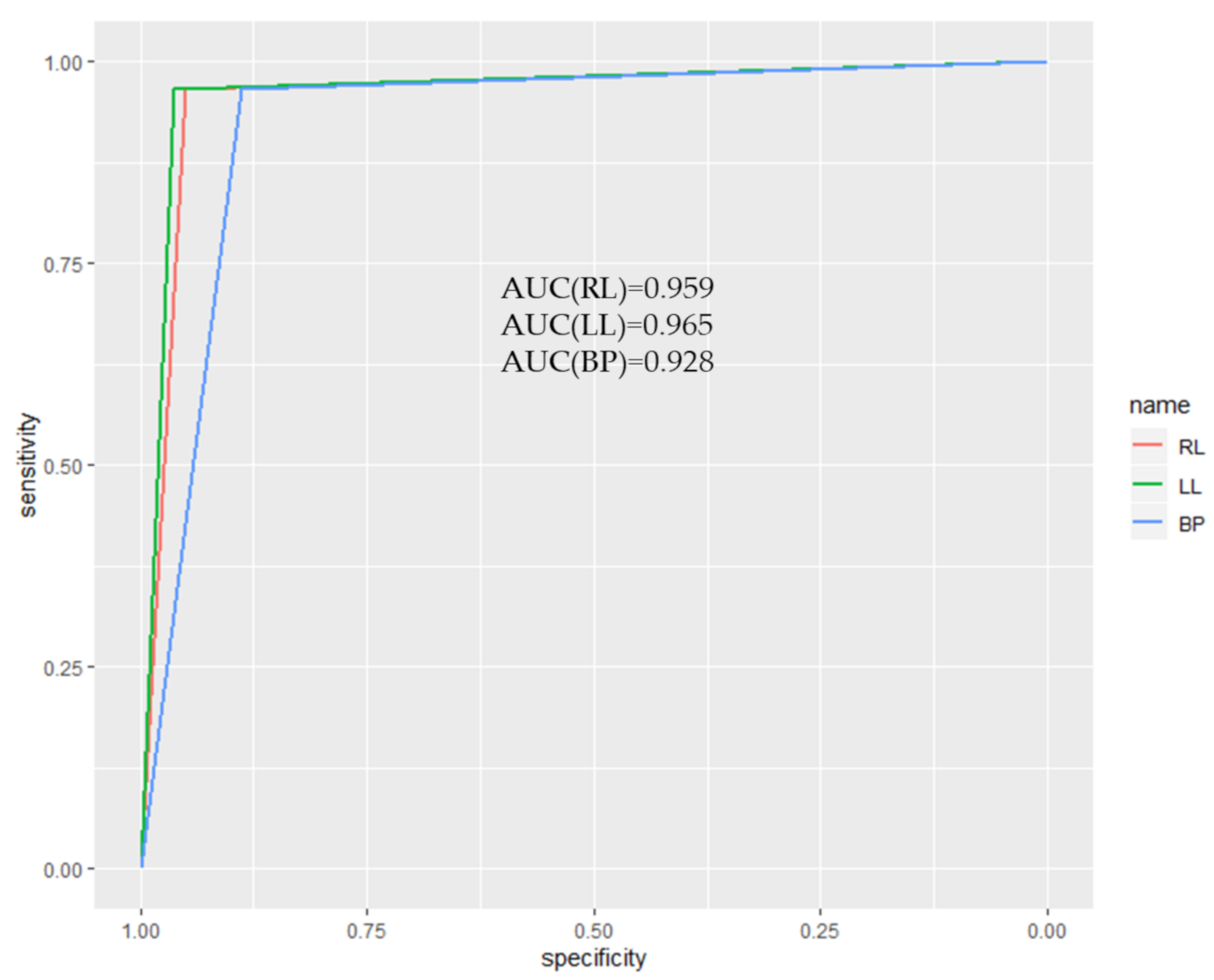

| Models | Prediction Accuracy | Type I Error | Type II Error | AUC | |

|---|---|---|---|---|---|

| Ridge regression model | 0.958 | 0.033 | 0.049 | 0.959 | |

| The train set | Lasso-logistic model | 0.965 | 0.033 | 0.037 | 0.965 |

| BP neural network | 0.923 | 0.033 | 0.111 | 0.928 | |

| Ridge regression model | 0.934 | 0.048 | 0.084 | 0.934 | |

| The test set | Lasso-logistic model | 0.964 | 0.044 | 0.032 | 0.962 |

| BP neural network | 0.903 | 0.049 | 0.148 | 0.903 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yang, Y.; Chu, X.; Pang, R.; Liu, F.; Yang, P. Identifying and Predicting the Credit Risk of Small and Medium-Sized Enterprises in Sustainable Supply Chain Finance: Evidence from China. Sustainability 2021, 13, 5714. https://doi.org/10.3390/su13105714

Yang Y, Chu X, Pang R, Liu F, Yang P. Identifying and Predicting the Credit Risk of Small and Medium-Sized Enterprises in Sustainable Supply Chain Finance: Evidence from China. Sustainability. 2021; 13(10):5714. https://doi.org/10.3390/su13105714

Chicago/Turabian StyleYang, Yubin, Xuejian Chu, Ruiqi Pang, Feng Liu, and Peifang Yang. 2021. "Identifying and Predicting the Credit Risk of Small and Medium-Sized Enterprises in Sustainable Supply Chain Finance: Evidence from China" Sustainability 13, no. 10: 5714. https://doi.org/10.3390/su13105714