Funding Sustainable Cities: A Comparative Study of Sino-Singapore Tianjin Eco-City and Shenzhen International Low-Carbon City

1

School of Economics and Management, Fuzhou University, No. 2, Xueyuan Road, Minhou, Fuzhou 350108, China

2

Faculty of Technology, Policy and Management, Delft University of Technology, Jaffalaan 5, 2600 GA Delft, The Netherlands

3

School of International Relations and Public Affairs, Fudan University, 220 Handan Road, Shanghai 200433, China

4

Rotterdam School of Management, Erasmus University Rotterdam, Postbus 1738, 3000 DR Rotterdam, The Netherlands

*

Author to whom correspondence should be addressed.

Sustainability 2018, 10(11), 4256; https://doi.org/10.3390/su10114256

Submission received: 26 October 2018

/

Revised: 13 November 2018

/

Accepted: 14 November 2018

/

Published: 17 November 2018

(This article belongs to the Section Sustainable Urban and Rural Development)

Abstract

:China has gone through a rapid process of urbanization, but this has come along with serious environmental problems. Therefore, it has started to develop various eco-cities, low-carbon cities, and other types of sustainable cities. The massive launch of these sustainable initiatives, as well as the higher cost of these projects, requires the Chinese government to invest large sums of money. What financial toolkits can be employed to fund this construction has become a critical issue. Against this backdrop, the authors have selected Sino-Singapore Tianjin Eco-city (SSTEC) and Shenzhen International Low-Carbon City (ILCC) and compared how they finance their construction. Both are thus far considered to be successful cases. The results show that the two cases differ from each other in two key aspects. First, ILCC has developed a model with less financial and other supports from the Chinese central government and foreign governments than SSTEC, and, hence, may be more valuable as a source of inspiration for other similar projects for which political support at the national level is not always available. Second, by issuing bonds in the international capital market, SSTEC singles itself out among various sustainable initiatives in China, while planning the village area as a whole and the metro plus property model are distinct practices in ILCC. In the end, the authors present a generic financing model that considers not only economic returns but also social and environmental impacts to facilitate future initiatives to finance in more structural ways.

1. Introduction

Hundreds of millions of people have migrated from rural areas to cities in China since the implementation of the reform and opening-up policy, which is unprecedented in human history [1], and this trend continues. It is estimated that approximately one billion Chinese people will live in cities in 2030 [2]. This trend challenges both central and local governments to mobilize limited financial resources to provide public goods and services, such as sustainable energy and green infrastructure, to their citizens. The rapid demographic and economic growth alongside this urbanization trend is also one of the causes for the environmental problems the world faces. As such, researchers and practitioners attempt to solve the problem by incorporating an environmental factor into urban development. In 2003, the ‘U.K. Energy White Paper: Our Energy Future—Creating a Low Carbon Economy’ was published by the U.K. government, leading to the launch of low-carbon and eco initiatives all over the world. Echoing the U.K.’s initiative, China has vigorously developed sustainable cities (we use ‘sustainable cities’ as the umbrella term to stand for eco cities, low-carbon cities, and eco low-carbon cities, since, in the literature, ‘sustainable cities’ is the term that most frequently co-occurs with other various terms for cities [3]) to change the ways of economic development and thus reduce the negative impacts of various economic activities on the environment. Some projects have seen rapid progress in their implementation thus far, which is evidenced by the cases of Sino-Singapore Tianjin Eco-City (SSTEC) and Shenzhen International Low Carbon City (ILCC). However, most of these projects are not as successful as expected because of planning, governance, and financial issues. For instance, Shanghai Dongtan Eco-city has been indefinitely suspended because of land use rights and financial problems [4]. In addition, the construction of ecological housing and the transition to a low-carbon economy result in higher transition and usage costs. As such, the question of who would eventually bear the costs also becomes a problem that initiators need to take into consideration [5].

The International Consensus on the Sustainable Development Goals and the 2030 Agenda underscore the need to find long-term solutions for addressing the challenges in funding sustainable development. It is projected that an annual investment of U.S. $5–7 trillion will be required to achieve the sustainable development goals, covering infrastructure, water supply, clean energy, sanitation, and agriculture [6]. Of this, developing countries need roughly U.S. $3.9 trillion. However, only U.S. $1.4 trillion has been reserved, while the remaining U.S. $2.5 trillion requires additional public and private funds. Public funds, such as fiscal funds, supply only a small proportion of the total investment amount. As such, the study of how to provide financial support for the construction of sustainable cities has become a core consideration for academics and policy-makers. For example, Baeumler and Mehndiratta [7] argue that balancing financial instruments and incentives is critical for the construction of sustainable cities. The Research Institute for Fiscal Science Ministry of Finance P.R. China [8] studies the significant role of finance in addressing climate change from an institutional angle. The research group indicates that fiscal policies play a guiding role in approaching the climate change issue, since authorities can employ positive and negative incentives to handle the various environmental impacts each project causes. Positive incentives, such as tax exemptions or subsidies, encourage investors to carry out their business activities by taking into account the environmental issue, while sanctions increase investors’ costs and internalize negative externalities, which makes investors think twice about their investment [9,10,11]. As a consequence, it is vital to explore which financial toolkits can be employed to finance the construction of sustainable projects.

Against this backdrop, we compare the financial instruments that SSTEC and ILCC, two sustainable city projects with a good reputation in China, employ to fund their construction. This article aims at addressing the following questions. (1) What are the similarities and differences in financing vehicles between Shenzhen International Low Carbon City and Sino-Singapore Tianjin Eco-City? (2) What roles do the involved stakeholders play in providing stable funding for the construction? (3) Which financial toolkits can be employed by other sustainable cities in China and globally?

The contribution of this research is twofold. On the one hand, it enriches the research on financing sustainable cities. On the other hand, addressing the above issues provides policy-makers with heuristics on how to finance the construction of sustainable cities by demonstrating a generic model based on the experience summarized from the comparison of the Tianjin and Shenzhen cases. Funding sustainable cities is a means to spur sustainable growth, which aligns with the battle against global warming.

The rest of this article is structured as follows. Section 2 offers the state-of-the-art in terms of financial instruments for urban development, and is followed by the methodology in Section 3. Section 4 briefly demonstrates the profiles of the two cases to provide background information for the comparative analysis in the following sections. Section 5 compares the financing instruments that the Shenzhen and Tianjin projects employed as well as the roles various actors played in the two projects. Based on the comparative study, a generic financing model is developed to facilitate sustainable initiatives to deal with financial problems. Section 6 concludes the research.

