Analyzing Characteristics and Implications of the Mortgage Default of Agricultural Land Management Rights in Recent China Based on 724 Court Decisions

1

School of Business Administration, Northeastern University, Shenyang 110819, China

2

School of Economic Crime Investigation, Criminal Investigation Police University of China, Shenyang 110854, China

3

School of Marxism, Party School of the Central Committee of C.P.C. (National Academy of Governance), Beijing 100089, China

*

Author to whom correspondence should be addressed.

Land 2021, 10(7), 729; https://doi.org/10.3390/land10070729

Submission received: 9 June 2021

/

Revised: 8 July 2021

/

Accepted: 9 July 2021

/

Published: 12 July 2021

(This article belongs to the Special Issue Land Use Transitions under Rapid Urbanization)

Abstract

:The transfer of rural land contractual management rights belongs to the recessive transition of land use. The mortgage of rural land management rights is a way of rural land circulation, and has an important impact on the transformation of land use. Rural land management rights mortgage loans can enable farmers to obtain more credit funds, which is conducive to agricultural development and Rural Revitalization. However, with the development of rural land mortgage financing, the associated risk has become increasingly prominent. The most typical risk is the default risk of farmers’ mortgage loans. Based on court decisions regarding rural land mortgage default during 2014–2020, this paper analyzes the characteristics of farmers’ default in different periods and locations. The empirical results reveal that the time and space of rural land mortgage default cases are widely distributed in China, especially in Heilongjiang Province. In the default judgement, the loan amount of CNY 50,000 to CNY 100,000 and the loan periods of 1 year accounted for the highest proportion. When making mortgage loan policies for rural land management rights, financial institutions should give farmers the most preferential treatment regarding the amount, term and interest rate of loans. Farmers’ social security should be improved, and agricultural insurance should be strengthened. Meanwhile, the credit review of small and short-term loan farmers should be heightened.

1. Introduction

China is a large agricultural country where agricultural land is the foundation of the rural social and economic system [1,2]. The system of agricultural land is not only closely related to agriculture, rural areas and farmers, but also directly affects the overall development level of the national economy. China’s agricultural land system has its own particularities. Land belongs to the state or collective, and private ownership is not allowed. In the past, the law prohibited the mortgage of agricultural land. In recent years, the separation of the ownership, contracting rights and management rights of agricultural land was proposed, and mortgage financing of land management rights was allowed in China [3,4,5,6]. The rural land mortgage system has Chinese characteristics. The Central Committee of the Communist Party of China (CPC) has long promoted comprehensive rural reform and supply-side structural reform, and the reform of the agricultural land system has been the core content [7,8,9]. After a long period of practice, the system of agricultural land mortgaging in developed countries is relatively mature [10,11]. With the introduction of the concept of land use transition into China [12,13,14,15], woodland and cultivated land have been the hot spots of land use transition research [16,17]. The transfer of rural land contractual management rights belongs to the recessive transformation of land use. The mortgage of rural land management rights is a way of rural land circulation, which will have an important impact on the transformation of land use. Rural land management rights mortgage loans can enable farmers to obtain more credit funds, which is conducive to agricultural development and rural revitalization.

The mortgage financing of farmland management rights is an important means for the government to support agriculture through the financial market and plays a positive and effective role in the development of rural finance [18,19,20]. However, as a new financial product, there are still many obstacles and restrictive factors in the financing of farmland mortgages in China. Among them, the risk problem is the greatest obstacle, which restricts the development of farmland mortgage financing and affects the implementation of mortgage financing through farmland management rights. Therefore, based on promoting land circulation, preventing and controlling the default risk of the mortgage of farmland management rights, and minimizing the cost of financial institutions supporting agriculture, rural areas and farmers have become a topic of wide concern to the state and all sectors of society.

In this regard, many studies have addressed risk types, empirical cases and the risk control of farmland management right mortgages. Agricultural land mortgage financing entails many types of risks, such as credit, nature, market (operation) and policy (system) [21,22,23,24,25]. The risks of agricultural land mortgage financing are reflected in the risk of farmers’ livelihood and the repayment source risk of banks at the micro level and in the rural social risk and rural financial risk at the macro level [26]. The regression analysis method and AHP method were used to demonstrate the factors that affect credit risk and predict the probability of default [27,28,29]. Studies have shown that the bank credit system, relevant systems, mortgage and disposal conditions, and risk compensation and sharing mechanisms were the key points of risk management [26,30].

In addition, the unclear property rights of farmland as collateral and high market transaction costs were the main causes of the risks perceived by financial institutions, such that the institutions did not actively lend to farmers who applied for loans with such collateral [31,32]. A prerequisite for effective agricultural land mortgage development is the development of effective instruments for the risk management of creditors in the pledging of agricultural land [33]. Yin [34] conducted empirical research on the risk measurement of mortgage loans on rural land contracts and management rights in Heilongjiang Province.

Previous studies on rural land mortgages have mainly focused on the willingness of actors on the supply and demand sides, financial innovation mechanisms and performance, and loan risk evaluation systems, and these studies mainly used the questionnaire method or model prediction within a certain area. The content of such surveys reflects the ideas of the respondents, not the objective situation, and conclusions based on such information lack scientific support. The above studies are important, but there is no precedent for statistics of rural land mortgage default cases nationwide.

In recent years, with the help of big data, legal judgment documents are increasingly applied to many fields [35,36]. This article uses the empirical research method to study the cases of rural land mortgage default judged by the first instance of the national court during 2014–2020. The 724 default cases in this article are all confirmed cases by the court and the data are true and reliable. According to the phenomenon of rural mortgage default, the formation mechanism of rural land mortgage loans is analyzed. Along with the court cases, the competent department of agricultural land mortgage finance of Heilongjiang Province is investigated. The research method of this article is highly objective and rigorous. It is of great significance to understand the characteristics of rural land mortgage default from all over the country and to reduce the risk of default.

2. Empirical Approach and Data

2.1. Sources of Data

Based on the key words of “rural land mortgage”, 868 civil judgements of the first instance of the national court were retrieved from the “China judgement documents website”, of which 724 were effective without repeated judgements. The “China judgment documents website” is a national platform for publishing court judgement documents established by the Supreme People’s Court of the People’s Republic of China. According to the requirements of the Supreme People’s court, the Supreme People’s court, all higher people’s courts and intermediate people’s courts across the country must publish judgement documents on the “China judgement documents website” from 1 January 2014. In addition, the basic people’s courts of 10 eastern provinces, including Beijing, Tianjin and Liaoning, and three central and western provinces, Henan, Guangxi and Shaanxi, should publish their judgement documents online. Since the end of June 2015, the courts at all three levels in 31 provinces (autonomous regions and municipalities) and Xinjiang Production and Construction Corps have all published effective judgement documents online. Therefore, the data source of this paper is authoritative, and the cases retrieved in this paper are comprehensive. In this paper, the court judgement time of farmland mortgage default cases is continuous from 2014 to 2020.

2.2. Empirical Approach

We adopted the empirical analysis method. Our empirical analysis focused on three issues. First, we combed each case and set specific indicators such as judgment court, judgment time, natural situation of borrower, name of lender, loan amount, loan term, loan interest rate, etc. Second, we summarized the indicators and find the common characteristics. Finally, we analyzed the causes of default and propose solutions.

3. Results

The comprehensive quality of borrowers plays a decisive role in the operation and management ability of farmers’ families, and can directly affect the use behavior of farmers’ credit funds. Among them, age is an important factor to reflect the repayment ability of the lender. Therefore, this paper analyzed the age characteristics of the defaulter. Similarly, the characteristics of the rural land mortgage also play an important role in the analysis of farmers’ default characteristics, so this article also analyzes the loan characteristics of default farmers.

