A Review of the Recent Developments of Green Banking in Bangladesh

1

Faculty of Business and Law, University of Portsmouth, Richmond Building, Portsmouth PO1 3DE, UK

2

Department of International Business Strategy, Newcastle University, London E1 7EZ, UK

*

Author to whom correspondence should be addressed.

Sustainability 2021, 13(4), 1904; https://doi.org/10.3390/su13041904

Submission received: 31 December 2020

/

Revised: 1 February 2021

/

Accepted: 6 February 2021

/

Published: 10 February 2021

(This article belongs to the Special Issue Green Growth Policy, Degrowth, and Sustainability: The Alternative Solution for Achieving the Balance between Both the Natural and the Economic System)

Abstract

:This paper aims to explore the emergence of ‘Green Banking’ in Bangladesh, with a focus on the role of financial regulation and regulators in greening the financial sector. It also examines the contribution and involvement of banks and non-bank financial institutions in promoting green economic transition. The study is based on the review of secondary data collected from various sources, such as quarterly reports, annual reports, websites of the central bank of Bangladesh, and other commercial banks and non-bank financial institutions as well as various articles, and newspapers reports on green banking in Bangladesh. The collected data is reviewed using descriptive statistics. The research results reveal that the central bank of Bangladesh played a major role in greening the financial system of the country by implementing various green policies and regulatory measures. Although Bangladesh is still far behind the developed countries in terms of environmental performance, the country has made a remarkable progress in initiating and expanding green banking practices, infrastructure development, and accelerating green growth in recent years.

1. Introduction

Green banking (GB) is an emergent concept that occupies a significant position in the intersectional field of environmental policy, financial services, and socio-economic development. It starts with the aim of protecting the environment where banks consider, before financing a project, whether it is environmentally friendly and has any implications for the future [1]. The negative consequences of climate change threaten sustainable living on this planet and call for practical and immediate solutions from both developed and developing countries, which require intensive efforts from every domain of the economy, especially financial institutions. Stakeholders are concerned about business activities that have adverse impacts on society and the environment [2]. As a result, paying greater attention to the environmental issues across the globe has exerted pressure on all industries to become greener, including the financial services and more particularly banks [3,4,5]. As a consequence, the global banking industry has shifted towards an environmentally focused strategy through the adoption of green banking [6].

The issues of environmental protection have become very critical in emerging and developing countries, as these countries are more exposed to the immediate challenges of climate change, pollution, deforestation, loss of biodiversity, and arable land [7]. Their dependence on natural resources for economic growth and development underpins the need for implementing policy and plans for sustainable use of resources [8]. Consequently, emerging markets are taking the lead in regulating sustainable banking practices, focusing on the impact of the financial sector on sustainable development [9]. Supervisory authorities of these countries are taking a key role in the sustainable transformation of the financial system. Countries such as Bangladesh, Brazil, China, India, Indonesia, and Vietnam have already taken various strategic regulatory and voluntary measures aimed to address the challenges of climate change and environmental sustainability.

In this regard, environmental issues have increasingly found attention in the financial sector and the significance of greener and more inclusive financial systems is being increasingly recognized globally by academics, policy makers, and private firms. Although discussions on different concepts of socially responsible investments, drivers and strategies, and disclosure practices are available in different practitioner and scholarly publications [3,5,9,10,11,12,13,14,15,16,17,18,19,20], only limited academic research exists on the role of regulations in the enhancement of green banking practices in emerging countries. The impact of the mandates, instruments, and policies of central banks or the regulatory authorities on the actual green performances of financial institutions in the emerging markets is rarely discussed in the literatures.

Therefore, the study aims to determine the role of green initiatives implemented by the central banks in promoting the green economic transition. It is a first attempt at assessing to what extent regulatory policies adopted by a central bank/regulatory body in an emerging country plays a role in promoting sustainability in the financial system and greening the economy. We reviewed recent developments of the green activities that the banks and non-bank financial institutions (NBFIs) have adopted in practice. In particular, we focus on the following research question: What is the role of regulatory initiatives in enhancing the green banking performance in Bangladesh? Thus, the contribution of the research carried out in the paper is two-fold: (1) to identify the role of financial regulations and regulators in a developing country in implementing green banking, and (2) to determine the contribution and involvement of banks and NBFIs in fostering green banking.

The paper is structured as follows. Section 2 reviews relevant literatures and discussions about the emergence of green banking, the role of the financial sector in green growth, and the role of regulators in promoting green banking. Subsequently, Section 3 discusses the methods and materials used in this study. Section 4 reviews the case of Bangladesh with a focus on the range of policy instruments and supervisory measures employed by the central bank of Bangladesh in greening the financial system; along with the actual green activities that commercial banks and NBFIs have adopted. Section 5 comprehends the discussion in light with the key findings of the study. Finally, Section 6 summarizes and concludes the study.

2. Literature Review

2.1. Emergence of Green Banking

Green banking is an emerging concept integrating the management of environmental issues with banking activities aiming to transform the financial sector and develop new sustainable business models [21]. The concept was first unveiled by a Dutch bank named Triodos Bank, which was established in 1980 [22]. The bank had formed a “Green Fund” in 1990 to provide support for environmentally friendly projects and, thus, acted as a precursor for other banks intending to adopt green bank initiatives [22,23]. However, due to increasing interest in the topic and external pressure on banks to consider sustainable practices [24], this has become a buzzword in today’s banking sector [20].

As a response to negative effects of economic development on the environment, as well as at the global financial crisis, the international community seeks solutions for sustaining a sustainable economy and society [25]. In this context, the concepts of “green economy”, “green growth”, and “low-carbon economy” evolved [26]. United Nations Environment Programme (UNEP) defines the green economy as “the process of reconfiguring businesses and infrastructure to deliver better returns on natural, human and economic capital investments, while at the same time reducing greenhouse gas emissions, extracting and using less natural resources, creating less waste and reducing social disparities” [27] (p. 5). Green growth is a more focused concept: growth created through investment in the environment [28]. Consequently, green financing/green banking has seen significant progress in recent times because banks as financier has a huge influence on providing funding for the projects undertaken by industries, and thereby green banking can play a significant role in the creation of growth through investment in the environment and ensuring responsible behavior of other businesses too [4,29,30].

There is not yet a universally accepted definition of green banking [31]; however, a common thread in the literature is that green banking has a dominant focus on environmental sustainability. Some researchers suggest that green banking is the normal process of banking where all the activities are controlled by the same authorities yet putting extra care on environmental sustainability [32,33,34,35]. Lalon [20] defines green banking as any form of banking that generates environmental benefits. Bhardwaj and Maholtra [36] stated that green banking is an effort by the banks to make the industries grow green and, in the process, restore the natural environment. According to Masukujjaman and Aktar [17], green banking refers to eco-friendly or environment-friendly banking systems to stop environmental degradation in order to make this planet more habitable. Tara et al. [37] indicated that green banking requires prioritizing financing to the sectors that promote various environmental protection activities. As a part of green banking initiatives, the banks and non-bank financial institutions adopt environment-friendly financing mechanism as well as green transformation of internal operations [38,39]. The process restores the natural environment with a view to ensure green safety and sustainable ecological balances [36]. Chowdhury and Dey [40] referred to GB as the operation of banking activities while giving special attention to social, ecological, and environmental factors with the aim of the conservation of nature and natural resources.

However, the ambiguity as to what constitutes green banking activities and products represent an obstacle for the classification of green assets as well as for the identification of further opportunities for green investments [41].

2.2. Role of Financial Sector in Green Growth

The allocation of funding to its most productive use is a key responsibility of finance. Thus, the financial sector can play an important role in managing climate-related risks and support the transition to a low carbon economy by driving investments in climate-friendly and green projects [42]. The banking institutions are the key actors in the financial system and occupy a significant position in the global economy [43,44]. They exercise the ability to have a strong impact on economies, societies, and sustainable development [45,46,47,48,49]. While the direct environmental effects of banks are low in comparison to other sectors [50], they have a significant indirect impact on sustainability through lending and investments that facilitate the expansion of polluting activities [47,50,51,52,53].

Banking institutions are the primary source of finance for many industrial projects such as steel, paper, cement, chemicals, fertilizers, power, textiles, etc., with potentially significant adverse social or environmental impacts [53]. Therefore, as financiers they have huge influence on the projects undertaken by industries, and thereby green banking can play a significant role in ensuring responsible behavior of other businesses too [4,29,30]. Accordingly, green finance is defined as comprising “all forms of investment or lending that consider environmental effect and enhance environmental sustainability” [54] (p. 2). Important aspects of green finance are sustainable investments and banking, where investment and lending decisions are taken based on environmental screening and risk assessment to meet sustainability standards, as well as insurance services that cover environmental and climate risk [55,56]. Further literatures on green financing suggest [57,58,59,60], cited in Bai, 2011, that green finance, within the banking sector, can be presented in a wide spectrum of market-based lending or investing businesses, involving retail banking, project financing, asset management, types of loans, and investment finance that are all responsible for the environment and society.

As such, banks can play a leading role in the transition to a low-carbon and greener economy by considering the entire spectrum of risks and through evaluating the projects from both an economic and environmental perspective [41]. They can define their lending strategy regarding which sectors and projects that are eligible for lending and can impose higher cost for projects that cause a threat to the environment. Moreover, using their commercial lending and securities underwriting, banks can catalyze the necessary transition to an economy that minimizes greenhouse gas pollution and relies on energy efficiency and low/no carbon energy sources [61].

2.3. Role of Regulators in Promoting Green Banking

The connection between climate change and the financial industry has been addressed in recent years not only by environmentally concerned organizations but also by the financial sector regulators. Green banking has advanced in recent years as policy makers and market participants increase efforts to promote long-term socio-economic and environmental factors. These efforts include increasing access to financing for green projects, developing sustainability-related principles and guidance to shape frameworks as well as enhancing financial reporting and disclosure [62].