2. Financial Instruments for Urban Development: Taking Stock

With the development of the economy, countries tend to take environmental issues more and more seriously and seek to transition their economy into a more sustainable direction. This trend thus poses new challenges for local authorities in funding various sustainable projects. Therefore, both researchers and practitioners have tried hard to explore new financial instruments that can be employed to expand the sources of finance. Merk et al. [12] argue that the main financial instruments in the principal green urban sectors include taxes, user fees, grants, Public–private Partnerships (PPPs), land-based income, loans, bonds, and carbon finance. These financial instruments are used to finance the development of transportation, buildings, water/waste, and energy. Inman [13] holds the view that local public services can be funded through user fees, resident-based taxation, and business-based land value taxes. Of these, user fees can be applied to both residential and business services, resident-based taxation is adopted to finance residential services, and business-based land value taxes are applicable to business services. Slack [14] presents some financial instruments for large cities, including user charges, tax, intergovernmental transfers, borrowing, PPPs and development charges. Bahl and Linn [15] divide financial instruments into own-source financing and external sources on the basis of financial sources. Own-source financing includes user changes and betterment levies, property taxation, and non-property taxes, while external sources encompass intergovernmental transfers, borrowing, PPPs, and international aid. Z/YenGroup [16] systematically explores financial instruments for financing sustainable infrastructures in cities. The research group identifies three instruments in general, namely, public finance, debt finance, and equity finance. To be specific, public finance instruments include land sales, land or infrastructure asset leaseholds, PPPs and Private-finance initiatives (PFIs), taxes, land value capture mechanisms, user charges and fees, grants and subsidies, building rights, and planning permits. Debt finance instruments encompass loans and bonds, de-risking and credit enhancement instruments, and debt refinancing instruments. Equity finance instruments consist of listed infrastructure equities, listed/unlisted equity funds, and equity-funded direct investments (e.g., special purpose vehicles and joint ventures) in infrastructure. Panayotou [17] takes stock of the available economic instruments for financing sustainable development, covering property rights, market creation, fiscal instruments, charging systems, financial instruments, liability systems, and performance bonds and deposit-refund systems. He [17] further identifies economic and financing instruments that can be employed for securing the global commons, including global environmental financing institutions, international environmental taxation, transferable development rights, internationally tradable emission permits, joint implementation and carbon offsets, and the clean development mechanism. Bäckstrand [18] stresses the important role of global partnerships in funding sustainable development. His study indicates that local governments can benefit from the Johannesburg partnerships by having a clearer connection to existing institutions and multilateral agreements and improving the effectiveness of local governance [18]. Olsen [19] proposes response strategies to key environmental challenges and divides them up into short-term, medium-term and long-term strategies. Of these, short-term strategies include dedicated investment funds, premium purchasing, mixed credits, and capacity development; medium-term strategies cover Green Investment Schemes, supporting unilateral clean development mechanism (CDM) and small-scale projects, and exploring ways to transfer climate change mitigation into sector programs; and long-term strategies should be negotiated in advance to reduce risks that bring about uncertainties. Instead of directly exploring financial instruments, Meltzer [20] discusses how to use concessional climate finance to facilitate the development of low-carbon resilient infrastructure projects. Methods include (1) developing an enabling environment and co-financing packages; (2) supporting local banks, the development of financial instruments, and low-carbon technology; (3) strengthening the monitoring of outcomes; and (4) improving cooperation between climate funds. Some researchers argue that whether general fiscal investment and innovative financing strategies show long-term effectiveness depends on the following criteria: ‘adequacy, stability, efficiency, equity, ease of implementation, and political acceptability’ [21].

Many researchers explore financial vehicles that can be used to finance the construction of sustainable cities, yet the identified financial instruments do not play equal roles in the amount of funds they bring to the table. Bahl and Linn [15] concluded that debt finance, PPPs, and land-based levies are effective instruments to finance urban construction; intergovernmental transfers and grant finance are of paramount importance; and user charges and property taxes are critical yet underused. In general, the financial instruments that large cities adopt should be in line with their responsibilities in providing infrastructure and services [14]. Many researchers shed light on mobilizing private capital in that the involvement of private sectors can alleviate local authorities’ financial pressure [14,22]. Therefore, local authorities should pay attention to the needs and interests of private investors [23] and provide political support to enabling conditions that involve private parties [24,25]. Some researchers, such as Reichelt [26] and Sullivan et al. [23], hold the view that PPPs and bonds are two effective means to allow the private sector to participate in the development of climate-related projects. PPPs have been widely drawn upon to finance projects in many fields. However, practitioners need to overcome many difficulties when they apply PPPs, particularly in developing countries. In terms of bonds, the money raised through green bonds only accounts for a small percentage of the projected amount that is required to fill the gap that green projects cause [26]. Still, the green bond market is booming in China, for which the amount raised through green bonds has grown from $1 billion in 2007 to over $41 billion in 2015 [27]. To unlock the potential of green bonds, dialogues between policy-makers and stakeholders should be strengthened to clear away barriers and improve information transparency [28].

The reviewed literature has suggested various methods to bridge the financial gap, yet they are scattered. There is no general model taking into account the sustainability of financial vehicles for urban development. To fill this research gap, this study offers a model to bring different financial vehicles together by taking non-financial factors into account, making financial vehicles more resilient in future financing activities.

3. Methodology

We relied on both desk research and interviews for data collection. As for desk research, the information was retrieved from the academic literature, SSTEC and ILCC’s websites, and other web-based reports, e.g., auditing reports and working papers that have been published by the World Bank and the United Nations Environmental Program. In addition, we interviewed 20 people in total whose work is closely related to the two projects. Of these, 11 interviewees were working in or with SSTEC in the period April–July 2015, including officials, developers, financial staff, and project managers. In February 2016, we revisited the SSTEC site and stayed there for one week to collect additional information. We also visited the ILCC site in the period February–March 2016 and interviewed nine people working in or with ILCC. The first author conducted the interviews, and the language was Chinese. The interviewee’s names are not presented due to confidentiality.

In addition, the research drew on the authors’ earlier work, including the two most recent and direct companion articles Zhan & de Jong [29] and Zhan & de Jong [30]. The two articles were about how sustainable cities were financed in Tianjin and Shenzhen, respectively. Based on the similarities and differences across the two cases, lessons were drawn to benefit other sustainable cities.

4. An Overview of the Tianjin and Shenzhen Projects

ILCC is a demonstration program and a collaboration between China and the European Union (E.U.) on sustainable urbanization, aimed at displaying China’s achievements in low-carbon technology. ILCC was launched in 2012 and covers a planned area of 53.4 km2. It is located in the Longgang District, Shenzhen, China, at the border of Dongguan and Huizhou in Guangdong province [31]. Currently, the economy in Pingdi is still underdeveloped, while the carbon emission levels are high. As a flagship project of the China–E.U. Partnership on Sustainable Urbanization, the Shenzhen municipality is trying its best to develop ILCC into a pilot area to realize a great leap forward in urban developmental planning under the concept of integrating industry with the city, green urban management, and benefit sharing under the constraints of carbon indicators to eventually provide replicable pathways for low-carbon development in future urbanization [32].