3.1. Trend of the Default Cases

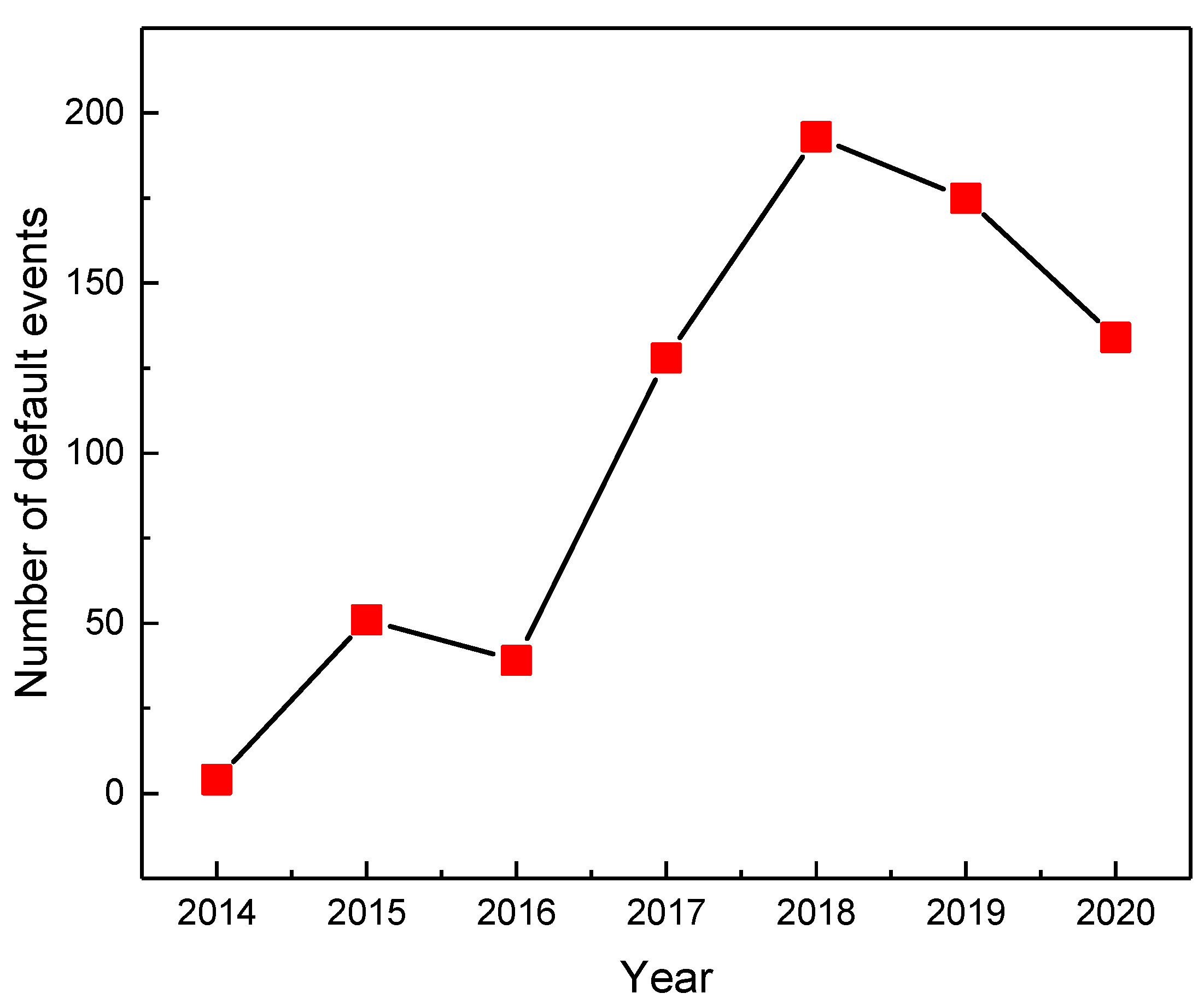

Figure 1 shows the proportion of default cases of farmland mortgages in each year from 2014 to 2020 in China. China’s law once prohibited the mortgage of farmland management rights, and there were few judgements on mortgage default cases before 2016. On 27 December 2015, authorized by the committee of the National People’s Congress (NPC), the State Council implemented “The Property Law” and “The Guarantee Law”, outlining the provisions that the right to use collectively owned cultivated land shall not be mortgaged in the administrative areas of 232 pilot counties (cities and districts). Since 2016, the “two-right” mortgage loan pilot project has been authorized by law, which has significantly stimulated the rural financial market. In 2018, the rural land contract law was amended to allow the mortgage of rural land management rights nationwide. With the guidance and publicity of local governments and financial departments, the number of rural land management right mortgage loans has gradually increased since 2016. In the early stage of loans, some borrowers had the impulse to borrow. The impulse of borrowing is the borrower’s cognitive deviation. The borrower does not consider his own actual situation, has the herd mentality when borrowing and has no proper use after borrowing, which leads to the failure to repay the loan on time; thus, there was a large number of default cases that peaked in 2018. The court decision shows that the financial institutions in the pilot areas sued the court, and the farmers who had borrowed money protested on the grounds that the mortgage violated legal provisions. As the loan review of financial institutions became stricter and borrowers began to make wiser decisions, loan default cases started a downward trend in 2019. Moreover, financial institutions have explored other ways to address risk, such as requiring the government to provide guarantees, setting up risk funds, and adopting multiple guarantees [37]. These measures have effectively addressed the default risk of borrowers to a certain extent.

3.2. Spacial Characteristics of the Default Cases

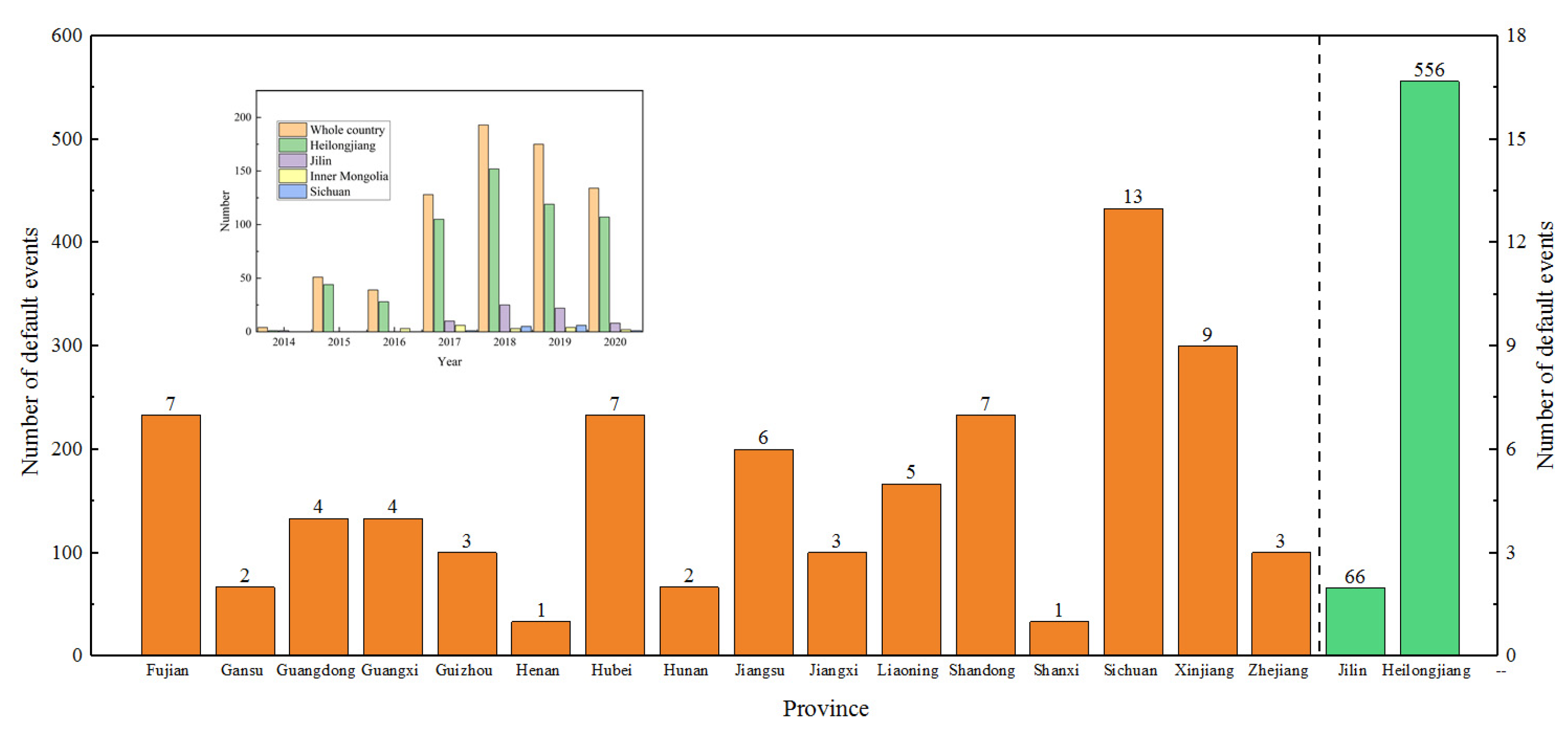

Figure 2 shows the regions where farmers defaulted on agricultural land mortgage loans in China from 2014 to 2019, with 19 provinces and autonomous regions affected; thus, the coverage area was relatively wide. From Figure 2, the provinces with a high number of default cases are Heilongjiang, Jilin and Inner Mongolia. There were 556 defaulting households in Heilongjiang Province, accounting for 77% of the total defaulting households. Heilongjiang Province presents the largest number of farmers defaulting on farmland mortgage loans. Heilongjiang Province is a large agricultural province in China, with 239 million mu of arable land, accounting for one ninth of the arable land in the country. The per capita arable land of the agricultural population is more than 10 mu, ranking first in the country [38]. Thus, Heilongjiang has the material basis for farmland mortgage loans. The scale of agricultural land mortgage loans in Heilongjiang Province is far greater than that in other provinces, as is the number of default cases. On the other hand, as early as 2010, Heilongjiang Province formulated the “Heilongjiang Province rural land management right mortgage loan method (Trial)”, selecting four cities and six counties to carry out the pilot work. In 2015, Heilongjiang was identified as the pilot area of land management right mortgage by the State Council, with 15 pilot districts and counties, ranking first in the country. By the end of 2017, the balance of rural land loans in Heilongjiang Province accounted for more than 30% of the total scale of the national pilot areas [39].