Safeguarding financial stability has always been one of the key responsibilities for central banks. Climate change and other environmental risks pose a great threat to the financial stability and to the overall financial system [63,64,65]. Three different types of risk have been identified [64]. Transition risks are those that could arise from a sudden and disorderly transition to a low-carbon economy. Physical risks are “those risks that arise from the interaction of climate-related hazards (including hazardous events and trends) with the vulnerability of exposure of human and natural systems” [66] (p. 9). Liability risks stem from “parties who have suffered loss from the effects of climate change seeking compensation from those they hold responsible” [67] (p. 2).

Central banks are among the most important stakeholders in the banking business as they have the necessary leverage to coerce/impose various influences on commercial banks and other financial institutions in order to conform to certain prescribed rules and regulations to carry out their business in an environmentally friendly manner [68]. Through their regulatory oversight over money, credit, and the financial system, central banks are in a powerful position to support the development of green approaches and enforce an adequate pricing of environmental and carbon risk by financial institutions [68]. Hence, to tackle climate-related financial issues and potential disruptions and to promote green and sustainable finance, a growing number of central banks and regulators around the world are becoming aware of their role and addressing climate change and environment risks in their mandate [68,69]. Globally, many central banks have already adopted sustainability policies to regulate or guide the activities of banks [42] or have started to incorporate climate risk into macro-prudential frameworks [70]. These regulations also seek to address in-house resource consumption for positive contributions towards the transition of green growth.

Nevertheless, central banks and supervisors across different jurisdictions operate within different mandates and legal frameworks [71] depending on the country and related institutional frameworks [72]. It is evident that emerging economies are the most engaged in pursuing green policies in the banking sector primarily because of regulatory requirements [65,73] while the green finance activities in developed countries are mostly voluntary and driven by the decision-makers’ awareness of sustainable development and corporate social responsibility [74].

Besides financial regulation, industry leadership plays a crucial role in implementing green/sustainable banking approaches. A growing number of financial institutions around the world have voluntarily either created their own networks or initiatives or joined platforms established by international development agencies such as the International Finance Corporation (IFC) and UNEP [75]. A group of central banks and supervisors launched the Networking for Greening the Financial System in 2017 to contribute to the analysis and management of climate and environment-related risks in the financial sector and to mobilize mainstream finance to support the transition toward a sustainable economy [76]. The Task Force on Climate-related Financial Disclosure was established by the Financial Stability Board, which is an international body that monitors and makes recommendations about the global financial system, with an aim to develop voluntary, consistent climate-related financial risk disclosures that would be helpful to investors, lenders, insurance companies, and asset managers in identifying and managing financial risks [77]. Moreover, the G20 Sustainable Finance Study Group, which was formerly known as G20 Green Finance Study Group, was created to identify barriers to green finance and improve the financial system to mobilize private capital for green and sustainable investment [78]. Global Alliance for Banking on Values (GABV) is an independent network of banks and banking cooperatives with a shared mission to use finance to deliver sustainable economic, social, and environmental development. Among other initiatives, Equator Principles (EP), the Impact Investing and Reporting Standards (IRIS), the Global Reporting Initiative (GRI) for subgroups of financial products and services, project finance, and institutional investment are worth mentioning [79].

3. Materials and Methods

The research is descriptive in nature and mainly based on the secondary data. It points out the regulatory and policy initiatives (financial and nonfinancial) of central banks relating to green financing. The advantage of this review process is that the data already exist in some form and can be evaluated for appropriateness and quality in advance of actual use [80]. In addition, quarterly reports on green banking in Bangladesh, websites of commercial banks and non-bank financial institutions and different organizations such as, World Bank, UNEP, published articles in different journals and renowned newspapers were also reviewed to gain insights. The research follows a qualitative approach and the research design involves organizing, collating, and assessing these data samples for valid research conclusions. The scope of the study is limited to banks and NBFIs operating in Bangladesh and excludes other financial institutions such as insurance companies, investment companies, and capital market intermediaries like brokerage houses.

4. Green Banking in Bangladesh

4.1. Emergence of Green Banking in Bangladesh

Bangladesh is also one of the fast-growing economies in South Asia, aspiring to gain the status of a middle-income country soon and has been making great strides in terms of social, economic, and technological transformation [78]. Between 2000 and 2017, the country has more than tripled its per capita income (in US$) and more than doubled it in terms of purchasing power parity in the same period. It recorded a commendable gross domestic product (GDP) growth rate of 7.86% in 2018 [81].

Nevertheless, this economic growth has increased industrialization and initiation of several mega projects, which eventually comes with a price of environmental degradation. Bangladesh’s CO2 emissions per capita have more than doubled from 0.2 to 0.46 metric tons of CO2 per capita between 2000 and 2016, although remaining very low (less than one tenth) compared to the world’s average of 4.8 t CO2/capita [78]. Climate vulnerability and potential threats of economic slowdown makes sustainability a prime development concern for the country [82,83,84,85], resulting in strong calls for adopting and implementing ambitious mitigating policies. The country is one of the worst sufferers of environmental pollution and climate change impacts, while being responsible for less than 0.35% of global greenhouse gas emissions [86], which is very insignificant compared to other developed and developing countries [87].

Climate change has already enhanced the intensity and frequency of floods, droughts, and cyclones in Bangladesh and these catastrophes are likely to become more frequent and severe in the coming years [17]. Bangladesh is a low-lying country that is highly susceptible to climate change outcomes, such as floods, draught, salinity, cyclones, and sea-level rises. Almost 75% of its territory lies less than 10 m above sea level, and more than 700 rivers run through its territory, making it highly vulnerable to climate change risks [85,88,89]. Tens of millions of people in Bangladesh are already at extreme risk from these environmental hazards and continued exposure leads to suffering, loss of potential, premature death, and the onset of debilitating non-communicable diseases [90,91,92]. In terms of financial damages, floods come up as the most devastating disaster type resulting in the loss more than 8.5 billion USD [92]. Rahman and Lateh [93] show the average temperature of the country rises by 0.2 C per decade. The adverse consequences of climate change outcomes would be enormous for a densely populated country of over 160 million inhabitants with 1252 people per square kilometer [56,94,95]. According to United Nations Framework Convention on Climate Change (UNFCCC), the country will be burdened with significant losses if the situation remains unchanged and it is estimated that the annual loss would be 2% and 9.4% of GDP by 2050 and 2100, respectively [96]. Another report of the World Bank shows that about 5.3 million poor people will be vulnerable to the effects of climate change in 2050 [81].

Financial sector of Bangladesh is mainly a bank-based system [97] that also includes NBFIs, capital market intermediaries, insurance companies, and microfinance institutions. Currently, there are 59 scheduled banks and five non-scheduled banks in the country operating under the control and supervision of the Bangladesh Bank (BB), which is the central bank in the country. There are also 34 NBFIs operating in Bangladesh [98]. Unlike in developed economies and sophisticated markets, both long- and short-term financing needs of the country are met by the banking industry [98]. However, the banking industry has experienced several challenges in the past few years. The banking sector of Bangladesh exhibits significant risks and vulnerabilities in the areas of non-performing loans, inadequate credit information, poor governance, and lengthy legal procedures [86]. The sector is also stressed with the slander of some financial scams in a few state-owned commercial banks (SCBs) and private commercial banks (PCBs) uncovered in recent years.

4.2. Initiatives for Greening the Financial System in Bangladesh

Green banking initiatives in Bangladesh are broadly categorized into the following four aspects: (1) policy initiatives, (2) green banking activities of banks and NBFIs, (3) refinance support from BB in diverse green products/sectors, and (4) BB’s initiatives for in-house environmental management. Accordingly, the following sections will review and analyze data from the annual reports of from 2016 to 2020 to provide evidence of these four categories.

4.2.1. Policy Initiatives

Bangladesh Bank (BB), the central bank of the country, gained recognition being an early mover in this case through formulating policies and facilitating innovative schemes for promoting green finance. Since 2011, the BB has developed several policies to promote sustainable finance. Environmental Risk Management (ERM) Guidelines for Banks and Financial Institutions was issued in 2011, which required the banks and financial institutions to conduct a preliminary review based on the due diligence checklists, and a detailed environmental review prior to making investment decisions in projects [98,99]. These guidelines were implemented in three main phases: “phase one, the policy formulation and governance; the second one related to green strategic planning and specific environmental policies and the third phase designing and introducing innovative products” [100] (p. 4). Additional support is offered by the BB through the publication of the ERM Guidelines, as well as Environmental Due-Diligence Checklists, to enable commercial banks to appropriately assess risk and finance environmentally sensitive projects [65,99,101].

In 2013, Bangladesh Bank, jointly with IFC, assessed the implementation experience of ERM Guidelines in the country. Based on the findings, BB has published the updated version of the guidelines in February 2017, now termed Environmental and Social Risk Management (ESRM) Guidelines. The new ESRM Guidelines have incorporated risk mitigation measures and integrated environment and social risks into overall credit management in a more comprehensive manner. The updated version contains a more robust quantitative risk rating system compared to the subjective qualitative risk assessment method of the previous ERM Guideline. It included evolving contemporary social and climate risks for the country and provided user-friendly reporting features for banks and financial institutions. BB has set the minimum annual target of direct green finance at 5% of the total loan disbursement since January 2016 for all banks and financial institutions. The green banking policy guidelines also requires banks and financial institutions to form a Climate Risk Fund and allocate at least 10% of their Corporate Social Responsibility budget to this fund. This fund can be utilized either through providing grants for implementing relevant projects or financing green projects at concessional interest rates. Banks and financial institutions (FIs) have been instructed to set up Solid Waste Management System, Rainwater Harvesting, and Solar Power Panel in their newly constructed or arranged building infrastructure [87,97,99]. Table 1 below depicts green banking policy initiatives taken by Bangladesh Bank.