Sino-Singapore Tianjin Eco-city is a project that was launched as a collaboration between the Chinese and Singaporean governments. In November 2007, the Framework Agreement between People’s Republic of China and Republic of Singapore about Building an Eco-City in the People’s Republic of China and Supplementary Agreement of this framework was signed. It was a new highlight and key project between the two countries following the establishment and development of the Suzhou Industrial Park. Sino-Singapore Tianjin Eco-City aims to develop itself into a new city that is economically vibrant, environmentally friendly, resource-efficient, and socially harmonious, and to provide a reference for other cities in China [33].

To give an overall picture of the two cities, Table 1 displays a profile for each of Tianjin and Shenzhen. From the table, we learn that the Tianjin project started in 2007, which was five years earlier than the Shenzhen project. SSTEC covers 30 km2, 23.4 km2 less than ILCC. However, SSTEC is built in an area consisting of salt pans, saline-alkaline non-arable land, and polluted water bodies. Each component takes up one-third of the land. The construction of SSTEC has a symbolic meaning both in China and elsewhere, since the Tianjin project builds a city from scratch. In contrast, ILCC is built on an existing city, but makes the transition by upgrading its industries to lower-carbon-emission industries. The differences in these aspects require the central government to be involved in the construction of SSTEC to a larger extent than in the Shenzhen project.

5. Analysis

5.1. Comparing the Financial Vehicles the Two Projects Employ

Financing sustainable urban development has become a major issue, especially in Asian countries where the size and scale of construction efforts are vast. Here, we compare the cases of ILCC and SSTEC to identify the similarities and differences in the financing vehicles that they employ (see Table 2).

5.1.1. Similarities in Financing Vehicles

ILCC uses bank loans and corporate bonds to provide funds for its construction, which are employed by SSTEC as well. Although SSTEC and ILCC both draw upon bank loans and corporate bonds to finance their construction, they differ from each other. For instance, bank loans and corporate bonds in Shenzhen are carried out in the name of the Shenzhen Special Zone Construction and Development Group Co., Ltd. (CDG), which is a financing platform of Shenzhen Municipality. In contrast, bank loans and corporate bonds in Tianjin’s case are arranged through Tianjin Eco-city Investment and Development Co., Ltd. (TEID), which has been regarded as an innovation of the Tianjin project since TEID has six stakeholders and separates the functions of local authorities from the company [29]. Regarding bank loans, both projects have a close connection with banks, so they can obtain large loan sums. For example, TEID is strongly backed by the public sector, which is helpful for the company in obtaining bank loans because government-backed projects are regarded as more reliable [34]. In addition, TEID cooperates with 12 banks, diversifying the sources for obtaining bank loans. As for ILCC, CDG plays an instrumental role in acquiring bank loans. CDG, as a financing platform, helps the government raise funds for its construction. Shenzhen Municipality packed the prime assets of its state-owned corporations to found CDG, which is conducive to CDG’s obtaining bank loans. Seen from this aspect, the two projects are similar.

5.1.2. Differences in Financing Vehicles

However, the corporate bonds issued by the two corporations are different. CDG issues bonds in the Chinese capital market, while TEID issues bonds in the Singaporean capital market except for in China. It was the first time that a Tianjin-based non-financial company issued bonds in the international capital market, which is one of ILCC’s major contributions in funding sustainable cities [35,36]. Issuing bonds in the international capital market not only reduces financial costs but also sets an example for other non-financial companies to raise money for sustainable projects internationally by issuing bonds.

The two cases also differ from each in arranging PPP. They both make use of international funds and domestic private funds, yet they vary in the detail. Foreign capital in the Tianjin case is predominantly from Singapore, including the Singaporean consortium led by Keppel Corporation, other Singapore-based companies, and the public in Singapore. However, ILCC has more diversified international cooperation. It originally wanted to utilize the same strategy as the Tianjin project to finance its construction. In particular, Shenzhen Municipality wanted the Dutch government to invest money in ILCC, yet it did not succeed in introducing the strategic partner, since the Dutch party just wanted to play a consultancy role in the construction [37]. Shenzhen Municipality has, since then, tried to diversify its partners by introducing companies from Germany, the Netherlands, Japan, and America [38]. This was one of the reasons for Shenzhen Municipality to change the low-carbon city’s name from Sino-Dutch Low-Carbon City into Shenzhen International Low-Carbon City [32].

As a component of its PPP arrangement, Shenzhen makes use of planning the village area as a whole (PVAW) and the ‘metro plus property’ model to fund the low-carbon city, which are regarded as two innovations of the Shenzhen case in financing its construction. On the one hand, PVAW is a new means to consolidate and reserve land taking into account the benefits of aboriginal residents, small enterprises, and other scattered landowners. PVAW does not merely give monetary compensation to landowners in ILCC but also allows them to participate in the construction by contributing their land. In the process, the benefits of different stakeholders have been balanced, and thus social conflicts have been alleviated. On the other hand, the ‘metro plus property’ model offers another option for local authorities to arrange financial issues. Local authorities grant the franchise to a subway company, allowing it to construct and operate the metro. Meanwhile, local authorities allow the subway company to develop real estate along the line to subsidize the loss that metro construction causes. This practice adds value to the real estate around metro stations due to the convenience of transportation while the prosperous real estate, in its turn, boosts the traveler flow and thus increases the revenue of the subway company. With the help of PVAW and ‘metro plus property’, private parties have been mobilized to participate in the construction of ILCC, which relieves the financial burden of local authorities. PVAW reduces local government’s expenditure in expropriating lands while the ‘metro plus property’ model decreases local government’s costs in building the metro.

The differences in finance between the two cases also include the assistance from national and international authorities and organizations. It plays an instrumental role in funding SSTEC, yet the amount in ILCC is so limited that it can be ignored.

5.2. Stakeholders Involved in the Two Cases

The literature includes an extensive discussion on how international, national, and subnational actors and the balance of their benefits in the construction of sustainable cities influence the sustainable financing in the two cities [29,30,39]. Since sustainable cities are long-term and huge investment projects, the risks associated with investing in them are also high. As such, it is of paramount importance to balance the interests of different stakeholders.

The key to success is the active participation of actors from financial institutions, including central banks, regulators and prudential official institutions, standard-setters, governmental departments (including the ministry of finance), and market-based rule makers (including stock exchanges and credit rating agencies). Other participants also play an instrumental role in the construction of sustainable cities. Market-based participants are banks, pension funds, and analysts. They participate in the construction through leadership, knowledge transfer, alliance building, and advocacy participation. Sustainable development communities are the Ministry of Environment, think tanks, civil society, and institutions (e.g., United Nations Environmental Programme). These participants bring professional knowledge, build alliances, and raise public awareness. International organizations are related to financial system development: policy reform, knowledge development, and standard setting and coordination. Individuals are consumers of financial services, employees of financial institutions, and participants in civil society. They bring unique skills on how to relate the financial system to human needs and aspirations. Most of the above participants need to join alliances to play their respective roles at the national, regional, and international levels.