3.3. Loan Amount of the Default Cases

Table 1 reveals the relationship between the number of defaulting farmers and the amount of default. As shown in Table 1, the defaulting households with a loan amount of 50,000 to 100,000 account for the largest proportion, up to 33.7%, followed by the defaulting households with a loan amount of less than 50,000, accounting for 21%, and the defaulting households with a loan amount of 500,000 to 1 million represent the smallest proportion, accounting for only 6.5% in total.

In all 724 default cases, 694 borrowers were natural persons, and 30 borrowers were companies or agricultural operation organizations. This is related to the area of mortgageable land owned by peasant households. The mortgage loan amount of rural land contracting and management rights is generally between 50 and 80% of the recognized value of the land assessed (including the attached objects on the ground), with different regulations in different regions.

Table 2 indicates that the default cases in which the borrowers are companies or cooperatives account for 4% of all default cases. Companies or cooperatives are the borrowers in 70% of the default cases with a loan amount of more than CNY 1 million.

3.4. Loan Term of the Default Cases

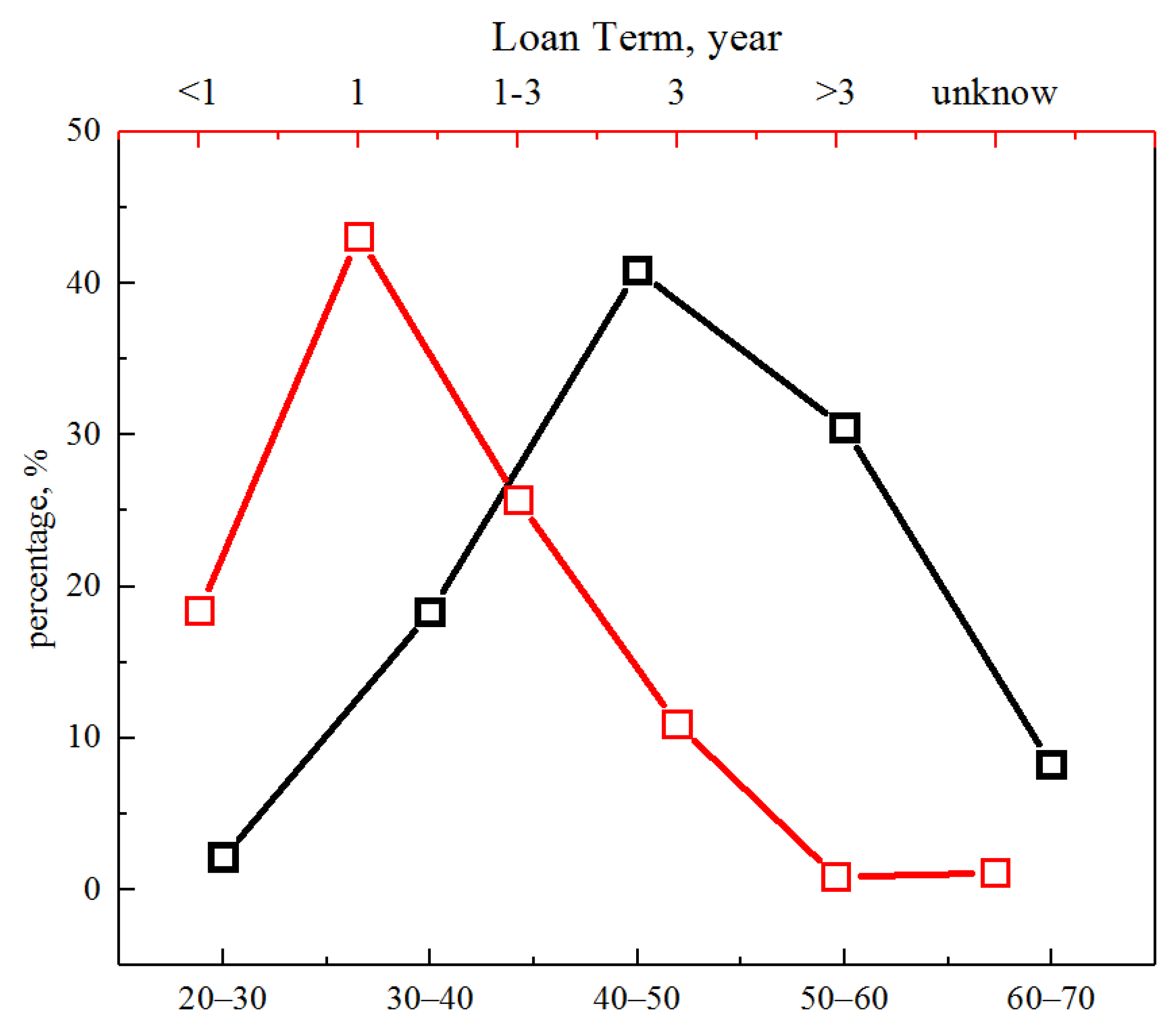

Figure 3 shows the distribution characteristics of the defaulting farmers’ age and the loan years in Heilongjiang Province from 2014 to 2020. As shown in Figure 3, the number of households with a loan term equal to 1 year is the largest, accounting for more than 40% of the total number of households with loans. Due to the high risk and volatility of agricultural operations, the loan term is relatively short. Generally, the mortgage loan term of rural land management rights is 1 year and, in principle, no more than 3 years. Terms of 5–10 years or more are also available in some areas, but they are few. From the characteristics of loan age, the largest number of farmers defaulting on farmland mortgage loans are between 40 and 50 years old, accounting for approximately 40% of each age group, followed by farmers between 50 and 60 years old, accounting for approximately 30% of the total. This is consistent with the results in previous studies [40]. The survey data [41] show that the age of agricultural labor force is middle-aged, with an average age of 48.5 years old. Men nearly 50 years old have become the main force in farming, and more than 60% of them are full-time agricultural producers. Most households with borrowing needs and borrowing behaviors are households whose heads are older than 40. Therefore, these households also account for the highest proportion of default events.

3.5. Loan Institutions and Interest Rates of the Default Cases

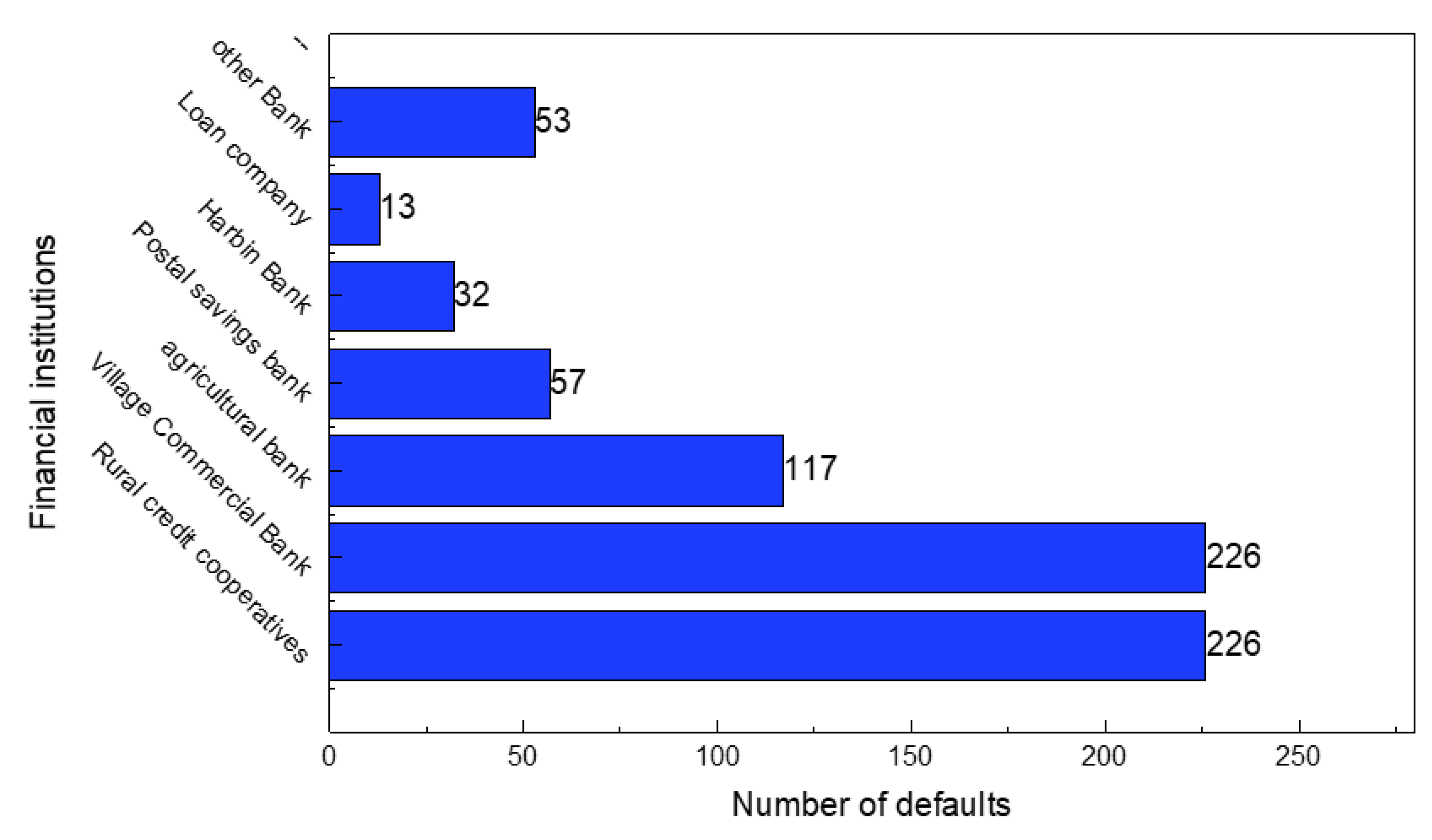

Figure 4 shows the financial institutions and the number of farmland mortgage default cases during 2014–2020. Figure 4 indicates that rural credit cooperatives and village commercial banks are involved in the most default cases, followed by the Agricultural Bank of China. The first consideration of financial institutions issuing loans is the security, profitability, and liquidity of loans. Farmland mortgage loans entail high risk, have a long cycle and offer poor profit-making, so financial institutions are often not willing to carry out such businesses. Rural credit cooperatives, village commercial banks and the Agricultural Bank of China have been engaged in the rural market for a long time, with their main business being related to agricultural funds, but other financial institutions rarely participate.