4.2.2. Current Trends and Green Banking Activities of Banks and NBFIs in Bangladesh

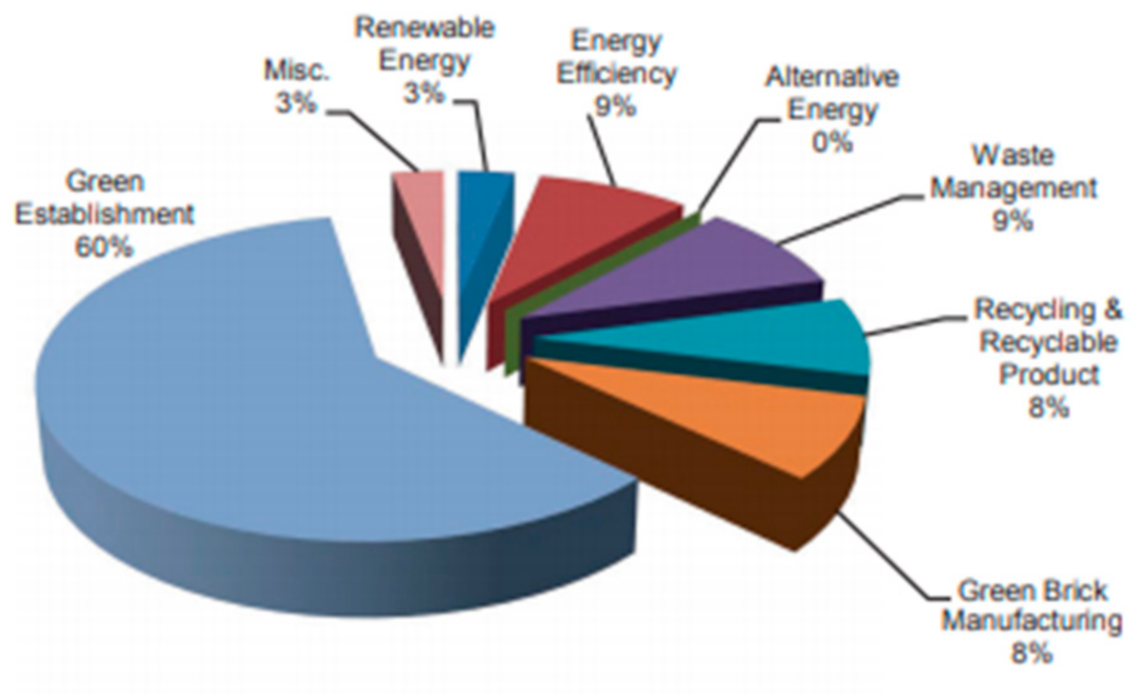

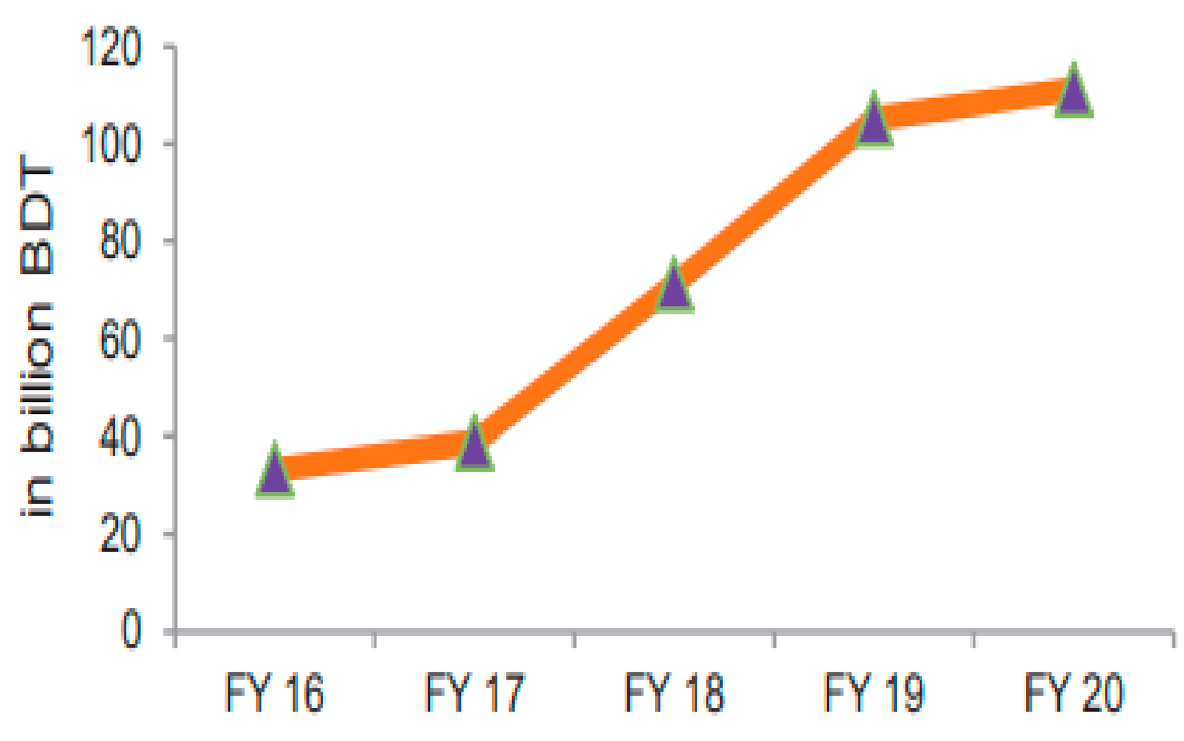

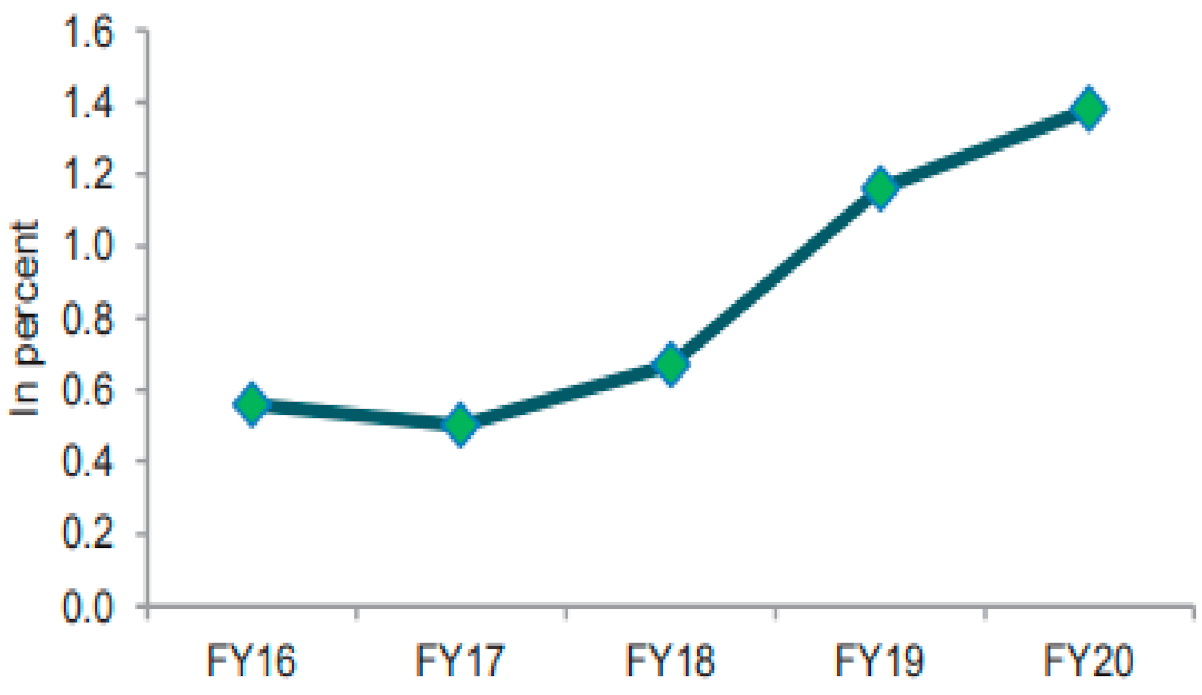

This section outlines the green banking trends of Bangladesh in the recent years and exhibits green banking activities of banks and NBFIs accumulated from the annual reports of 2016 to 2020. While Table 2 below represents category-wise direct green finance in 2020, Table 3 shows year on year disbursement of green finance during the last five years. Table 4 shows the snapshot of quarterly sanction and disbursement of total finance along with green finance in 2020. Figure 1 presents share of category-wise green finance in FY20. Figure 2 and Figure 3 displays the green finance trend by banks and NBFIs in the last five years, where Figure 2 indicates trend in total green finance (directly disbursed) and Figure 3 indicates the trend in the percentage of green finance of total funded loans disbursed.

Total amount of direct disbursement of green finance by banks and NBFIs in Bangladesh during the financial year 2020 was 228,153.5 billion Bangladeshi Taka (BDT) or approximately USD 2737.84 million (see Table 1). Of the total disbursed amount, BDT 105.9 billion (approx. USD 1270.8 million) has been distributed by banks and BDT 5.3 billion (approx. USD 63.60 million) by NBFIs. It shows that the investments made by banks in green initiatives have increased to BDT 7167.18 million (approx. USD 86.01 million), which is a 7% growth over the previous year. However, in the case of the NBFIs, it has been decreased by BDT 1204.7 million (approx. USD 14.46 million), which is 19% lower than the previous year.

From Table 3 above, in terms of banks, a positive trend in the year-on-year relative percentage changes can be observed, especially from the year 2017. A new guideline ‘Environmental and Social Risks Management (ESRM)’ along with an Excel-based Risk Rating Model for banks and financial institutions in Bangladesh were issued to evaluate Environmental and Social Risks in the process of Credit Risk Management in this year. New prudential regulations and reporting requirements were also introduced by Bangladesh Bank. These have visible implications in the volume and year-on-year green performances. In 2018, the investment increased 99.7% from the previous year. However, a relatively slow growth can be observed in 2019 and 2020. The possible reason could be the pandemic that affected the overall investment opportunities in the country. It is also evident that private commercial banks have contributed around 80% of the total green finance, playing a significant role in greening the economy of the country.