Table 3 lists the major stakeholders involved in Tianjin and Shenzhen, including primary direct, primary indirect, and secondary stakeholders.

5.2.1. Primary Direct Stakeholders

From a primary stakeholder’s perspective, the Tianjin project involves three major players, namely local governments, the administrative committee, and Urban Investment and Financing Platforms (UIFPs) and their subsidiaries. These players directly participate in the construction of SSTEC, greatly contributing to SSTEC’s development. Local governments in SSTEC are responsible for promoting the development of the local economy and preserving the environment. The administrative committee, as the representative of the local governments, has the same interests as local governments but predominantly focuses on implementation. Tianjin Eco-city Investment and Development Co., Ltd. (TEID) plays the role of master developer, being responsible for (1) land acquisition, consolidation, and reserve in the eco-city, and (2) investment, construction, operation, and maintenance of infrastructure and other public facilities in the eco-city.

The Shenzhen project does not have an administrative committee, in contradistinction to the Tianjin project. The primary stakeholders of the Shenzhen project include local governments and UIFPs. Local governments include both the municipal and district governments, namely Shenzhen Municipality, the low carbon office of Shenzhen Municipality, the low carbon office of Longgang District, and Pingdi Avenue. Each plays its role in the construction. The municipal government is responsible for overall planning of the low-carbon city, which includes making the overall development plan, developing innovative management mechanisms, and drafting standards for the construction and admittance of a newly entering industry. The district level governments stress the implementation function more. Their responsibilities cover overall planning, land acquisition, investment promotion, dealing with ILCC-based enterprises, and defending the interests of residents. The UIFPs in the Shenzhen project include both the municipal and district level UIFPs, i.e., CDG and Longgang District Urban Construction and Investment Co., Ltd. (DUCI). They are accountable for financing and investment, infrastructure development, investment promotion, operation, and management.

It should be noted that the two projects both have UIFPs, yet they serve different functions in each project. TEID distinguishes itself from other UIFPs in two respects. First, its ownership is diversified. Second, local authorities do not share profits from the company and are not responsible for its losses either. This means that TEID cannot be simply viewed as the local government’s financial vehicle. TEID is set up as per the needs of SSTEC yet operates on the basis of the principles of marketization and professionalization [40]. Similarly, TEID’s subsidiaries have diversified ownership as well, consisting of both Chinese and Singaporean firms. The objective of these subsidiaries is to generate profits through involvement in the construction with their expertise in fields such as waste management and water treatment. However, CDG and DUCI in the Shenzhen project are financial vehicles of local governments, which were founded earlier than the launch of ILCC and aimed at financing for local governments. CDG and DUCI are also responsible for the investment and development of other projects in Shenzhen, acting on behalf of the municipal and district government, respectively. A UIFP usually would found a project company when it fulfills its responsibilities for local governments. However, CDG did not set up a project company to meet the requirements of the construction of ILCC, which resulted in CDG playing a weaker role in ILCC compared with those UIFPs that set up project companies.

5.2.2. Primary Indirect Stakeholders

The policy support for the construction of SSTEC is characterized by ‘strong national government support, paired with structured foreign involvement’ [39]. Both the Singaporean and Chinese central governments are involved in the eco-city, having a great deal of influence on SSTEC at the national level; however, this impact is indirect. For example, the Chinese and the Singaporean central government together set the eco-city’s goal to build a replicable eco-city in SSTEC. The extensive political collaboration contributes to the progress SSTEC has made. The Chinese central government stipulates the overall planning, but does not get involved in the implementation. The Singaporean government offers its experience in environmental protection, but also looks for more opportunities to transfer its capital, technology, and knowledge. The extensive participation of the Singaporean government in SSTEC is a solid guarantee of sustainable funding.

The Shenzhen project is a demonstration program and a collaboration between China and the E.U. on sustainable urbanization. It involves multiple transnational investors, but does not have countries acting like the Singaporean government in SSTEC. Different from SSTEC, ILCC set up a steering committee, which is the representative of the National Development and Reform Committee, consisting of relevant ministries and commissions and Shenzhen Municipality. The steering committee oversees the progress of the low-carbon city; however, its impact is very limited.

5.2.3. Secondary Stakeholders

Banks, private parties, the public in China and other countries, and aboriginal residents are viewed as the secondary stakeholders due to their roles in the sustainable city. These stakeholders cannot influence the policies in the eco-city or the low-carbon city, but they play an instrumental role in funding the construction.

Regarding the Tianjin case, bank loans, bonds, and PPPs are the major financing vehicles employed in SSTEC. Accordingly, the stakeholders cover banks, the public in China and Singapore, and both China-based and Singapore-based private companies. Banks contribute to the construction through loans, and are one of the most traditional and reliable players in offering money for various construction projects. The public from China and Singapore provides their funds through buying bonds in the capital market. In the Tianjin case, in addition to the strong political support, the private parties from both countries are involved in the eco-city, including transnational and domestic investors [4,22]. From the Singaporean side, a Singaporean consortium led by Keppel Corporation is heavily involved in the development of the project, investing CNY 4 billion in the eco-city. Additionally, the Singaporean government also encouraged Singapore-based companies to expand their business in the low-carbon city by providing subsidies for them. From the Chinese side, many companies have become involved in the construction by investing their money through TEID’s subsidiaries.

Similarly, banks, the public, and private parties are also involved in the Shenzhen project. Banks merely play a role in providing loans for UCG to support the construction. In the Shenzhen model, local governments are the real debtors, especially when UCG cannot pay back its debts. The public provides funds for the project through buying bonds at the capital market. Additionally, multinational investors, such as ESI (a German company), and Japanese and American companies bring their capital to the project as well as their skills, technology, and other resources.

However, there are some differences in the involved stakeholders in the two projects, especially among the private parties. First, Tianjin issued bonds in the Singaporean capital market, which distinguishes its financing method from other projects, since TEID is the first Tianjin-based non-financial company to issue bonds in the international market. Second, SSTEC mainly cooperates with Singaporean investors, but ILCC cooperates with multiple transnational investors. Singaporeans are extensively involved in the construction of SSTEC, but there are no multinational investors playing roles as significant as Singaporean corporations in ILCC. The practice in ILCC makes the financing sources more diversified than SSTEC, reducing the risks the high dependency on a single country brings about. Third, original residents also play a different role in the construction process. Residents act as service payers in the Tianjin case, while residents in ILCC also act as investors by contributing their land use rights. The practice in Shenzhen changes the benefit distribution mechanism. Residents can share the fruits of ILCC’s development as well as act as major investors. This practice takes the disadvantaged group into account and thus reduces the conflicts between residents and local governments.