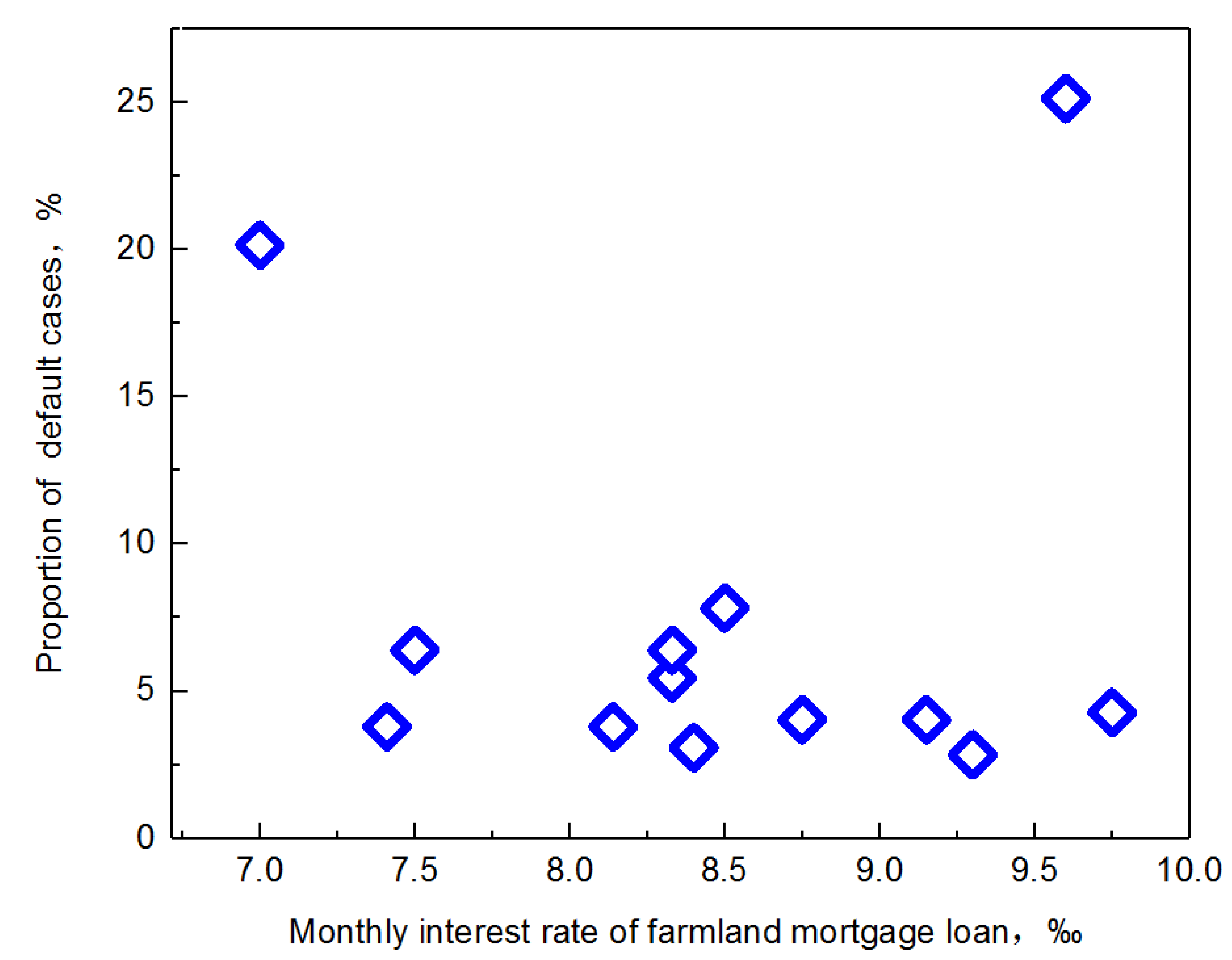

In the statistical cases of farmland mortgage default, the monthly interest rate is concentrated between 7‰ and 10‰. Figure 5 shows the proportion of default cases of farmland mortgage with monthly interest rate between 7‰ and 10‰. The default cases with monthly interest rate of 7‰ and 9.6‰ accounted for 20.14% and 25.12%, respectively. In addition, the highest monthly interest rate is 14.895‰, and the lowest is 3.9887‰. Most loan contracts stipulate that after overdue, the monthly interest rate will be charged 50% as penalty interest based on the original interest rate. Additionally, there are eight contracts provide for a 30% rise in lending rates at the same level of benchmark lending rates at the People’s Bank of China over the same period.

4. Discussion

4.1. Reasons for Farmland Mortgage Default

4.1.1. Frequent Agriculture Natural Disasters

China is a traditional agricultural country. As a developing country, China’s agricultural infrastructure construction has received increasing attention, but it is still relatively weak. Agricultural natural disasters are the main cause of farmers’ losses. Changes in natural conditions bring many uncertain factors to agricultural production and management [42]. Only from the data since the beginning of the new century, the annual loss of grain due to drought in China is as high as more than 30 billion kg, about 6% of the total grain output in the same period [43]. Failures in agricultural land management make farmers unable to repay loans. Turvey and Norton [44] proposed that the core assumption is that there exists a covariate relationship between the underlying weather event and crop loss. Its general form is given as follows:

where

Natural disasters can significantly reduce agricultural output.

Table 3 [45] indicates that the losses caused by agricultural natural disasters are great. Agricultural insurance is not common in China, and agricultural risk mainly depends on farmers’ self-relief. At the current stage, agricultural income is still the main economic source of agricultural operators and the first source of funds to repay mortgage loans. Once a large-scale natural disaster occurs, agricultural operators suffer great economic losses, are unable to repay loans and therefore violate the land management right mortgage contract.

4.1.2. Huge Agricultural Market Risk

Agricultural system is not only highly dependent on the natural environment, but also highly dependent on the market [46,47]. Once the market environment changes adversely, it will bring serious uncertainty and uncontrollable to agricultural production.

The Chinese agricultural market is underdeveloped, and the distribution is different. Eastern China has a large number and large scale of production market, which has a significant role in promoting industry and agricultural products circulation, while the central and western regions have a small number of production market and low construction standards. The trading and settlement of the origin market is relatively backward, inefficient and risky, and it is difficult to form an open and fair transaction price.