Nevertheless, the case is not the same for the NBFIs. Although NBFIs have achieved impressive growth in recent years the year-on-year growth of green finance has been unstable and slow over the years. A negative growth trend has been noticed from year 2016 to 2018 where the year-on-year growth decreased by 28.5%, 22.1%, and 26.8%, respectively. While in 2019 there has been a substantial improvement with a growth of 91.8%, it was decreased by 18.5% in 2020. There are only 34 NBFIs currently operating in Bangladesh while there are 60 scheduled banks. In comparison with the commercial banks, the business line of the NBFIs is narrow, as their investments are mostly concentrated in industrial sector. Most NBFIs conduct their merchant banking activities through separate subsidiaries like banks. These could be the possible reasons for the lower green performances of the NBFIs compared to the banks.

Figure 1 shows the category-wise percentage of green finance in 2020 where it is evident that the majority of the green finance was mobilized in the green establishments with a share of 60% of the total green finance. Figure 2 shows the trend in total green finance (directly disbursed) by banks and NBFIs during last five years. There is a significant upward trend from FY17. Figure 3 also indicates an upward trend in terms of the share of green finance in total funded loan disbursement [98]. However, the recent peak of 1.6% of total loans is still less than a third of the target of 5% set by BB in 2014, and again in 2020.

4.2.3. Refinance Support from Bangladesh Bank

Apart from the policy initiatives, to broaden the financing avenue for green products like solar energy, biogas plants, and effluent treatment plants, etc., BB established a revolving refinance scheme amounting to BDT 2 billion (approx. USD 48 million) from its own fund for solar energy, biogas, and effluent treatment plant (ETP) in 2009, which was increased to BDT 4 billion subsequently. Bangladesh Bank also launched a refinancing window targeting the green transformation of brick industries in 2012 [87,97,102]. The Asian Development Bank (ADB) funded USD $50 million in Financing Brick Kiln Efficiency Improvement Project aimed at reducing emissions of greenhouse gases and fine particulate pollution through promoting use of energy efficient modern technology in the existing traditional brick fields. So far, 35 banks and 21 financial institutions so far have signed participation agreement with Bangladesh Bank to utilize this fund [98].

Table 4 below presents the product wise disbursement figure from FY16 to FY20. It shows that in FY20, total disbursement under the BB’s refinance was BDT 568.54 million (approx. USD 6.82 million). An increasing trend in the disbursement of refinance scheme can be observed from the total disbursements during the period of last five years [98].

Table 4 shows that, although the overall reimbursement under the green products refinancing scheme has grown over the years, the growth has been unstable and slow. Year 2017 has seen the maximum growth, which has been around 134% more from the previous years. A comprehensive list of products/initiatives for banks and FIs has been circulated this year, which could be a possible reason for this growth. While a decline in the % of growth can be seen in the following two years, there has been a significant growth of around 77% in year 2020. This is probably because in 2020, Bangladesh Bank has almost doubled the amount of funding for three refinance schemes—cottage, micro, small, and medium enterprises to ensure the long-term investment flow due to the Covid-19 impact. In addition, the interest rates for the schemes, for banks and customers, have been reduced by two percentage points, each making it a 3% for the banks to avail the funds from the regulator and 7% for the customers, which was 5% and 9%, respectively [98,99]. A list of eligible green products/initiatives under “Refinance scheme for green products/initiatives” can be found in Appendix A.

In September 2014, Bangladesh Bank introduced an “Islamic Refinance Fund” with the surplus liquidity of Shariah based Islamic banks and NBFIs. To encourage further involvement in green finance, BB launched a refinance scheme for the Islamic banks and NBFIs operated by “Islamic Refinance Fund”. The scheme was later renamed as “Refinance Scheme for Islamic Banks and Financial Institutions for Investment in Green Products/Initiatives”. These banks and NBFIs can utilize this fund for financing in the 52 products identified under BB’s Refinance scheme.

The central bank also launched Green Transformation Fund (GTF) in 2016, a $200-million refinancing scheme sourced from Bangladesh Bank’s own resources for export-oriented sectors like textile, jute, and leather industries. From that fund, all manufacturing industries can avail loans at less than two per cent interest, to import environment-friendly and energy-efficient capital machinery and accessories [87,97,99].

4.2.4. Initiative of Bangladesh Bank for in-House Green Practices

BB has taken several initiatives to make the in-house operational activities more environmentally friendly, energy efficient, and technologically advanced ones. To reduce CFC emission, a chiller based central air conditioning system has been installed. Moreover, BB has installed a solar power system on its rooftop to increase energy efficiency. E-recruitment, documentation management system, leave management system, online salary and account statement, personal file update system, online office orders, electronic pass for visitors, and many other initiatives were also introduced through the BB intranet. Most of the regulatory reporting from banks and NBFIs are collected through a web upload and Enterprise Data Warehouse (EDW) system [98]. Some of the Bangladesh bank’s in-house green practices include:

- Rooftop Solar Power System and Chillar Based Air Conditioning

- Online Documentation and Leave Management System

- Online Office Order and Electronic Pass for Visitors

- Enterprise Data Warehouse (EDW) System

- Bangladesh Electronic Fund Transfer Network (BEFTN)

- Carbon Footprint Measurement and E-recruitment

- Enterprise Resource Planning (ERP) and Online Account Statement

- LAN/WAN Computer Network among all BB offices

- Bangladesh Automated Cheque Processing System (BACPS)

- Credit Information Bureau (CIB)

4.3. Role of Government in Greening the Economy of Bangladesh

The government has also been supportive in promoting sustainable banking and financing activities in the country. Especially, the government’s efforts on the way to attain Sustainable Development Goals (SDGs) are very much allied with the sustainable banking ventures [103,104,105].

Bangladesh has made significant progress in banking reforms among 38 SBN countries to drive development and fight climate change [100,102]. These reforms require banks to assess, manage, and report on environmental, social, and governance risks in their lending operations. The government of Bangladesh has undertaken a series of major policy and institutional changes. The adoption of the Bangladesh Climate Change Strategy and Action Plan and the creation of the Climate Change Trust Fund from its own resources to finance projects for implementation of BCCSAP, represent the government’s pledge and readiness to reduce climate vulnerabilities [97] to provide strategic direction on climate change.

Further, to provide a roadmap for climate finance in the country’s public financial management systems, the country adopted a Climate Fiscal Framework in 2014, which is another significant step towards linking climate policies and strategies with the resource allocation process. Apart from that, Bangladesh has also developed “National Adaptation Programme of Action” (NAPA) and “Nationally Determined Contributions” as part of its engagement with UNFCCC [97,98]. Investments in “climate proofing” have resulted in major positive impacts on climate-resilient economic growth and poverty reduction in the country.

The government is in the process of implementing the National Financial Inclusion Strategy (NFIS) that was approved by the Cabinet in July 2019. “Financial Inclusion Department (FID)” of BB has actively been engaged in handling policy and regulatory issues of the central bank associated with financial inclusion. No Frill Accounts (NFAs) and refinancing activities targeting vulnerable sections of the society facilitated by the FID are also expanding. In January 2020, the Bangladesh Financial Intelligence Unit (BFIU) BFIU issued an electronic Know Your Customer (e-KYC) guideline to open accounts in the financial sector without filling up any paper-based documents [106].

5. Discussion

It is evident that Bangladesh has made significant accomplishments in terms of policy perspectives. The above review of the data from the past few years shows that the policy and regulatory interventions have a significant positive impact in the green performances of the banks and non-bank financial institutions in Bangladesh. The study suggests that the implementation of the Policy Guidelines for Green Banking by the Bangladesh Bank in three phases, ending in 2015, and the introduction of guidelines on Environmental and Social Risk Management (ESRM) for banks and financial institutions in Bangladesh in 2017 bring positive change to green financial performance. This finding is consistent with [107], whose study conducted on 148 listed companies on the Dhaka Stock Exchange (DSE) found that introduction of new policy guidelines significantly improved sustainability performance of the listed firms. By the discreet initiatives of the central bank (coupled with potent support from the government), Bangladesh has been placed on the global map by championing the development role of central banks in advancing financial inclusion and green finance. Green banking has improved in recent years, both in terms of green financing and in-house endeavors of environmental risk management. All scheduled banks have formed their own Sustainable Finance Unit and Green Banking Policy. All the FIs have also formed their own Green Banking Policy. Currently, 58 Banks out of 59 have at least one online branch and 45 banks have introduced Internet-banking facility up to 30 September 2020 [97].

Bangladesh Bank has also built partnership with different international strategic alliances and has also become a member of international organizations to boost up the green banking practices [39,98]. The bank is an active member of the Sustainable Banking Network (SBN) and has been one of the most supportive SBN country regulators in the development of its national sustainable banking framework. Bangladesh has also partnered with UNEP inquiry since it started it’s journey in 2014 [92,108]. Few other banks and financial institutions are also engaged with different international organizations to promote sustainable financing. For example, BRAC Bank, one of the largest commercial banks in Bangladesh, is a member of GABV and UN global compact. Mutual Trust bank has also recently joined as a member of UN Global Compact. IDLC Finance Limited is the largest non-bank financial institution in Bangladesh and is signatory to local and international initiatives promoting sustainable business practices to CSR activities such as UN Global Compact, UNEP Finance Initiative, and CSR Centre [99,109].

Adoption of technology brought changes in the policy and regulatory approach of the BB in the areas of technology driven services like mobile banking and agent banking. An increase in the automation towards green banking has been observed with the expansion of online branches. At least 90 percent of the branches of the country’s commercial banks are now fully online, according to the latest statistics of the central bank. Refinance support from BB is also playing an important role to incentivize the green banking activities. In addition to banks, non-bank financial institutions such as the state-owned Infrastructure Development Company Limited (IDCOL) play a key role in intermediating refinancing to enable households to purchase solar home energy systems, domestic biogas, solar irrigation systems and solar mini grids. IDCOL combines concessional refinancing to microfinance institutions and with technology assessments, quality control, monitoring, and other support services [99,109].

Previous reports from 2011 and 2014 emphasized that Bangladesh was far behind in green banking compared to its counterparts from the developed countries [16,104]. However, a more recent report exploring green banking in emerging markets suggests that the country has not only made substantial progress but is also a leader among emerging markets when it comes to green banking regulation [110]. The World Bank’s International Finance Corporation on Green Banking provides information on green banking in 35 emerging markets. Their framework analyses three dimensions: (1) green loans market size (share of total loans and % of banks offering green loans), (2) maturity of green policy and regulation, and (3) level of offering of green bonds.