5.3. A Generic Model for Funding the Construction of Sustainable Cities

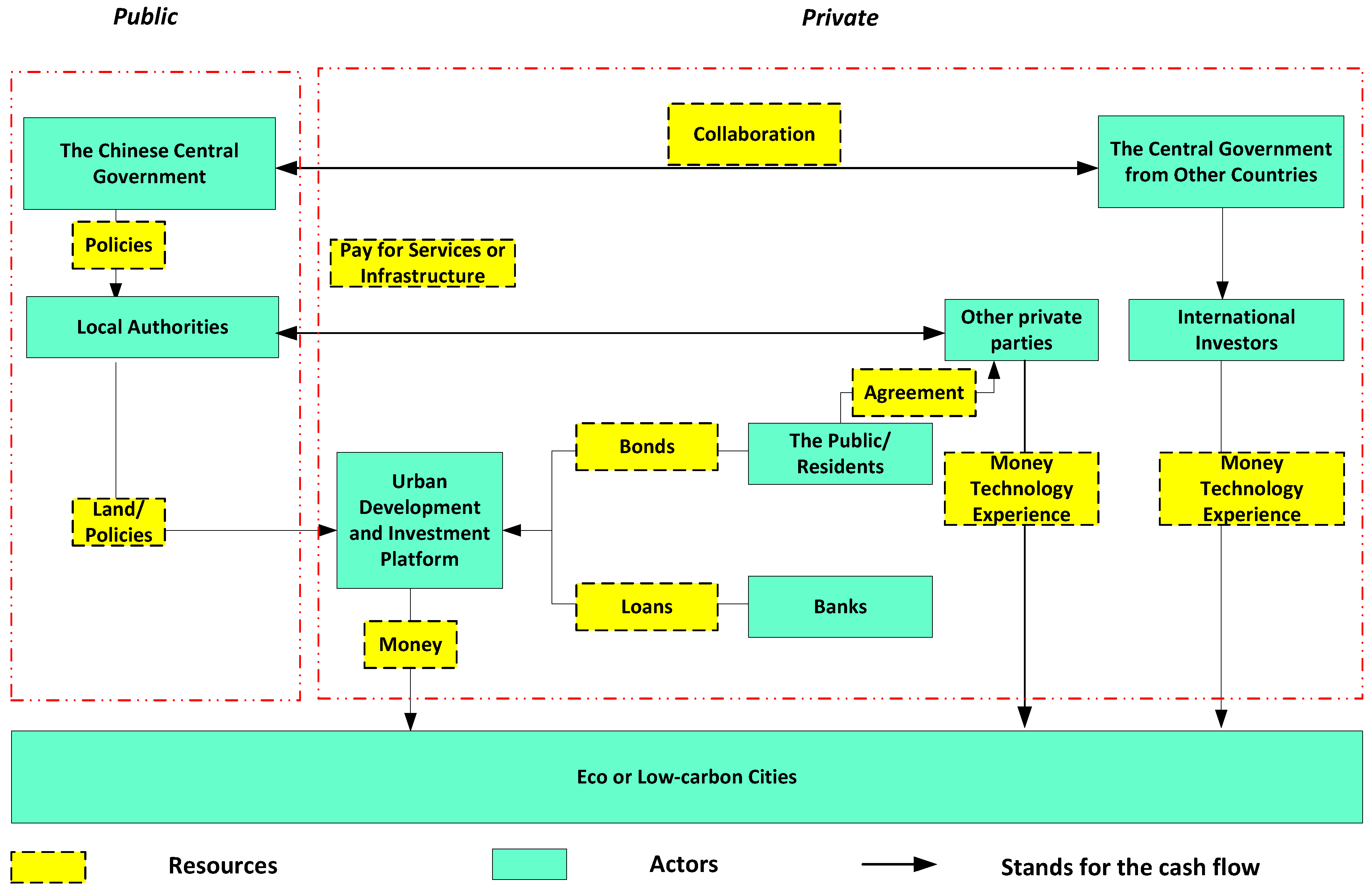

The similarities in finance between the Shenzhen and Tianjin cases indicate the critical role of traditional financial tools in urban development, while the differences present the innovative practice in each case and show the importance of exploring new instruments to diversify financial sources and balancing different stakeholders’ interests for sustainable finance. With the help of the analysis of the financial vehicles used in the two cases and the stakeholder analysis, we come to the following model for funding sustainable cities in China. Figure 1 is a generic model for funding sustainable cities, which brings various financial vehicles and stakeholders together to increase financial resilience. The model illustrates how stakeholders interact with each other and how they contribute to the development of sustainable cities. The key factors of the model are demonstrated below.

The Chinese central government and local governments are the initiators of the development of sustainable cities. Currently, various sustainable cities in China are developed under the supervision of ministries and commissions. Without national support, it is difficult to carry out projects successfully. For example, the failure of the Dongtan project was mainly due to the developer’s failure in obtaining a land conversion permit from the central government [4,41]. Therefore, the policy imperatives and various resource inputs from public authorities are key to the development of sustainable cities in the Chinese context.

Transnational governmental collaboration is crucial for projects to gain renown in the international market, which is conducive to attracting transnational investors to the project. China is still a developing country and lags behind in many respects, such as water treatment and the transformation of high-carbon-emission industries to low-carbon-emission ones. The participation of international counterparts brings not only money but also technology and skills.

UIFPs are either state-owned or state-holding enterprises, playing an instrumental role in arranging various resources. They are representatives of local governments to raise money from banks and the capital market. Some UIFPs are listed on stock exchanges, making them responsible to the public rather than merely representing local governments. However, the role of UIFPs is changing, as the National Audit Office of PRC has reported that local governments are at high risk of dealing with implicit debts through UIFPs [42]. Currently, local governments try to operate UIFPs based on the principle of marketization, and propose to implement PPPs to reduce their financial burden [22].

Concession agreements with public authorities give permission to private parties to charge fees from the public. For example, the application of the ‘metro plus property’ model allows the involved players to be paid through selling the properties along the metro line and collecting fees from metro travelers.

The public is another important financial source for a construction project, while residents are the cash inflow for the development of sustainable cities to guarantee the revenues under the arrangements used with PPP.