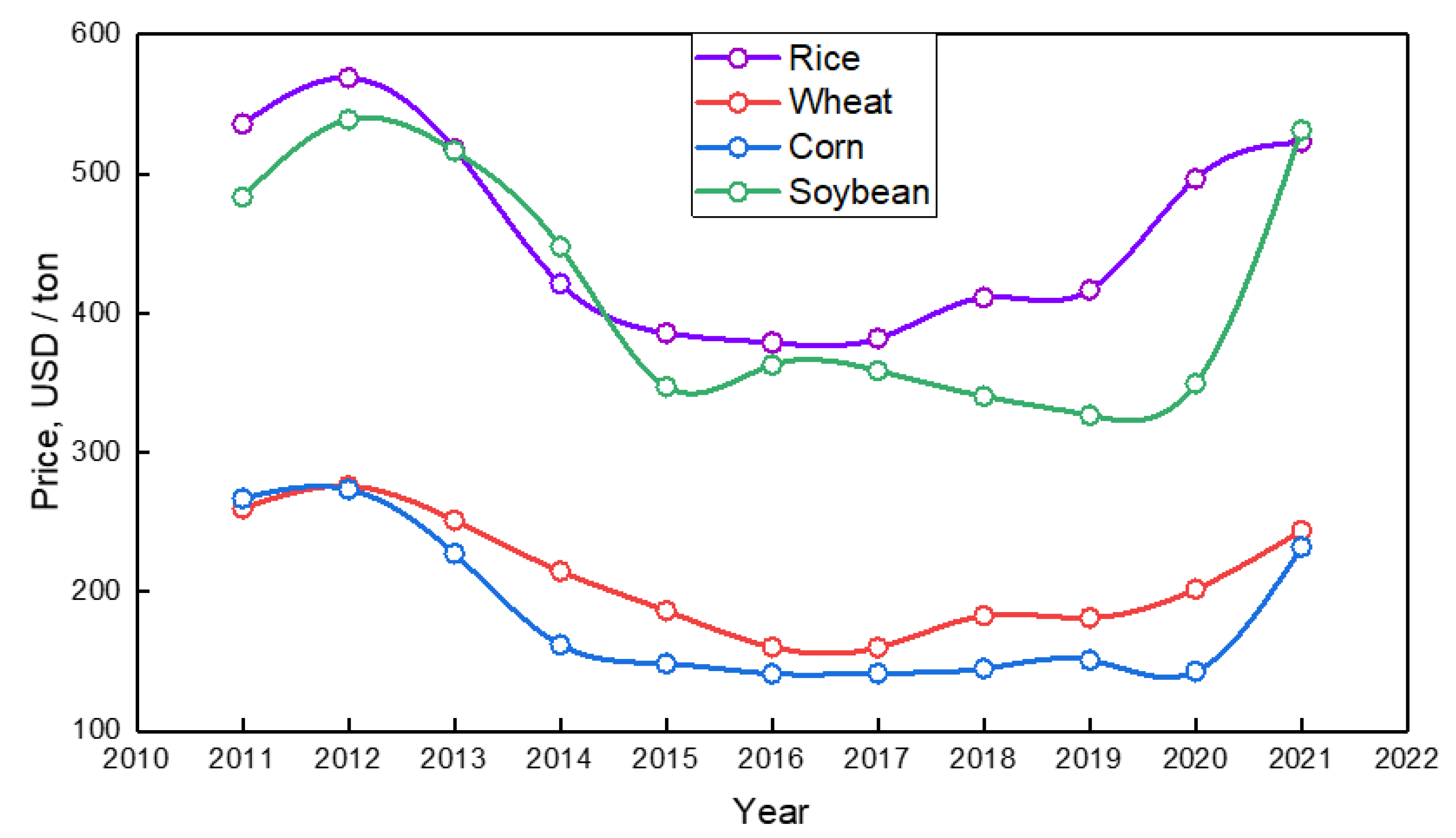

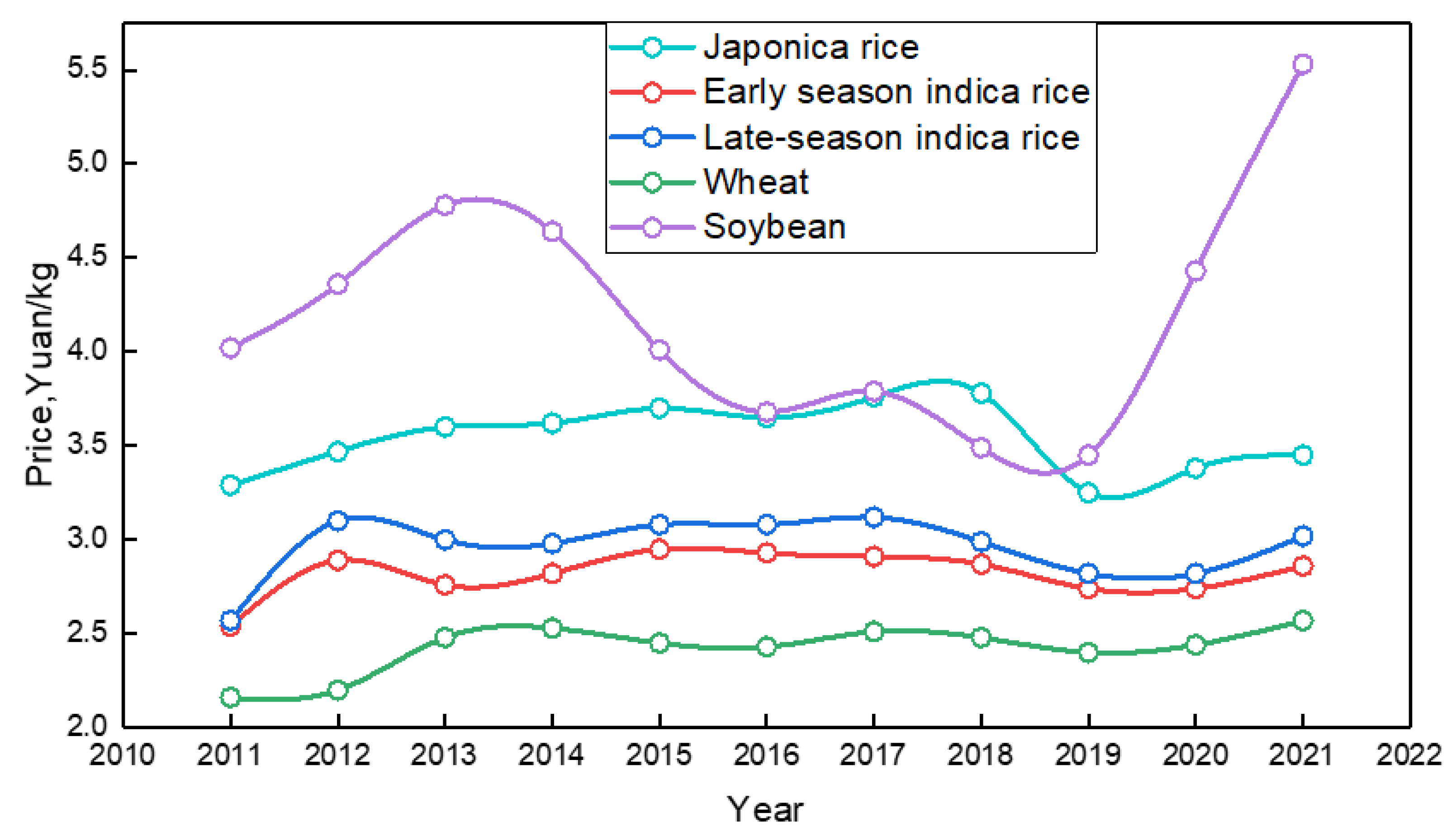

Under the background of economic globalization, agriculture is faced with not only domestic market risks, but also international market risks. The uncertainty of market risks increases (Figure 6), many factors are often superimposed, and the price fluctuates greatly. International grain price fluctuations and impact on Chinese grain prices (Figure 7).

4.1.3. High Cost of Agricultural Production

Chinese agriculture has entered the era of high production cost. In the increment of agricultural production input, the increase of direct production cost is the main factor to promote the increase of total agricultural production cost. Costs of seeds, fertilizers, pesticides, agricultural films, machinery operations, irrigation and drainage, land rent, labor, etc., accounting for over 80% of total costs [48].

High production costs have pushed up food prices, reduced agricultural operating income and damaged agricultural competitiveness. As shown in Table 4, the domestic grain price is close to or even higher than the international grain import to the shore tax price, the grain trade deficit situation, and this situation is expanding year by year.

4.1.4. Low Efficiency of Agricultural Production

In the process of promoting the large-scale operation of agricultural services in China, a series of problems, such as the small scale of agricultural land, the high degree of fragmentation, the small farmers as the main body of agricultural management and the insufficient supply of services, limit the full stimulation of the large-scale benefits of agricultural services.

As of July 2020, the cultivated land area under household contracts was 1,545,766,706 mu and the number of farmers under household contracts was 220,040,147. The average land contracted by each household was 2.48 mu. The details are as follows in Table 5.

There are more than 200 million agricultural operators in China, and the average cultivated land area is only 7 mu, which is only 1/40 of the European Union and 1/400 of the United States [49] Agricultural labor productivity is approximately 47% of the world average, 2% of high-income countries and 1% of the United States. China’s current land per labor and household arable land is no more than 10 mu, which is not only significantly below the world average, but also significantly below the Asian average [50]. Scholars have studied the functional equation of grain yield and its influencing factors in China for a long time [51,52]. The law of diminishing returns is in operation as more physical inputs are applied to shrinking land. Small-scale agriculture results in low agricultural productivity high unit production costs, low agricultural income and weaken the ability of farmers to resist natural disasters. When farmers’ input is greater than output, they may be unable to repay the loan and default.

4.1.5. Poor Credit Environment in Rural Areas

Of the 724 judgements, 570 were judged by default because the defendant (the borrower) did not appear in court. As the whereabouts of the defendant (the borrower) were unknown, three cases of prosecution were rejected by the court. Some agricultural operators do not actively communicate with the lenders or appear in court when they breach the contract. Instead, they take a negative attitude and let the court dispose of the mortgaged land management right. This reflects a lack of contract spirit and legal thinking among agricultural operators and suggests that the agricultural operators do not value the land.

Since the reform and opening-up in 1978, with the development of China’s social economy, people’s demands regarding the legal environment have become increasingly urgent. The legal environment of China has been greatly improved, as has citizens’ legal consciousness. However, due to the imbalance of China’s social and economic development, the legal environment in the vast rural areas is relatively poor, which is manifested in the poor legal awareness of farmers, the weak legislation in rural and agricultural areas, the insufficient legal popularization in rural areas, the greater use of power than law in the management of rural affairs, etc. [53]. In the current situation, farmers’ awareness of contracts is relatively poor, the cost of enforcing farmers’ performance is very high and there are high social risks. At present, there are no effective measures to solve this problem.