- (1)

- The report estimates that in average the share of green loans to total loans in emerging market financial institutions is 7%. However, the IFC notes that this figure has been estimated based on assumptions and partial surveys because only two countries, China and Bangladesh request banks to report periodically on green loans. In terms of % of banks offering green loans, the report does not provide neither an average nor country figures, but reports result from a survey of 400 banks in Latin America: 49% out of 400 banks offered green banking.

- (2)

- Maturity of regulation and policy is assessed analyzing government and central banks requirements and quality of legislation. There are five stages: Initial, Formulating, Emerging, Established and Measuring, Mature and Changing behavior. There are no countries in the mature stage, and only 8 out of 35 in the Established and Measuring Stage (Bangladesh, Brazil, China, Colombia, Morocco, Nigeria, South Africa, and Vietnam). Quality of Measuring is analyzed looking at whether the regulations provide; (a) definition of green assets and investment sectors, (b) legal requirement for periodical report, and (c) specification of climate change as a standalone risk. Only Bangladesh and China fulfill all three criteria.

- (3)

- Offering of green bonds: The report estimates that 21% of banks offer green bonds but note this is the indicator with the lowest level of actual data.

Comparing our results with this report, we conclude that Bangladesh is a leader among emerging countries in terms of the maturity of regulation. However, such leadership does not yet translate in a sizable green banking market (1.6% green banking share in Bangladesh, about 20% of the average share of 7% in emerging countries). According to the quarterly review reports of green banking by the Bangladesh Bank, approximately 49.4% of institutions have had an exposure in green finance in 2020. This might be because Bangladesh seems to be following Korea’s Green State strategy—which is reliant on a strong state [111]. However, while Korea has strong institutions, Bangladesh’ s weaker institutional environment creates additional challenges for the private sector and as a consequence, the initiative has yet to gain momentum in keeping with the size of the country’s economy and the latest measures taken by the global community.

Although the central bank of the country has initiated green practices as early as 2009, and the legislation is comprehensive and advanced, implementation and enforcement are patchy. Recent studies revealed that some banks are still in the first stage of the green banking adoption in terms of the prescribed guidelines by the Bangladesh Bank [112,113]. BIBM [99] reported that there is a lack of consciousness at all levels regarding “green banking”. According to ADB Institute [56], the total disbursement under the refinancing scheme for green products in Bangladesh has been very slow. According to the Bangladesh Bank report, the outstanding loans under green finance stood at BDT 28, 5290 million as of September this year, up 131 percent from previous year.

Consequently, despite the increasing levels of regulatory adoption of sustainability policies and green initiatives, the country remains far behind in terms of environmental performance [111]. According to some indicators, Bangladesh ranked among the top ten countries in the world most affected by extreme weather events during 1998–2018 and currently holds 7th position in the list of German watch long-term climate risk index [114,115]. Losses linked to such events were estimated annually to average 1.8 percent of GDP between 1990 and 2008 [88]. Furthermore, the country has ranked 162nd out of 180 countries in the 2020 Environmental Performance Index (EPI) that evaluates the condition of environmental health and vitality of their ecosystems. Nonetheless, two years ago, the country was in the 179th position, being the second worst performer in the world. There are 32 performance indicators under these 11 issue categories which are air quality, sanitation and drinking water, heavy metals, waste management, biodiversity and habitat, ecosystem services, fisheries, climate change, pollution emissions, agriculture, and water resources. Bangladesh performed poorly in the top-weighted categories, such as air quality (166th), climate change (140th), heavy metals (172nd) and biodiversity and habitat (124th). In the latest ranking, the country scored only 29 out of 100, securing the third worst position in the South Asia region, only ahead of India at 168th and Afghanistan at 178th position [114,115].

The ongoing economic hardship caused by the corona virus pandemic may also reduce the rate of commercial profitability and growth of green investments. In this context, green banking indicators need to be included at the core to estimate financial stability of the banking sector. Adopting newer approaches in identifying and preventing environmentally harmful activities by banks and NBFIs also needs to be considered. Bangladesh Bank, in a recent circular has mentioned that banks and NBFIs will have to disburse 5% of their term loans, excluding employee loans, for green financing. Previously, the banks were supposed to invest at least 5% of their total funded loans to environment friendly initiatives. Compliance with the target was made mandatory; otherwise the Camels rating of the entities would deteriorate. A drop in Camels rating would ultimately create multidimensional problems for the financial institutions, and it would act as an indirect penalty. The central bank came up with the instruction as the disbursement of credit by the banks and NBFIs in the April–June quarter this year dropped by 16.83% compared to that in the previous quarter [48].

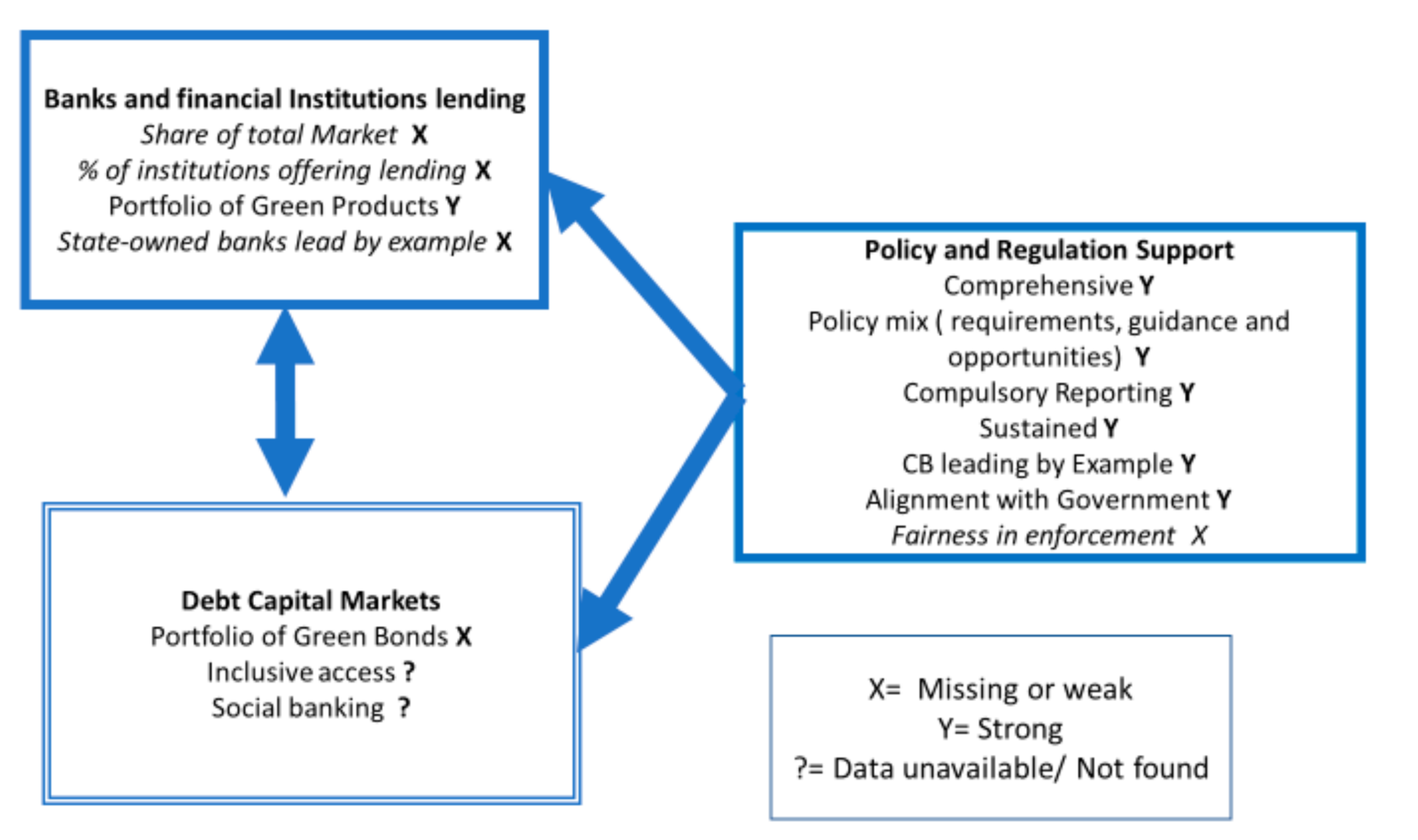

The following figure summarizes the main points to consider for the successful implementation of green banking and key challenges for Bangladesh. We expand the framework proposed by IFC (2018) with criteria extracted from our analysis and literature review to assess progress in each of the ingredients [109]. Figure 4 shows that Bangladesh is very strong in terms of the regulation ingredient but that the lack of fairness in the treatment of state-owned banks might be hindering the behavior change. In contrast, bank and institutions lending is way weaker despite a good portfolio of products. Finally, while we did not focus on debt capital markets, information is scarce and fragmented, suggesting this is the weakest ingredient. Based on the figure, for Bangladesh to succeed in greening finance, green loan markets and debt offerings should be strengthened, and imbalances in the take up of green banking by state-owned banks must be swiftly addressed.

6. Conclusions

The study confirms that the Bangladeshi financial sector is pioneering green banking activities since 2011. It reveals that the central bank of Bangladesh has clearly played a major role in helping to green the Bangladeshi banking system. The regulation is comprehensive, with a sustained policy focus maintained for nine years. Our analysis shows a healthy policy mix of mandatory restrictions, detailed guidance and support, and variety of opportunities such as the Green Transformation Mix. There is also a strong alignment between green banking regulation and the green growth vision underpinning the government political initiatives. Strengthening the coherence of policies and practices in the public sectors, the Central bank also sets itself as an example of in-house green practices. We suggest that in the emerging markets, the measures taken by the central banks and the level of support provided by financial supervisors have implications for long-term outcomes to achieve sustainable development goals, contributing to a just transition to a sustainable and green economy. Further research is required to assess the effectiveness of greening measures introduced by the central banks in emerging markets and examine the factors that facilitate the adoption of green banking initiatives.