This model embodies both traditional and new financial instruments. Traditional financial instruments, such as bank loans and bonds issued in the Chinese capital market, guarantee the stability of the sources. Innovative financing practices expand financing sources and are conducive to raising a higher amount of money [26]. Furthermore, different stakeholders are taken into account to ensure the rest of the sustainable attributes as defined by Sun et al. [21]: efficiency, ease of implementation, and political acceptance. The model also covers governments from other countries, multinational investors, and local investors. They are encouraged to participate in the construction of sustainable cities. The international collaboration between governments eradicates many barriers in the implementation and is beneficial for attracting more private investors [30], which increases political acceptability. The involvement of private parties brings in money. They also bring in new technologies and expertise. The participation of governments and private parties makes it possible to achieve the environmental goals. The Chinese government plays an instrumental role in raising funds for environmental purposes, especially the development of green bonds. It encourages issuing cross-border green bonds, which increases international investors’ interests in investing in green projects [43]. From the investors’ side, green bonds are attractive since they have the characteristics of high stability, excellent credit, and good liquidity [43]. The consideration of different stakeholder’s interests guarantees social sustainability by offering each of them opportunities to share in economic development. Issuing green bonds guides the money towards green projects and facilitates cities to transition to a low-carbon economy and environmental sustainability. The involvement of private parties provides funds and expertise for the development of sustainable cities boosting the economy’s development, which contributes to economic sustainability as well.

6. Conclusions

We compared SSTEC and ILCC to gain insight into the similarities and differences in funding sustainable cities and thus to provide references for future sustainable construction projects. The two cases both rely on bank loans, corporate bonds, and PPP to provide funds for their construction, which are traditional vehicles for funding sustainable cities. There is no doubt that other projects can resort to these tools, but these do not suffice to raise money for the development of sustainable cities.

Therefore, light was cast on the innovative practices in SSTEC and ILCC, diversifying the funding sources. The Tianjin project offers experience in issuing bonds in the international market, which is the first bond issued by a Tianjin-based non-financial institute. One the one hand, issuing bonds in the international capital market expands financing sources and facilitates the project developer to raise money with lower costs. On the other hand, it is an efficient way to raise large sums of money and enhances the project’s influence domestically and globally [20]. Such practice would be especially important to climate finance due to its lower interests and wider influences, and thus should be encouraged by the Chinese authorities. However, we should not forget that the master developer in SSTEC successfully issued bonds in Singapore partly because of assistance from the Chinese central government. Therefore, it is critical to change institutional arrangements to eradicate the barriers for non-financial corporations for issuing bonds internationally. Regarding the Shenzhen project, planning the village area as a whole and arranging finance through ‘metro plus property’ provide a replicable example for other cities in funding urban renewal and community transformation and dealing with the issue of how residents can share the benefits of urban development with developers. The practice taking the interests of third parties into account guarantees social sustainability because it meets the needs of the disadvantaged group by increasing their access to economic opportunities [44]. These innovative financing practices from the Tianjin and Shenzhen projects can be applied to other similar projects in China and globally. Taken as a whole though, Shenzhen and ILCC have developed a model of sustainable finance with less extensive financial and other support from the central government and foreign governments than SSTEC, and thus may offer more practical lessons for other cities. This should certainly be seen as a significant institutional and organizational step forward in achieving the social, environmental, and economic goals in sustainable urbanization.

The generic model that was constructed on the basis of Shenzhen’s and Tianjin’s experiences provides valuable lessons for other sustainable construction projects in how to finance their development in structural ways by incorporating social, economic, and environmental factors into their financing practices. The contribution of this research is not to be exhaustive, but to introduce innovative practices to other projects both launched in China and globally. However, it should be noted that the model cannot be applied to other projects directly, since local conditions always vary, particularly projects launched in other countries, requiring policy-makers and practitioners to make adjustments when they take the model as a reference. For instance, the decision-making processes are different between China and many other countries, which influences the efficiency of project development and thus how costs are handled. The difference, coupled with different land property right institutions, determines that planning the village as a whole might not be feasible in those countries to implement a bottom-up approach, since a longer time-frame and more efforts are required in negotiating with other actors than in China. However, the concept of mobilizing private capital through international collaboration and the involvement of governments should be encouraged to implement PPPs by both Chinese and international sustainable initiators. Furthermore, this model is still conceptual. Many other detailed issues should be further explored, such as the choice of discount rates [45,46] and information disclosure [47]. Currently, the environmental externalities, particularly negative externalities, have not been taken into account when gauging the feasibility of a project, which makes the project financially feasible even if it might be environmentally infeasible. As such, researchers, such as Scholtens [46], propose that the environmental influence should be taken into account when calculating the return of investment (ROI). Internalizing negative externalities will increase an operator’s costs and thus decrease the project’s ROI, which might prevent enterprises from initiating projects with negative environmental externalities. Contrarily, the internalization of positive externalities will lead to an increase in the ROI by adding value to enterprises, which is conducive to having money flowing into the field of sustainable urban development. Additionally, the disclosure of information regarding accountability, governance, and implementation is notoriously poor [47], which is a barrier to evaluating ecological implications and risks for investors [46]. Therefore, more effort should be put into funding future projects sustainably, which requires cooperation among the involved actors and a balancing of their respective interests.

Author Contributions

C.Z. and M.J. designed the study. C.Z. collected and analyzed the data and wrote the core of the manuscript. M.J. contributed to the manuscript by eliciting its narrative and adding, revising and editing text. H.B. contributed to the conceptualization and supervision of the article.

Funding

The authors are indebted to the Urban Knowledge Network Asia (UKNA) and the Delft Initiative for Mobility and Infrastructures for their financial support.

Acknowledgments

The authors thank the anonymous reviewers for their constructive comments on an earlier version of this manuscript.

Conflicts of Interest

The authors declare no conflict of interest.

References and Notes

- Liu, Z.; Salzberg, A. Developing Low-Carbon Cities in China: Local Governance, Municipal Finance, and Land-Use Planning-The Key Underlying Drivers. In Sustainable Low-Carbon City Development in China; Baeumler, A., Ijjasz-Vasquez, E., Mehndiratta, S., Eds.; World Bank: Washington, DC, USA, 2012; pp. 97–127. [Google Scholar]

- Zhang, Y. China National Human Development Report 2013: Sustainable and Liveable Cities: Toward Ecological Civilization. 2013. Available online: http://www.cn.undp.org/content/dam/china/docs/Publications/UNDP-CH_2013%20NHDR_EN.pdf (accessed on 16 April 2017).

- de Jong, M.; Joss, S.; Schraven, D.; Zhan, C.; Weijnen, M. Sustainable-Smart-Resilient-Low Carbon-Eco-Knowledge Cities: Making sense of a multitude of concepts promoting sustainable urbanization. J. Clean. Prod. 2015, 109, 25–38. [Google Scholar] [CrossRef]

- Miao, B.; Lang, G. A Tale of Eco-cities: Experimentation under Hierarchy in Shanghai and Tianjin. Urban Policy Res. 2015, 2, 247–263. [Google Scholar] [CrossRef]

- The UK-China Eco-Cities & Green Building Group. Progressing Eco-City Policies into Mainstream Practice in China. 2012. Available online: http://www.igsystems.co.uk/uploads/2/1/3/4/21346554/progressing_eco_city_policies_into_main_stream_practice_-_digital_edition_v1.1.pdf (accessed on 12 July 2017).