4.1.6. Gradually Weakening the Land Restrictions for Farmers

In recent years, a large number of rural laborers have transferred to cities. Table 6 shows that the rural population of migrant workers reached 287 million in 2017, as massive farmers left their homes and went to cities for employment. The phenomenon of rural land transfer and the separation of people and land has become very common. The new generation of farmers accounts for 49.7% of the total number of migrant workers; they hardly participate in agricultural production, have long been accustomed to urban life, and are unwilling to engage in farm work. In addition, due to the low income from farming and the fragmentation of cultivated land, some agricultural areas have been abandoned. In the mountainous areas of Southern Henan and Western Hunan, the proportion of abandoned farmland is close to one quarter [54]. The restriction of land to farmers is gradually weakening. Land is no longer important to agricultural operators. Some agricultural operators choose to give up the right of land management and do not repay the loan. Farmers become part-time farmers and even urban workers. The cost of default to agricultural operators is low, which leads to high moral hazard.

The sharp decrease in the agricultural labor force will have a great impact on Chinese farms, making it a very serious problem. The Chinese government has paid attention to this problem. In 2014, the State Council proposed cultivating new agricultural operators, focusing on those whose land management scale is equivalent to 10 to 15 times the average contracted land area of local households.

4.1.7. High Interest Rates of Loans

The interest rate of rural land mortgage loans in China is higher than that in developed countries [55,56]. With the penalty interest after loans become overdue, the interest and penalty interest of some loan cases exceed the loan principal. When applying for loans, some rural land operators do not carefully read the terms of the contract or do not seriously consider the consequences of the interest rate and penalty interest. Once default occurs, farmers have a sense of being deprived of value and then turn to negative non-cooperation, allowing the court to decide.

4.2. Methods for Reducing Farmland Mortgage Default

Farmers are the main demanders of the rural financial market, and their credit default constitutes the main source of the credit risk of rural cooperative financial institutions. Therefore, improving the loan repayment rate of farmers and reducing default are fundamental to realize the virtuous cycle of rural land mortgages.

4.2.1. Strengthen Agricultural Insurance

Agricultural insurance is an effective means to disperse and resolve agricultural risks and has become an important part of many countries’ agricultural policy systems [57,58,59,60]. In addition, agricultural insurance is a “green box” policy in line with the provisions of the agricultural agreement and is an important non-price agricultural protection tool. However, in recent years, the efficiency of China’s agricultural insurance premium subsidies has been weakened, and there are unsustainable risks in policy agricultural insurance. There are still other problems in China’s agricultural insurance, such as a low level of security, narrow insurance liability, and claim conditions. Therefore, we need to improve agricultural insurance policy, expand the scope of insurance, and increase the number of claims. When agricultural land operators encounter natural or market risks in agricultural production, they should reduce losses through insurance and increase the source of funds for the repayment of mortgages based on land management rights.

Through various publicity methods, farmers can be encouraged to correctly understand the role of agricultural insurance and the related policies of agricultural insurance to improve their recognition of agricultural insurance and effectively protect their own interests.

4.2.2. Cultivation of Farmers’ Contract Spirit

The market economy is both a contract economy and a legal economy, and rural land operators should strengthen their contract consciousness and legal spirit. When disasters affect agricultural production and farmers cannot repay loans in time, we should actively negotiate with the lender to formulate a practical and feasible repayment plan. Based on the unique geographically based relationships in the countryside, village committees should play a role in improving the rural credit environment, collect comprehensive credit information about farmer households, establish a complete credit information database, and employ professionals to systematically manage the credit information database to enhance the binding force of credit on farmer households. The evaluation of farmers’ credit should be carried out under a unified standard to ensure fairness and transparency.

4.2.3. Reduce the Loan Interest Rate

Rural land finance needs the government to provide subsidies through credit. At present, China’s rural land mortgage interest rate is generally high, which is not conducive to the development of this business and increases the burden of rural land operators. By comparison, it can be seen that in the United States, the monthly interest rate of land mortgage loans is usually 4%~6%, while in Germany, the monthly interest rate of land mortgage loans is less than 5% [56,57]. It is urgent to reduce the mortgage interest rate of land management rights and reduce the burden of agricultural land operators. This can also effectively reduce the risk of adverse selection.

4.2.4. “Project Pool” Mode

The practice of Wucheng County in Shandong Province is worth learning from. Wucheng County initiated the “project pool” mechanism for undertaking mortgage loans for land management rights and establishing risk prevention [61]. In the project pool, high-quality subjects with good operating conditions and high reputation are selected from the new agricultural operating subjects in the county and given preferential policies, such as agricultural project support and financial support. When a borrower is unable to repay a loan through normal operation, the mortgaged land management right is undertaken by other subjects in the project pool, who continue to pay the farmers’ land rent and repay the bank loan with part of the aboveground facilities. This reduces the loan risk of the bank and enables the bank to dispose of the land management rights of a borrower who violates the rules in the later stage. In addition, the county took the lead in the development and construction of a rural comprehensive property rights information sharing system, which helps banks understand the operating situation of collateral and borrowers, thus solving the problem of information asymmetry and reducing the risk to the bank.

5. Conclusions

The reform of rural land ownership, contract rights and management rights not only represent an innovation of the rural land system with Chinese characteristics but is also the only way to develop modern agriculture. At present, rural land mortgage has been carried out all over the country, but the empirical research on rural land mortgage default is few. According to the court’s judgment, this paper comprehensively analyzed the characteristics of defaults in different regions of China during 2014–2020 and explained them. This can provide a reference for the governance of default risk of rural land mortgage. In the field of recessive transformation of agricultural land use, the topic is also worth studying.

The number of farmland mortgage defaults reached a peak in 2018, and since then, the value declined year by year, which confirmed that after the separation of the management rights of contracted rural land from the management rights of contracted land, farmers’ farmland mortgage loans could be protected by law, and the default risk of farmland mortgage still exists, but it has been reduced.

The mortgage loan defaults for rural land management rights amounting to less than CNY 100,000 accounted for the largest proportion, 54.7%. A small loan amount can promote a balanced distribution between the loan amount and the borrower’s income and effectively disperse the liquidity risk. These borrowers may have a weak ability in avoiding risk and could be prone to moral hazard. For these borrowers, more preferential loans or financial assistance should be considered. The default events of mortgage loans for rural land management rights concerned mainly 1-year short-term loans, which was consistent with the actual situation. To reduce the risk of farmers’ default, the term of bank loans was generally limited to one year.

China’s financial institutions mainly issue short-term agricultural loans (within 3 years), with a typical loan term of 12 months. Default cases are concentrated in the loan term of 6–12 months, of which defaults in the loan term of 12 months accounts for more than 40%.

The average age of agricultural labor force is 48.5 years old. Nearly 50-year-old men have become the main force of agriculture, of which more than 60% are full-time agricultural producers. Therefore, most of the households with loan demand and behavior are those whose head of household is over 40 years old, which also leads to the farmers in this age group may become the main body of default.

Natural disasters are the main cause of farmers’ default. The annual loss of grain caused by drought alone in China is as high as more than 30 billion kg, about 6% of the total grain output in the same period. The failure of agricultural land management caused by natural disasters makes farmers unable to repay loans and result in default.

There are few financial institutions involved in farmland mortgage, which are not easy to share risks. It is recommended to expand financial institutions involved in farmland mortgage. These findings are not only a summary of the current situation of rural land mortgage default in China, but also the first-hand information on empirical research on rural land mortgage default, which can provide reference for the governance of rural land mortgage default risk.

The deficiency of this article lies in that this article makes only descriptive statistics on the default judgments of rural land management right mortgage loans from 2014 to 2020 in China, the data obtained from the court judgments can truly reflect the farmers’ default. There are also limitations regarding cases of defaults that were addressed by the court. For example, some cases of “de facto default” have not been granted a trial, so this part of the data cannot be obtained from the court. We discussed only the default cases judged by the court in this article. This is a work that needs to be further promoted. In follow-up research, it is necessary to conduct in-depth interviews to explore the institutional, individual, and natural causes of rural land management right mortgage default in China. It will be more helpful to reveal the formation mechanism of the default risk of rural land management rights and mortgage loans in China, clarify the current situation and characteristics of the default of rural land mortgage loans, and put forward suggestions for preventing the default risk of rural land mortgage loans.

China’s land system reform needs to pay attention to some problems. The first is clearing property relations. At present, the question as to whether rural land management right is a property right or creditor’s right is controversial, which is directly related to the protection of property right or creditor ‘s right. In addition, the content of land contract management right and land management right is not clear, which affects the practical effect of land contract management right and land management right. The second problem is a sound assessment system. At present, due to the lack of professional evaluation institutions and scientific evaluation standards, the real value of collateral cannot be accurately reflected in agricultural land mortgage. Therefore, it is necessary to improve the evaluation institutions, cultivate professional talents and improve the evaluation methods to effectively protect the legitimate rights and interests of all parties in the process of agricultural land mortgage. The third is supervision of land use. The Food and Agriculture Organization of the United Nations has set the warning line for arable land at 0.8 mu per capita, and no mortgage is allowed for arable land below 0.8 mu per capita. In the process of farmland mortgage, the tendency of farmland’s “non-agriculturalization” and “non-grain growing” should be eliminated to ensure that “the land use is not changed and the comprehensive agricultural production capacity is not destroyed” and that the red line of 1.8 billion mu of farmland will not be broken.