For years, the financial industry in Bangladesh had lagged behind compared to regulators. However, our study highlights that banks in Bangladesh are beginning to understand the importance of introducing green banking into their mainstream operations. It also reveals differences in terms of ownership and type of activity. The differences in green performance are notable when it comes to comparing the state-owned banks versus private commercial banks. Private commercial banks are fast increasing their level of adoption of green banking and our Figure 3 suggests that if the rate of change is maintained the 5% target could be achieved within five years. On the other hand, despite huge prospects in green banking, state-owned commercial banks are far behind in terms of green banking practices. Furthermore, no bank in Bangladesh has been found in the UNEPs signatories of the Equator Principles, which is regarded as one of the most important standards for responsible financing. Further research is needed to examine the barriers to adoption of international green banking standards in emerging markets.

The negative impacts of climate change will result in significant economic consequences along with huge loss in annual GDP. Therefore, to reduce the sources of greenhouse gas emissions and to manage the associated climate change risks, there is a strong need for speedy implementation of adaptation and mitigation policies in developing countries. The central bank of Bangladesh has clearly done a good job by taking numerous initiatives in these regards. However, there are limits to what central banks can do in a context with weak market institutions. Governments have a leadership role in providing a clear transition path on which households and firms could build their investment decisions. Legislators could also help to transform the financial infrastructure. Rigorous action plans of coordinated endeavors from all concerned stakeholders can make Bangladesh more capable combating against climate change and hold a sustainable economy. Further research should look into barriers and opportunities for commercial banks to engage with green banking initiatives and the effects these initiatives have on greening the economy and economic actors.

This study uses only secondary statistical data reported from the central bank of Bangladesh. Further research should examine the performance of green banking by collecting and analyzing in-depth qualitative and quantitative data on individual bank performances and banking instruments. Regulatory frameworks for green banking and guidelines that are detailed in the review are relatively recent. Thus, further research is necessary to confirm the effectiveness and implication of these policies. Additional research may be conducted to ascertain to what extent these regulatory measures have mitigated ecologically harmful activities and, thus, overall environmental risks. The role of government in green banking could also be explored further in the future.

Author Contributions

Conceptualization—F.K., D.A.V.-B. and N.Y.; methodology—F.K.; formal analysis—F.K., investigation—F.K.; writing, F.K.; writing, D.A.V.-B.—review and editing, N.Y.; visualization, F.K.; supervision, D.A.V.-B. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Data available in a publicly accessible repository that does not issue DOIs Publicly available datasets were analyzed in this study. This data can be found here: https://www.bb.org.bd/pub/annual/anreport/ar1819/chap6.pdf.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A. Green Products Eligible for Financing by Banks and Financial Institutions in Bangladesh

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table A1.

Green Products Eligible for Financing by Banks and Financial Institutions in Bangladesh.

| Type of Sector | Sub-Sector | Type of Product/Initiative |

|---|---|---|

| Renewable Energy | Solar Energy | 1. Solar Home System |

| 2. Solar Micro/Mini Grid | ||

| 3. Solar Irrigation Pumping System | ||

| 4. Surface Water Purification Plant through Solar Pump | ||

| 5. Solar PV Assembly Plant | ||

| 6. Solar PV Plant capable ofproducing 1 MW of power or more | ||

| 7. Solar Cooker Assembly Plant | ||

| 8. Solar Water Heater Assembly Plant | ||

| 9. Solar Air Heater and Cooling System Assembly Plant | ||

| 10. Solar Energy-Driven Cold Storage | ||

| Biogas | 11. Setting up of Biogas Plant on existing Dairy and Poultry Farm | |

| 12. Integrated Cattle Rearing and Setting up of Biogas Plant | ||

| 13. Organic Manure from Slurry | ||

| 14. Mid-Range Biogas Plant | ||

| 15. Biomass-ased Large-scale Biogas Plant | ||

| 16. Poultry and Dairy-based Large-scale Biogas Plant | ||

| Wind Power | 17. Wind Energy-driven Power Plan | |

| HydroPower | 18. Hydropower (Pico, Micro and Mini) | |

| Energy Efficiency | 19. Substitution of Energy Inefficient Lighting System, Electronic Material, Boiler with | |

| Energy-Efficient Alternatives | ||

| 20. Auto Sensor Power Switch Assembly Plant | ||

| 21. Energy-Efficient Improved Cook Stove (ICS)/ICS Renewable/ Hybrid Cook Stove Assembly plant | ||

| 22. LED Bulb/Tube Manufacturing Plant | ||

| 23. LED Bulb/Tube Assembly Plant | ||

| 24. Substitution of Conventional Lime Kiln by Energy-Efficient Kiln | ||

| 25. Waste Heat Recovery System | ||

| Alternative Energy | 26. Production of Burnable Oil by the Process of Pyrolysis | |

| Waste Management | Liquid Waste Management | 27. Installation of Biological Effluent Treatment Plant (ETP) |

| 28. Installation of Combination of Biological and Chemical ETP | ||

| 29. Conversion of Chemical ETP to Combination Type (Chemical+Biological) of ETP | ||

| 30. Installation of Chemical ETP | ||

| 31. Central ETP | ||

| 32. Wastewater Treatment Plant | ||

| 33. Sewage Water Treatment Plant | ||

| Solid Waste Management | 34. Methane Recovery from Municipal Waste and to Produce Power | |

| 35. Municipal Waste to Compost | ||

| 36. Hazardous Waste Treatment Facility | ||

| 37. Fecal Sludge Treatment and Recycling Plant | ||

| Manufacturing of Recycling and Recyclable Product | 38. PET Bottle Recycling Plant | |

| 39. Plastic Waste Recycling Plant (PVC, PP, LDPE, HDPE,PS) | ||

| 40. Waste Paper Recycling Plant for Production of Recycled Paper | ||

| 41. Recyclable Baggage Manufacturing Plant (from natural raw material like bamboo) | ||

| 42. Recyclable Poly Propylene Thread and Baggage Manufacturing Plant | ||

| 43. Solar Battery Recycling Plant | ||

| 44. Used Lead Acid Battery Recycling Plant | ||

| Green (Environmentfriendly) Brick Manufacturing | 45. Compressed Block Brick | |

| 46. Foam Concrete Brick | ||

| 47. Modern Technology Brick (like Hybrid Hoffman Kiln, Vertical Shaft Brick Kiln, Zigzag Brick | ||

| Green (Environment-friendly) Establishments | 48. Green Industry or Green Building Constructed or Under Construction Accredited by USGBC-LEED, BREEAM, CASBEE, EDGE, GRIHA or any Green Building Rating System developed by SREDA, Bangladesh | |

| 49. Green-Featured Building (green Features of any building) | ||

| Miscellaneous | 50. Ensuring Safety and Work Environment (for Safety System, Disaster Management System and Health Safety System of Workers) of Factories | |

| 51. Commercial Production of Vermicompost | ||

| 52. Energy-Efficient Palm Oil Plant |

Source: Sustainable Banking Department, Bangladesh Bank, 2019.

References

- Ahmad, F.; Nurul, M.Z.; Harun, M. Factors behind the adoption of green banking by Bangladeshi commercial banks. ASA Univ. Rev. 2013, 7, 242–245. [Google Scholar]

- Mia, A.; Zhang, M.; Zhang, C.; Kim, Y. Are microfinance institutions in South-East Asia pursuing objectives of greening the environment? J. Asia Pac. Econ. 2018, 23, 229–245. [Google Scholar] [CrossRef]

- Shaumya, K.; Arulrajah, A. The impact of green banking practices on banks environmental performance: Evidence from Sri Lanka. J. Financ. Bank Manag. 2017, 5, 77–90. [Google Scholar] [CrossRef] [Green Version]

- Sahoo, P.; Nayak, B.P. Green banking in India. Indian Econ. J. 2007, 55, 82–98. [Google Scholar] [CrossRef] [Green Version]

- Shakil, M.H.; Azam, K.G.; Hossain Raju, M.S. An evaluation of green banking practices in Bangladesh. Eur. J. Bus. Manag. 2014, 6, 8–16. [Google Scholar] [CrossRef]

- Ahuja, N. Green banking in India: A review of literature. Int. J. Res. Manag. Pharm. 2015, 4, 11–16. [Google Scholar]

- Doh, J.P.; Tashman, P.; Benischke, M.H. Adapting to grand environmental challenges through collective entrepreneurship. Acad. Manag. Perspect. 2019, 33, 450–468. [Google Scholar] [CrossRef]

- Stockholm Environment Institute. Annual Report 2013; Stockholm Environment Institute US: Somerville, MA, USA, 2013; Available online: https://www.sei.org/wp-content/uploads/2017/12/sei-us-annualreport-2013.pdf (accessed on 29 January 2021).