- UNCTAD. World Investment Report 2014—Investing in SDGs. 2014. Available online: http://unctad.org/en/pages/PublicationWebflyer.aspx?publicationid=937 (accessed on 1 July 2017).

- Baeumler, A.; Mehndiratta, S. Financing a Low-Carbon City: Introduction. In Sustainable Low-Carbon City Development in China; Baeumler, A., Ijjasz-Vasquez, E., Mehndiratta, S., Eds.; World Bank: Washington, DC, USA, 2012; p. 467. [Google Scholar]

- Research Institute for Fiscal Science Ministry of Finance, P. R. China. Climate Public Expenditure and Institutional Review in China. 2015. Available online: http://www.cn.undp.org/content/china/en/home/presscenter/pressreleases/2015/04/new-report-sheds-light-on-chinas-climate-public-expenditure/ (accessed on 10 August 2017).

- Bovenberg, A.L.; De Mooij, R.A. Environmental Tax Reform and Endogenous Growth. J. Public Econ. 1997, 63, 207–237. [Google Scholar] [CrossRef]

- Engel, S.; Pagiola, S.; Wunder, S. Designing Payments for Environmental Services in Theory and Practice: An Overview of the Issues. Ecol. Econ. 2008, 65, 663–674. [Google Scholar] [CrossRef]

- Sandmo, A. Optimal Taxation in the Presence of Externalities. Swed. J. Econ. 1975, 77, 86–98. [Google Scholar] [CrossRef]

- Merk, O.; Saussier, S.; Staropoli, C.; Slack, E.; Kim, J.-H. Financing Green Urban Infrastructure. OECD Regional Development Working Papers 2012/10. 2010. Available online: http://dc.doi.org/10.1787/5k92p0c6j6r0-en (accessed on 3 April 2017).

- Inman, R.P. Financing Cities. 2005. Available online: http://www.nber.org/papers/w11203.pdf (accessed on 6 May 2017).

- Slack, E. Financing Large Cities and Metropolitan Areas. 2010. Available online: http://www.ieb.ub.edu/aplicacio/fitxers/2012/2/InformeFF2011_eng.pdf#page=39 (accessed on 10 July 2017).

- Bahl, R.W.; Linn, J.F. Governing and Financing Cities in the Developing World. 2014. Available online: http://www.lincolninst.edu/sites/default/files/pubfiles/governing-and-financing-cities-developing-world-full_0.pdf (accessed on 10 July 2017).

- Z/YenGroup. Financing the Transition: Sustainable Infrastructure in Cities. 2015. Available online: http://www.wwf.se/source.php/1667872/summary_financing_infrastructure_in_cities_1.pdf (accessed on 22 March 2017).

- Panayotou, T. Instruments of Change: Motivating and Financing Sustainable Development; Routledge: Abingdon-on-Thames, UK, 2013. [Google Scholar]

- Bäckstrand, K. Multi-stakeholder Partnerships for Sustainable Development: Rethinking Legitimacy, Accountability and Effectiveness. Eur. Environ. 2006, 16, 290–306. [Google Scholar] [CrossRef]

- Olsen, K.H. The Clean Development Mechanism’s Contribution to Sustainable Development: A Review of the Literature. Clim. Chang. 2007, 84, 59–73. [Google Scholar] [CrossRef]

- Meltzer, J.P. Financing Low Carbon, Climate Resilient Infrastructure: The Role of Climate Finance and Green Financial System. 2016. Available online: https://www.brookings.edu/wp-content/uploads/2016/09/global_20160921_climate_finance.pdf (accessed on 18 June 2017).

- Sun, Z.; Li, X.; Xie, Y. A Comparison of Innovative Financing and General Fiscal Investment Strategies for Second-class Highways: Perspectives for Building a Sustainable Financing Strategy. Transp. Policy 2014, 35, 193–201. [Google Scholar] [CrossRef]

- Zhan, C.; de Jong, M.; de Bruijn, H. Path Dependence in Financing Urban Infrastructure Development in China: 1949–2016. J. Urban Technol. 2017, 24, 73–93. [Google Scholar] [CrossRef]

- Sullivan, R.; Gouldson, A.; Webber, P. Funding Low Carbon Cities: Local Perspectives on Opportunities and Risks. Clim. Policy 2013, 13, 514–529. [Google Scholar] [CrossRef]

- Jacobson, C.; Choi, S.O. Success Factors: Public Works and Public–private Partnerships. Int. J. Public Sector Manag. 2008, 21, 637–657. [Google Scholar] [CrossRef]

- Osei-Kyei, R.; Chan, A.P. Review of Studies on the Critical Success Factors for Public–Private Partnership (PPP) Projects from 1990 to 2013. Int. J. Proj. Manag. 2015, 33, 1335–1346. [Google Scholar] [CrossRef]

- Reichelt, H. Green Bonds: A Model to Mobilize Private Capital to Fund Climate Change Mitigation and Adaptation Projects. In The EuroMoney Environmental Finance Handbook; The World Bank: Washington, DC, USA, 2010; pp. 1–7. [Google Scholar]

- Climate Bond Initiative, China Central Depository & Clearing Co., Ltd. (CCDC). Report on the Current Status of China Green Bond Market 2016. 2017. Available online: https://www.climatebonds.net/files/reports/sotm-2016-a4-cn_1.pdf (accessed on 11 August 2017).

- Shishlov, I.; Morel, R.; Cochran, I. Beyond Transparency: Unlocking the Full Potential of Green Bonds. 2016. Available online: https://www.i4ce.org/wp-core/wp-content/uploads/2016/06/I4CE_Green_Bonds.pdf (accessed on 15 May 2017).

- Zhan, C.; de Jong, M. Financing Sino-Singapore Tianjin Eco-City: What Lessons Can Be Drawn for Other Large-scale Sustainable City-projects? Sustainaility 2017, 9, 201. [Google Scholar] [CrossRef]

- Zhan, C.; de Jong, M. Financing Low Carbon City: The Case of Shenzhen International Low Carbon City. J. Clean. Prod. 2018, 180, 116–125. [Google Scholar] [CrossRef]

- ILCC. Project Information. Available online: http://ilcc2015.szvi.com/Overview/Default.aspx (accessed on 23 March 2017).

- Interviewee 1 (HIT Shenzhen China). Interview. 2016.

- SSTEID. About Sino-Singapore Tianjin Eco-City Investment & Development Co., Ltd. Available online: http://stc.dashilan.cn/en/SinglePage.aspx?column_id=10304 (accessed on 23 March 2017).

- Ba, S.; Yang, X. The New Urbanization Financing and Financial Reform; Workers Press: Beijing, China, 2014. [Google Scholar]

- Financial staff 1 (TEID Tianjin China). Interview. 2015.

- Financial staff 2 (TEID Tianjin China). Interview. 2016.