Author Contributions

This is the independent work of the authors; investigation, original draft, writing and editing, H.Z.; theoretical direction, Z.Z. Both authors have read and agreed to the published version of the manuscript.

Funding

This research was supported by Ministry of education Youth Fund for Humanities and Social Sciences Research (Grant No. 15YJCZH239).

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Li, J. Analysis of Agricultural Product Brand Marketing Strategy. Financ. Eng. Risk Manag. 2020, 3, 61–64. [Google Scholar]

- Zhuo, Y.F.; Xu, Z.G.; Li, G.; Liao, R.; Christiaan, L.; Wu, C.F.; Wu, Y. LADM-based profile for farmland Tripartite Entitlement System in China. Land Use Policy 2020, 92, 104459. [Google Scholar] [CrossRef]

- Wang, Q.; Zhang, X. Three rights separation: China’s proposed rural land rights reform and four types of local trials. Land Use Policy 2017, 63, 111–121. [Google Scholar] [CrossRef]

- Xu, Y.; Huang, X.; Bao, H.X.; Ju, X.; Zhong, T.; Chen, Z.; Zhou, Y. Rural land rights reform and agro-environmental sustainability: Empirical evidence from China. Land Use Policy 2018, 74, 73–87. [Google Scholar] [CrossRef]

- Zhou, Y.; Guo, L.; Liu, Y. Land consolidation boosting poverty alleviation in China: Theory and practice. Land Use Policy 2019, 82, 339–348. [Google Scholar] [CrossRef]

- Zhou, Y.; Guo, Y.; Liu, Y.; Wu, W.; Li, Y. Targeted poverty alleviation and land policy innovation: Some practice and policy implications from China. Land Use Policy 2018, 74, 53–65. [Google Scholar] [CrossRef]

- Yang, Z.; Xunhuan, L.; Yansui, L. Rural land system reforms in China: History, issues, measures and prospects. Land Use Policy 2020, 91, 104330. [Google Scholar]

- Qing-ling, H. On Agricultural Land System Reform—From the Perspective of Land Order and Land Cognition. Soc. Sci. Beijing 2016, 5, 22–30. [Google Scholar]

- Zou, Q.R. Property Right and Institutional Change: An Empirical Study of China’s Reform; Peking University Press: Beijing, China, 2004. [Google Scholar]

- Aditya, R.K.; Omobolaji, O. Rural Finance, Capital Constrained Small Farms, and Financial Performance: Findings from a Primary Survey. J. Agric. Appl. Econ. 2020, 52, 288–307. [Google Scholar]

- Chizoba, P.A.; Nneamaka, O.T.N.; Cynthia, O. Relationship between Rural Finance Institution Services and Standard of Living of Rural Farming Households in Anambra State, Nigeria. Asian J. Agric. Ext. Econ. Sociol. 2020, 102–109. [Google Scholar] [CrossRef]

- Long, H.L.; Li, X.B. Analysis on regional land use transition: A case study in transect of the Yangze River. J. Nat. Resour. 2002, 17, 144–149. [Google Scholar]

- Long, H.L.; Qu, Y.; Tu, S.; Zhang, Y.; Jiang, Y.F. Development of land use transitions research in China. J. Geogr. Sci. 2020, 30, 1195–1214. [Google Scholar] [CrossRef]

- Long, H.L.; Zhang, Y. Rural planning in China: Evolving theories, approaches, and trends. Plan. Theory Pract. 2020, 21, 782–786. [Google Scholar] [CrossRef]

- Long, H.L. Land Use Transitions and Rural Restructuring in China; Springer Nature: Singapore, 2020. [Google Scholar]

- Li, M.; Long, H.L.; Tu, S.S.; Zhang, Y.N.; Zheng, Y.H.; Yang, R. Farmland transition in China and its policy implications. Land Use Policy 2020, 92, 104470. [Google Scholar]

- Long, H.L.; Zou, J.; Pykett, J.; Li, Y.R. Analysis of rural transformation development in China since the turn of the new millennium. Appl. Geogr. 2011, 31, 1094–1105. [Google Scholar]

- Mishra, A.K.; Moss, C.B.; Erickson, K.W. The Role of Credit Constraints and Government Subsidies in Farmland Valuations in the US: An Options Pricing Model Approach. Empir. Econ. 2008, 34, 285–297. [Google Scholar] [CrossRef]

- Johnson, J. Rural Economic Development in the United States: An Evaluation of the US Department of Agriculture’s Business and Industry Guaranteed Loan Program. Econ. Dev. Q. 2009, 23, 229–241. [Google Scholar] [CrossRef]

- Fang, Q.M.; Luo, J.C.; Cai, Q.H. The Optimal Land Scale under the Maximum Willingness of Rural Land Mortgage Financing. J. South China Agric. Univ. Soc. Sci. Ed. 2016, 6, 49–57. [Google Scholar]

- Zhan, Z.M.; Luo, J.C. Logistic-DEA-Model-Based Assessment of Risk Control Effect of Rural Land Contract and Management Rights Mortgage Pilot. Wuhan Univ. J. 2016, 69, 47–54. [Google Scholar]

- Lin, J.W. Risks and precaution of mortgage of farmland management right. J. Fujian Agric. For. Univ. 2016, 19, 14–19. [Google Scholar]

- Zhao, Y.Z.; Wang, Q. The Risk Management of the Rural Land Contracted Management Right Mortgage Loan: From the Perspective of Agriculture-related Financing Institutions. J. Anhui Agric. Univ. 2015, 24, 12–16. [Google Scholar]

- Hui, X. Exploration and path selection of rural land mortgage financing practice mode—Based on the empirical observation of rural land finance pilot. Southwest Financ. 2014, 3, 66–71. [Google Scholar]

- Peng, Y.; Liu, W.B.; Tan, C. Study on Risks in Mortgage Financing of Rural Land Management Right. In Proceedings of the 2017 6th International Conference on Social Science, Education and Humanities Research (SSEHR 2017), Jinan, China, 18 October 2017. [Google Scholar]

- Pan, W. On the Risks of Rural Land Management Right Mortgage Loan. J. Nanjing Agric. Univ. 2015, 5, 104–113. [Google Scholar]

- Lihong, Y. Credit risk evaluation of rural land management right mortgage—Based on AHP analysis. Rural Econ. 2014, 11, 79–82. [Google Scholar]

- Chao, W.; Liao, Y.; Wang, M. Research on Farmland Mortgage Loan Risk Evaluation Based on AHP-Fuzzy Comprehensive Evaluation Method. J. Hebei Norm. Univ. Sci. Technol. 2014, 13, 38–43. [Google Scholar]

- Dehong, L.; Wuke, Z. Influential Factors and Measuring of Credit Risk on Rural Land Contract Right Mortgage Loan—Estimation Based on CreditRisk+ Model. J. Huazhong Agric. Univ. 2018, 4, 137–147. [Google Scholar]

- Qicai, Y.; Xie, L.; Wenlong, H. The Realization and Risk of Mortgage Loan Based on Agricultural Land Using Rights: A Comment on the Practices and Case. Probl. Agric. Econ. 2015, 10, 4–11. [Google Scholar]

- Liu, Y.X.; Min, J.; Liu, Y. Identification and Evaluation of Mortgage Financing Risk of Agricultural Land Management Right under the ‘Threepower Split’: An Empirical Study Based on Structural Equation Model. Macroeconomics 2019, 1, 158–175. [Google Scholar]

- Christen, R.P.; Pearce, D. Managing Risks and Designing Products for Agricultural Microflnance: Features of an Emerging Model; Consultative Group to Assist the Poor (CGAP): Washington, DC, USA, 2005; pp. 1–44. [Google Scholar]

- Ruslana, S.; Oksana, A.; Olha, H.; Kateryna, M. Mortgage Lending in the Agricultural Economy: Opportunities and Risks. Financ. Credit Act. Probl. Theory Pract. 2019, 1, 225–233. [Google Scholar]

- Yin, K.X.; Lan, Q.G.; Kan, S.S.; Su, Y.D. Empirical Research on the Risk Mea surement of Mortgage Loans on Rural Land Contract and Management Rights: A Case Study of Heilongjiang Province. J. Coast. Res. 2020, 103, 226–230. [Google Scholar] [CrossRef]

- Ge, Y.; Yu, L.; Shu, Z.; Chen, Z. Data Augmentation for Deep Learning of Judgment Documents. In Proceedings of the IScIDE 2019 Intelligence Science and Big Data Engineering, Big Data and Machine Learning, Nanjing, China, 17–20 October 2019; pp. 232–242. [Google Scholar]

- Yuan, J.; Wei, Z.; Gao, Y.; Chen, W.; Song, Y.; Zhao, D.; Ma, J.; Hu, Z.; Zou, S.; Li, D.; et al. Overview of SMP-CAIL2020-Argmine: The Interactive Argument-Pair Extraction in Judgement Document Challenge. Data Intell. 2021, 3, 287–307. [Google Scholar]

- The State Council’s Summary Report on the Pilot Project of Operating Right of Contracted Land and Mortgage Loan of Farmers’ Housing Property Right in Rural Areas. Available online: http://www.npc.gov.cn/npc/c12435/201812/2067ecc784a8437cbe8780a32bcf48ac.shtml (accessed on 23 December 2018).