- Oyegunle, A.; Weber, O. Development of Sustainability and Green Banking Regulations: Existing Codes and Practices; Centre for International Governance Innovation: Waterloo, ON, Canada, 2015. [Google Scholar]

- Jizi, M.I.L.; Salama, A.; Dixon, R.; Stratling, R. Corporate governance and corporate social responsibility disclosure: Evidence from the US banking sector. J. Bus. Ethics 2014, 125, 601–615. [Google Scholar] [CrossRef] [Green Version]

- Menassa, E.; Brodhäcker, M. The type and quantity of corporate social disclosures of German ‘Universal’ banks. J. Manag. Gov. 2017, 21, 119–143. [Google Scholar] [CrossRef]

- Nobanee, H.; Nejla, E. Corporate sustainability disclosure in annual reports: Evidence from UAE banks: Islamic versus conventional. Renew. Sustain. Energy Rev. 2016, 55, 1336–1341. [Google Scholar] [CrossRef]

- Thompson, P.; Christopher, J. Bringing the environment into bank lending: Implications for environmental reporting. Br. Account. Rev. 2004, 36, 197–218. [Google Scholar] [CrossRef]

- Weber, O. Sustainable Banking–History and Current Developments; School of Environment, Enterprise and Development, University of Waterloo: Waterloo, ON, Canada, 2012. [Google Scholar]

- Shaumya, K.; Arulrajah, A. Measuring green banking practices: Evidence from Sri Lanka. In Proceedings of the 13th International Conference on Business Management (ICBM), Gangodawila, Sri Lanka, 8 December 2016; pp. 1000–1011. [Google Scholar]

- Tu, T.T.R.; Nguyen, T.P.D. Factors affecting green banking practices: Exploratory factor analysis on Vietnamese banks. J. Econ. Dev. JED 2017, 24, 4–30. [Google Scholar] [CrossRef]

- Masukujjaman, M.; Aktar, S. Green banking in Bangladesh: A commitment towards the global initiatives. J. Bus. Technol. (Dhaka) 2013, 8, 17–40. [Google Scholar] [CrossRef] [Green Version]

- Hossain, D.M.; Bir, A.; Sadiq, A.T.; Tarique, K.M.; Momen, A. Disclosure of green banking issues in the annual reports: A study on Bangladeshi banks. Middle East J. Bus. 2016, 55, 1–12. [Google Scholar] [CrossRef]

- Islam, M.S.; Das, P.C. Green banking practices in Bangladesh. IOSR J. Bus. Manag. 2013, 8, 39–44. [Google Scholar] [CrossRef]

- Lalon, R.M. Green banking: Going green. Int. J. Econ. Financ. Manag. Sci. 2015, 3, 34–42. [Google Scholar]

- Jeucken, M.H.A.; Bouma, J.J. The Changing Environment of Banks. Greener Manag. Int. 1999, 27, 21–36. [Google Scholar] [CrossRef]

- Yadav, R.; Pathak, G. Environmental sustainability through green banking: A study on private and public sector banks in India. OIDA Int. J. Sustain. Dev. 2013, 6, 37–48. [Google Scholar]

- Dash, R.N. Sustainable ‘Green’ Banking: The story of Triodos Bank. Cab Call. 2008, 5, 26–29. [Google Scholar]

- Zitti, M.; Ferrara, C.; Perini, L.; Carlucci, M.; Salvati, L. Long-term urban growth and land use efficiency in Southern Europe: Implications for sustainable land management. Sustainability 2015, 7, 3359–3385. [Google Scholar] [CrossRef] [Green Version]

- Ciocoiu, C.N. Integrating digital economy and green economy: Opportunities for sustainable development. Theor. Empir. Res. Urban Manag. 2011, 6, 33–43. [Google Scholar]

- Mundaca, L.; Markandya, A. Assessing regional progress towards a ‘Green Energy Economy’. Appl. Energy 2016, 179, 1372–1394. [Google Scholar] [CrossRef]

- United Nations Environment Programme (UNEP). Towards A Green Economy: Pathways to Sustainable Development and Poverty Eradication—A Synthesis for Policy Makers; UNEP: Nairobi, Kenya, 2011. [Google Scholar]

- Vazquez-Brust, D.; Smith, A.M.; Sarkis, J. Managing the transition to critical green growth: The ‘Green Growth State’. Futures 2014, 64, 38–50. [Google Scholar] [CrossRef]

- Bihari, S.C.; Pandey, B. Green banking in India. J. Econ. Int. Financ. 2015, 7, 1–17. [Google Scholar]

- Rifat, A.; Nisha, N.; Iqbal, M.; Suviitawat, A. The role of commercial banks in green banking adoption: A Bangladesh perspective. Int. J. Green Econ. 2016, 10, 226–251. [Google Scholar] [CrossRef]

- Alexander, K. Greening Banking Policy; Support of the G20 Green Finance Study Group: Zürich, Switzerland, 2016. [Google Scholar]

- Singh, H.; Singh, B.P. An effective & resourceful contribution of green banking towards sustainability. Int. J. Adv. Eng. Sci. Technol. 2012, 1, 41–45. [Google Scholar]

- Jha, N.; Bhome, S. A study of green banking trends in India. Int. Mon. Ref. J. Res. Manag. Technol. 2013, 2, 127–132. [Google Scholar]

- Karunakaran, R. Green Banking–An Avenue to Safe Environment. Galaxy Int. Interdiscip. Res. J. 2014, 2, 144–153. [Google Scholar]

- Nath, V.; Nayak, N.; Goel, A. Green banking practices–A review. IMPACT: Int. J. Res. Bus. Manag. 2014, 2, 45–62. [Google Scholar]

- Bhardwaj, B.R.; Malhotra, A. Green banking strategies: Sustainability through corporate entrepreneurship. Greener J. Bus. Manag. Stud. 2013, 3, 180–193. [Google Scholar] [CrossRef] [Green Version]

- Tara, K.; Singh, S.; Kumar, R. Green banking for environmental management: A paradigm shift. Curr. World Environ. 2015, 10, 1029–1038. [Google Scholar] [CrossRef]

- Bahl, S. Green banking-The new strategic imperative. Asian J. Res. Bus. Econ. Manag. 2012, 2, 176–185. [Google Scholar]

- Rahman, M.; Ahsan, M.; Hossain, M.; Hoq, M. Green banking prospects in Bangladesh. Asian Bus. Rev. 2013, 2, 59–63 and 117–121. [Google Scholar] [CrossRef] [Green Version]

- Chowdhury, M.A.A.; Dey, M. Green Banking Practices in Bangladesh. Cost Manag. 2016, 44, 34–39. [Google Scholar]

- European Banking Federation. Briefing Note: Greening the Financial System: Exploring the Ways Forward; European Banking Federation: Brussels, Belgium, 2017; Available online: https://www.ebf.eu/ebf-media-centre/briefing-note-greening-the-financial-system-october-2017/ (accessed on 23 December 2020).

- International Finance Corporation (IFC). Green Finance: A Bottom-up Approach to Track Existing Flows; International Finance Corporation: Washington, DC, USA, 2016; Available online: https://www.ifc.org/wps/wcm/connect/3218ea9e-e479-4ddd-b6c7-d51de1f73d16/Green+Finance_Bottom+up+approach_ConsultDraft.pdf?MOD=AJPERES&CVID=lyS6ShT. (accessed on 23 December 2020).

- Jayawardhena, C.; Foley, P. Changes in the banking sector–the case of Internet banking in the UK. Internet Res. 2000, 10, 19–31. [Google Scholar] [CrossRef]

- Wang, Y. What are the biggest obstacles to growth of SMEs in developing countries?—An empirical evidence from an enterprise survey. Borsa Istanb. Rev. 2016, 16, 167–176. [Google Scholar] [CrossRef] [Green Version]

- Helleiner, E.; Pagliari, P. The end of an era in international financial regulation? A postcrisis research agenda. Int. Organ. 2011, 65, 169–200. [Google Scholar] [CrossRef]

- Mezher, T.; Jamali, D.; Zreik, C. The role of financial institutions in the sustainable development of Lebanon. Sustain. Dev. 2002, 10, 69–78. [Google Scholar] [CrossRef]

- Scholtens, B. Corporate social responsibility in the international banking industry. J. Bus. Ethics 2009, 86, 159–175. [Google Scholar] [CrossRef]

- Hasan, M. Missing green financing target to affect banks, NBFI ratings. Dhaka Tribune. 2020. Available online: https://www.dhakatribune.com/business/banks/2020/09/09/missing-green-financing-target-to-affect-banks-nbfi-ratings (accessed on 24 December 2020).

- Weber, O.; Diaz, M.; Schwegler, R. Corporate social responsibility of the financial sector–strengths, weaknesses, and the impact on sustainable development. Sustain. Dev. 2014, 22, 321–335. [Google Scholar] [CrossRef]

- Pintér, É.; Deutsch, N.; Ottmár, Z. New Direction Line of Sustainable Development and Marketing in Green Banking. 22nd IMP Conference in Milan, Italy, 2006. Available online: https://www.impgroup.org/paper_view.php?viewPaper=5671 (accessed on 23 December 2020).

- Schmidheiny, S.; Zorraquin, F.J. Financing Change: The Financial Community, Eco-efficiency, and Sustainable Development; MIT Press: Cambridge, MA, USA, 1998. [Google Scholar]

- Meena, R. Green banking: As initiative for sustainable development. Glob. J. Manag. Bus. Stud. 2013, 3, 1181–1186. [Google Scholar]

- Wendt, K. (Ed.) Responsible Investment Banking: Risk Management Frameworks, Sustainable Financial Innovation and Softlaw Standards; Springer: Berlin, Germany, 2015. [Google Scholar]

- Volz, U.; Böhnke, J.; Knierim, L.; Richert, K.; Roeber, G.M.; Eidt, V. Financing the Green Transformation: How to Make Green Finance Work in Indonesia; Springer: Berlin, Germany, 2015. [Google Scholar]

- Volz, U. Fostering Green Finance for Sustainable Development in Asia; Asian Development Bank Institute: Tokyo, Japan, 2018. [Google Scholar]

- Asian Development Bank (ADB). Asian Development Bank Sustainability Report 2018: Investing for An Asia and The Pacific Free of Poverty; Asian Development Bank: Mandaluyong, Philippines, 2018; Available online: https://www.adb.org/documents/asian-development-bank-sustainability-report-2018 (accessed on 23 December 2020).

- Durbin, A.; Steve, H.; Hunter, D.; Peck, J. Sustainable Finance—Moving from Paper Promises to Performance: Bank Track; World-Wide Fund for Nature (WWF): Godalming Surrey, UK, 2006. [Google Scholar]

- Perez, O. The New Universe of Green Finance: From Self-Regulation to Multi-Polar Governance; Hart Publishing: Oxford, UK, 2007. [Google Scholar]

- UNEP Financial Initiatives, WWF and GIAN. Innovative Financing for Sustainable Small and Medium Enterprises in Africa; Meeting Report; International Workshop: Geneva, Switzerland; United Nations Environment Programme Finance Initiative: Nairobi, Kenya, 2008; Available online: https://thegiin.org/research/publication/innovative-financing-for-sustainablesmall-and-medium-enterprises-in-africa (accessed on 23 December 2020).