- de Jong, M.; Wang, D.; Yu, C. Exploring the Relevance of the Eco-city Concept in China: The Case of Shenzhen Sino-Dutch Low Carbon City. J. Urban Technol. 2013, 20, 95–113. [Google Scholar] [CrossRef]

- Cheshmehzangi, A.; Xie, L.J.; Tan-Mullins, M. The Role of International Actors in Low-carbon Transitions of Shenzhen’s International Low Carbon City in China. Cities 2018, 74, 64–74. [Google Scholar] [CrossRef]

- de Jong, M.; Yu, C.; Joss, S.; Wennersten, R.; Yu, L.; Zhang, X.L.; Ma, X. Eco City Development in China: Addressing the Policy Implementation Challenge. J. Clean. Prod. 2016, 134, 31–41. [Google Scholar] [CrossRef]

- Civil servant (Administrative Committee of SSTEC Tianjin China). Interview. 2015.

- Ma, X.; de Jong, M.; den Hartog, H. Assessing the Implementation of the Chongming Eco Island Policy: What a Broad Planning Framework Can Tell More than Technocratic Indicator Systems. J. Clean. Prod. 2018, 172, 872–886. [Google Scholar] [CrossRef]

- National Audit Office of P. R. China. The Audit Result of National Government Debts. 2013. Available online: http://www.audit.gov.cn/n1992130/n1992150/n1992500/3432077.html (accessed on 5 July 2016).

- Climate Bond Initiative. 2015 Green Bond Market Roundup. 2015. Available online: https://www.climatebonds.net/files/files/2015%20GB%20Market%20Roundup%2003A.pdf (accessed on 16 August 2017).

- Godfrey, N.; Zhao, X. Financing the Urban Transition for Sustainable Development: Better Finance for Better Cities, Contributing paper for the Sustainable Infrastructure Imperative: Financing for Better Growth and Development. New Climate Economy, London and Washington, DC. 2016. Available online: http://newclimateeconomy.report/misc/working-papers/ (accessed on 8 September 2017).

- Gollier, C. Pricing the Planet’s Future; Princeton University Press: Princeton, NJ, USA, 2013. [Google Scholar]

- Scholtens, B. Why Finance Should Care about Ecology. Trends Ecol. Evol. 2017, 32, 500–505. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Eisenbach, S.; Schiereck, D.; Trillig, J.; von Flotow, P. Sustainable project finance, the adoption of the Equator principles and shareholder value effects. Bus. Strateg. Environ. 2014, 23, 375–394. [Google Scholar] [CrossRef]

Figure 1.

A generic model for funding sustainable cities.

{kind=link}

Table 1.

A comparison between Tianjin’s profile and Shenzhen’s profile.

| Tianjin | Shenzhen | |

|---|---|---|

| Year of launch | 2007 | 2012 |

| Total area | 30 km2 | 53.4 km2 |

| Location | SSTEC is located in the core area of Tianjin Binhai New Area, which is 45 km from Tianjin’s city center, 150 km from Beijing, 40 km from Binhai International Airport, and 20 km from Tianjin Port. | ILCC is located in Longgang District, Shenzhen, China, at the border of Dongguan and Huizhou in Guangdong province. |

| Geographic conditions | An area consisting of deserted salt pans, saline-alkaline non-arable land, and polluted water bodies. | Nearly half of the Pingdi Avenue is mountain area, of which 40% is natural reserve land; the other half has been urbanized. |

| Goals | To establish a replicable eco-city that is resource-saving, environmentally friendly, economically robust, and socially harmonious. Sino-Singapore Tianjin Eco-city has a planning area of approximately 30 km2 and will be established in 10–15 years with an estimated population of 350,000. | To build a low-carbon technology research and development center and a low-carbon technology integration application demonstration center, a low-emission industry gathering center, a low-carbon solution provider center, and a low-carbon development service center |

| Industries | Cultural creation, environmental protection, high technology, specific finance, information technology and related services, and green building. | Service industry, information technology (IT) industry, energy and environmental protection industry, modern agricultural industry, low-carbon economic new material industry. |

Source: abstracted from Sino-Singapore Tianjin Eco-city (SSTEC)’s and Shenzhen International Low-Carbon City (ILCC)’s brochures.

Table 2.

The financial vehicles that Tianjin and Shenzhen employ.

| Financing Vehicles | Tianjin | Shenzhen |

|---|---|---|

| Bank loans | x | x |

| Corporate bonds | x | x |

| Public–Private Partnerships | ||

| - Planning the village area as a whole (PVAW) | x | |

| - Metro plus Property model | x | |

| - Foreign capital | x | x |

| - Funds from domestic private investors | x | x |

| National and international Assistance | ||

| Governmental funds and tax refunds | x | |

| International assistant programs | x |

Table 3.

The stakeholders involved in Tianjin and Shenzhen.

| Stakeholders | Tianjin | Shenzhen |

|---|---|---|

| (A) Primary direct | ||

| Local Governments | x | x |

| Administrative Committee | x | |

| Urban Investment and Financing Platforms and subsidiaries | x | x |

| (B) Primary indirect | ||

| Chinese Central Government | x | x |

| The Central Government of Other Countries | x | |

| Steering Committee | x | |

| (C) Secondary | ||

| Banks | x | x |

| Private Parties (including parties from other countries) involved in the construction | x | x |

| The Public in China | x | x |

| The Public in Other Countries | x | |

| Other Companies Based in the Eco-city or Low-carbon City | x | x |

| Residents | x | x |

Note: (A) Direct primary stakeholders: parties that directly participate in the construction of SSTEC and ILCC. (B) Indirect primary stakeholders: parties that indirectly participate in the construction of SSTEC and ILCC but are important and have a high influence on the construction. (C) Secondary stakeholders: remaining players, including parties that are important but with low influence, or less important and with low influence. Sources: Zhan and de Jong [29] and Zhan and de Jong [30].

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Zhan, C.; De Jong, M.; De Bruijn, H. Funding Sustainable Cities: A Comparative Study of Sino-Singapore Tianjin Eco-City and Shenzhen International Low-Carbon City. Sustainability 2018, 10, 4256. https://doi.org/10.3390/su10114256

AMA Style

Zhan C, De Jong M, De Bruijn H. Funding Sustainable Cities: A Comparative Study of Sino-Singapore Tianjin Eco-City and Shenzhen International Low-Carbon City. Sustainability. 2018; 10(11):4256. https://doi.org/10.3390/su10114256

Chicago/Turabian StyleZhan, Changjie, Martin De Jong, and Hans De Bruijn. 2018. "Funding Sustainable Cities: A Comparative Study of Sino-Singapore Tianjin Eco-City and Shenzhen International Low-Carbon City" Sustainability 10, no. 11: 4256. https://doi.org/10.3390/su10114256

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.