- Bai, Y. Financing a Green Future: An Examination of China’s Banking Sector for Green Finance. Master Thesis, Lund University, Lund, Sweden, 2011. [Google Scholar]

- Carè, R. Emerging Practices in Sustainable Banking. In Sustainable Banking; Carè, R., Ed.; Palgrave Pivot: London, UK, 2018; pp. 65–92. [Google Scholar]

- International Organization of Securities Commissions. Annual Report; International Organization of Securities Commissions: Madrid, Spain, 2019; Available online: https://www.iosco.org/annual_reports/2019/pdf/annualReport2019.pdf (accessed on 23 December 2020).

- Bank of England Prudential Regulation Authority. The Impact of Climate Change on the UK Insurance Sector; A Climate Change Adaptation Report; Bank of England: London, UK, 2015; Available online: https://www.bankofengland.co.uk/-/media/boe/files/prudential-regulation/publication/impact-of-climate-change-on-the-uk-insurance-sector.pdf (accessed on 23 December 2020).

- Carney, M. Breaking the Tragedy of the Horizon–Climate Change and Financial Stability; Speech given at Lloyd’s of London; Bank of England: London, UK, 2015; Available online: https://www.bankofengland.co.uk/speech/2015/breaking-the-tragedy-of-the-horizon-climate-change-and-financial-stability (accessed on 23 December 2020).

- Dikau, S.; Ryan-Collins, J. Green Central Banking in Emerging Market and Developing Country Economies; New Economics Foundation: London, UK, 2017; pp. 18–22. Available online: https://eprints.soas.ac.uk/24876/ (accessed on 23 December 2020).

- Batten, S.; Sowerbutts, R.; Tanaka, M. Let’s Talk About the Weather: The Impact of Climate Change on Central Banks; Staff Working Papers; Bank of England: London, UK, 2016. [Google Scholar]

- Carney, M. Fifty shades of green. Financ. Dev. 2019, 56, 12–15. [Google Scholar]

- Volz, U. On the role of central banks in enhancing green finance. Inquiry Working Paper; United Nations Environment Programme: Nairobi, Kenya, 2017. [Google Scholar]

- Sachs, J.; Woo, W.T.; Yoshino, N.; Taghizadeh-Hesary, F. Handbook of Green Finance: Energy Security and Sustainable Development; Springer: Singapore, 2019. [Google Scholar]

- McDaniels, J.; Robins, N. Greening the Rules of the Game: How Sustainability Factors Are Being Incorporated into Financial Policy and Regulation; UNEP Inquiry into the Design of a Sustainable Financial System: Geneva, Switzerland, 2018. [Google Scholar]

- Dikau, S.; Volz, U. Central Bank Mandates, Sustainability Objectives and the Promotion of Green Finance; SOAS Department of Economics Working Paper No. 232; School of Asian and African Studies: London, UK, 2020. [Google Scholar]

- Campiglio, E.; Dafermos, Y.; Monnin, P.; Ryan-Collins, J.; Schotten, G.; Tanaka, M. Climate change challenges for central banks and financial regulators. Nat. Clim. Chang. 2018, 8, 462–468. [Google Scholar] [CrossRef]

- Alexander, K. Stability and Sustainability in Banking Reform: Are Environmental Risks Missing in Basel III? United Nations Environment Programme Financial Initiative and University of Cambridge Institute for Sustainability Leadership (CISL): Cambridge, UK, 2014; Available online: https://www.cisl.cam.ac.uk/resources/sustainable-finance-publications/banking-regulation (accessed on 24 December 2020).

- Ward, M.; Naude, R. Banking for a Sustainable Economy; Working Paper; Centre for Researching Education and Labour (REAL), University of Witwatersrand: Johannesburg, South Africa, 2018. [Google Scholar]

- Park, H.; Kim, J.D. Transition towards green banking: Role of financial regulators and financial institutions. Asian J. Sustain. Soc. Responsib. 2020, 5, 1–25. [Google Scholar] [CrossRef]

- Network for Greening the Financial System (NGFS). Climate Scenarios for Central Banks and Supervisors; Network for Greening the Financial System, Banc De France: Paris, France, 2020; Available online: https://www.ngfs.net/sites/default/files/medias/documents/820184_ngfs_scenarios_final_version_v6.pdf (accessed on 24 December 2020).

- Task Force of Climate-Related Financial Disclosures. Final Report: Recommendations of the Task Force on Climate-Related Financial Disclosures; Financial Stability Board, Task Force on Climate-related Financial Disclosures: Basel, Switzerland, 2017; Available online: https://assets.bbhub.io/company/sites/60/2020/10/FINAL-2017-TCFD-Report-11052018.pdf (accessed on 24 December 2020).

- Johnston, M.P. Secondary data analysis: A method of which the time has come. Qual. Quant. Methods Libr. 2017, 3, 619–626. [Google Scholar]

- G20 Green Finance Study Group. G20 Green Finance Synthesis Report, 2016. Available online: https://unepinquiry.org/wp-content/uploads/2016/09/Synthesis_Report_Full_EN.pdf (accessed on 24 December 2020).

- Stewart, D.W.; Kamins, M.A. Introduction Secondary Research. In Sage Secondary Data Analysis; Goodwin, J., Ed.; Sage: London, UK, 1993; pp. 151–163. [Google Scholar]

- World Bank. World Bank Annual Report 2018; World Bank: Washington, DC, USA, 2018; Available online: http://documents1.worldbank.org/curated/en/630671538158537244/pdf/The-World-Bank-Annual-Report-2018.pdf (accessed on 24 December 2020).

- World Bank. Climate Finance; World Bank: Washington, DC, USA, 2019; Available online: https://www.worldbank.org/en/topic/climatefinance (accessed on 24 December 2020).

- Crippa, M.; Oreggioni, G.; Guizzardi, D.; Muntean, M.; Schaaf, E.; Lo Vullo, E.; Vignati, E. Fossil CO2 and GHG Emissions of All World Xountries; Publication Office of the European Union: Luxemburg, 2019. [Google Scholar]

- Millat, K.M.; Chowdhury, R.; Singha, E.A. Green Banking in Bangladesh: Fostering Environmentally Sustainable Inclusive Growth Process; Department of Communications and Publications, Bangladesh Bank: Dhaka, Bangladesh, 2013. [Google Scholar]

- Hossain, M. Green Finance in Bangladesh: Policies, Institutions, and Challenges. Asian Development Bank Institute Working Paper. 2018, p. 892. Available online: https://www.adb.org/sites/default/files/publication/467886/adbi-wp892.pdf (accessed on 24 December 2020).

- International Monetary Fund. Country Report, Bangladesh: Selected Issues; International Monetary Fund: Washington, DC, USA, 2019; Available online: https://www.imf.org/~/media/Files/Publications/CR/2019/1BGDEA2019002.ashx (accessed on 24 December 2020).

- Hoque, N.; Mowla, M.; Uddin, M.S.; Mamun, A.; Uddin, M.R. Green Banking Practices in Bangladesh: A Critical Investigation. Int. J. Econ. Financ. 2019, 11, 58–68. [Google Scholar] [CrossRef]

- Rosenzweig, C.; Jones, J.W.; Hatfield, J.L.; Ruane, A.C.; Boote, K.J.; Thorburn, P.; Winter, J.M. The agricultural model intercomparison and improvement project (AgMIP): Protocols and pilot studies. Agric. Forest Meteorol. 2013, 170, 166–182. [Google Scholar] [CrossRef] [Green Version]

- Climate Analytics. Country Profile Bangladesh: Decarbonizing South and South East Asia; Climate Analytics: New York, NY, USA, 2019; Available online: https://climateanalytics.org/media/decarbonisingasia2019-profile-bangladesh-climateanalytics.pdf (accessed on 23 December 2020).

- Murcott, S. Arsenic Contamination in the World; IWA Publishing: London, UK, 2012. [Google Scholar]

- World Health Organization (WHO). The Cost of a Polluted Environment: 1.7 Million Child Deaths a Year; World Health Organization: Rome, Italy, 2017; Available online: https://www.who.int/news/item/06-03-2017-the-cost-of-a-polluted-environment-1-7-million-child-deaths-a-year-says-who (accessed on 23 December 2020).

- United Nations Environment Programme (UNEP). United Nations Environment Programme (UNEP); UNEP: Nairobi, Kenya, 2019; Available online: https://sdgs.un.org/un-system-sdg-implementation/united-nations-environment-programme-unep-24515 (accessed on 23 December 2020).

- Rahman, M.R.; Lateh, H. Climate change in Bangladesh: A spatio-temporal analysis and simulation of recent temperature and rainfall data using GIS and time series analysis model. Theor. Appl. Climatol. 2017, 128, 27–41. [Google Scholar] [CrossRef]

- Toufique, K.A.; Islam, A. Assessing risks from climate variability and change for disaster-prone zones in Bangladesh. Int. J. Disaster Risk Reduct. 2014, 10, 236–249. [Google Scholar] [CrossRef]

- Ministry of Environment, Forest and Climate Change Government of the People’s Republic of Bangladesh. Third National Communication of Bangladesh to the United Nations Framework Convention on Climate Change; Ministry of Environment, Forest and Climate Change Government of the People’s Republic of Bangladesh Building: Dhaka, Bangladesh, 2018; Available online: https://unfccc.int/sites/default/files/resource/TNC%20Report%20%28Low%20Resolation%29%2003_01_2019.pdf (accessed on 23 December 2020).

- Bhuiyan, M.A.H.; Hassan, S.; Darda, M.A.; Habib, M.W.; Hossain, M.B. Government Initiatives for Green Development in Bangladesh. Available online: https://www.preprints.org/manuscript/202008.0298/v1 (accessed on 23 December 2020).

- Bangladesh Bank. Quarterly Review report on Green Banking Activities of Banks and Financial Institutions and Green Refinance Activities of Bangladesh Bank; Bangladesh Bank: Dhaka, Bangladesh, 2020; Available online: https://www.bb.org.bd/pub/publictn.php# (accessed on 23 December 2020).