- Overview of Agricultural and Rural Areas in Heilongjiang Province, Agricultural and Rural Department of Heilongjiang Province. Available online: http://nynct.hlj.gov.cn/jggk/nygk/2020/index.htm (accessed on 1 January 2021).

- The Balance of Rural Contracted Land Management Right Mortgage Loan Reached 7.955 Billion Yuan. The “Two Rights” Mortgage Loan Revitalized the “Sleeping” Resources. Available online: https://www.hlj.gov.cn/zwfb/system/2018/01/08/010859158.shtml (accessed on 8 January 2018).

- Zhang, Y.Y. Research on the Influencing Factors and Control of Credit Risk of Rural Cooperative Financial Institutions in Shanxi Province. Ph.D. Thesis, Northwest Agriculture & Forestry University, Xianyang, China, 2015. [Google Scholar]

- The Voice of Chinese Countryside. Available online: http://country.cnr.cn/gundong/20181231/t20181231_524467209.shtml (accessed on 29 December 2018).

- State Statistical Yearbook. Available online: https://data.stats.gov.cn/easyquery.htm?cn=C01 (accessed on 11 July 2021).

- Ding, Y.G.; Sun, Q.X. Does agricultural insurance mitigate the negative impac of natural disaster on the agricultural economy? Theory Pract. Financ. Econ. 2021, 42, 43–49. [Google Scholar]

- Turvey, C.G.; Norton, M. An internet-based tool for weather risk management. Agric. Resour. Econ. Rev. 2008, 37, 63–78. [Google Scholar] [CrossRef]

- Rosenzweig, M.R.; Binswanger, H.P. Wealth, Weather Risk and the Composition and Profit Ability of Agricultural Investments. Econ. J. 1993, 103, 56–78. [Google Scholar] [CrossRef] [Green Version]

- Yoji, K.; Gen, S.; Toshichika, I. Systemic Risk in Global Agricultural Markets and Trade Liberalization under Climate Change: Synchronized Crop-Yield Change and Agricultural Price Volatility. Sustainability 2020, 12, 10680. [Google Scholar]

- Moschini, G.; Hennessy, D.A. Chapter 2 Uncertainty, risk aversion, and risk management for agricultural producers. Handb. Agric. Econ. 2001, 1, 87–153. [Google Scholar]

- Wan, B.R. Chinese agriculture has entered the era of high production cost. People’s Daily, 13 March 2014. [Google Scholar]

- Han, C.F. Rural land reform in China. In Proceedings of the 40-Year Symposium on Rural Reform of the Ministry of Agriculture and Rural Affairs, Beijing, China, 4 December 2018. [Google Scholar]

- Lin, W.L. Farmland operation scale: International experience and Chinese realistic choice. Probl. Agric. Econ. 2017, 7, 33–42. [Google Scholar]

- Battese, G.E.; Coelli, T.J. Prediction of Firm-Level of Technical efficiencies with a Generalised Frontier Production Function and Panel Data. J. Econom. 1988, 38, 387–399. [Google Scholar] [CrossRef]

- Yao, S.; Liu, Z. Determinants of Grain Production and Technical Efficiency in China. J. Agric. Econ. 1998, 49, 171–184. [Google Scholar] [CrossRef]

- The Survey Report of Migrant Workers in 2019. Available online: http://www.stats.gov.cn/tjsj/zxfb/202004/t20200430_1742724.html (accessed on 30 April 2019).

- Wei, H.K.; Yan, K. Report on China’s Rural Development—To Stimulate New Energy of Rural Development by Comprehensively Deepening Reform; China Social Science Press: Beijing, China, 2017; p. 17. [Google Scholar]

- Cheng, Y.; Wang, B. Foreign farmland mortgage loan. Land Resour. 2016, 1, 50–53. [Google Scholar]

- Babić, L. Comparison of Agricultural Insurance Development of Croatia, EU and USA. Poljoprivreda 2014, 20, 49–52. [Google Scholar]

- Ministry of Finance of the PRC. Available online: http://jrs.mof.gov.cn/zhengcefabu/201910/t20191012_3400537.htm (accessed on 19 September 2019).

- Yarmolenko, V.V. The Factors’ Influence on the Functioning of the Agricultural Insurance Market. Bìznes Ìnform 2019, 9, 144–151. [Google Scholar]

- Rokicki, T. The agricultural insurance market in Poland. Rocz. Nauk. Stowarzyszenia Ekon. Rol. Agrobiz. 2018, 1, 117–122. [Google Scholar] [CrossRef] [Green Version]

- Ranjan, K.G.; Shweta, G.; Vartika, S. Demand for Crop Insurance in Developing Countries: New Evidence from India. J. Agric. Econ. 2021, 72, 293–320. [Google Scholar]

- China Rural Network. Available online: http://journal.crnews.net/ncgztxcs/2020/dsbq/dc/139687_20200929111724.html (accessed on 29 September 2020).

Figure 1.

Annual distribution of 724 farmland mortgage default events in China from 2014 to 2020.

Figure 2.

Number of default events of farmland mortgages during 2014–2020.

Figure 3.

Age of the household head and the loan term of default farmland mortgage loans in Heilongjiang Province, starting time of loan, 2014–2020.

Figure 3.

Age of the household head and the loan term of default farmland mortgage loans in Heilongjiang Province, starting time of loan, 2014–2020.

Figure 4.

Financial institutions and the number of farmland mortgage default cases during 2014–2020.

Figure 4.

Financial institutions and the number of farmland mortgage default cases during 2014–2020.

Figure 5.

Farmland mortgage monthly interest rate.

Figure 6.

International grain prices, 2011–2021 (Ministry of Agriculture and Rural Affairs of the People’s Republic of China).

Figure 6.

International grain prices, 2011–2021 (Ministry of Agriculture and Rural Affairs of the People’s Republic of China).

Figure 7.

Annual changes of major grain purchase prices in China, 2011–2021 (Ministry of Agriculture and Rural Affairs of the People’s Republic of China).

Figure 7.

Annual changes of major grain purchase prices in China, 2011–2021 (Ministry of Agriculture and Rural Affairs of the People’s Republic of China).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

The default amount and proportion of farmland mortgages.

| Loan Amount, CNY 10,000 | Numbers | Ratio, % |

|---|---|---|

| 0 < x ≤ 5 | 152 | 21 |

| 5 < x ≤ 10 | 244 | 33.7 |

| 10 < x ≤ 20 | 139 | 19.2 |

| 20 < x ≤ 50 | 84 | 11.6 |

| 50 < x ≤ 100 | 47 | 6.5 |

| 100 < x | 58 | 8 |

| Total | 724 | 100 |

Table 2.

Default amount of farmland mortgage loans with the borrower being a company or agricultural operation organization.

Table 2.

Default amount of farmland mortgage loans with the borrower being a company or agricultural operation organization.

| Loan Amount, CNY 10,000 | Numbers | Ratio, % |

|---|---|---|

| ≤10 | 1 | 3.33 |

| 20 ≤ x ≤ 50 | 4 | 13.33 |

| 50 < x ≤ 100 | 4 | 13.33 |

| >100 | 21 | 70 |

| Total | 30 | 100 |

Table 3.

Agricultural natural disasters in China during 2010–2019.

| Index, 103 HA | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 |

|---|---|---|---|---|---|---|---|---|---|---|

| Covered Area | 37,426 | 32,471 | 24,962 | 31,350 | 24,891 | 21,770 | 26,221 | 18,478 | 20,814 | 19,257 |

| Covered by Flood | 17,525 | 6863 | 7730 | 8757 | 4718 | 5620 | 8531 | 5415 | 3950 | 6680 |

| Covered by Drought | 13,259 | 16,304 | 9340 | 14,100 | 12,272 | 10,610 | 9873 | 9875 | 7712 | 7838 |

| Covered by wind and hail | 2180 | 3309 | 2781 | 3387 | 3225 | 2918 | 2908 | 2268 | 2407 | |

| Covered by freezing | 4121 | 4447 | 1618 | 2320 | 2133 | 900 | 2885 | 525 | 3413 | |

| Affected Area | 18,538 | 12,441 | 11,475 | 14,303 | 12,678 | 12,380 | 13,670 | 9201 | 10,569 | 7913 |

| Affected by Flood | 7024 | 2840 | 4145 | 4859 | 2704 | 3327 | 4338 | 3022 | 2551 | 2612 |

| Affected by Drought | 8987 | 6599 | 3509 | 5852 | 5677 | 5863 | 6131 | 4444 | 2621 | 3332 |

| Affected by Hail | 916 | 1348 | 1368 | 1682 | 2193 | 1825 | 1424 | 1238 | 1548 | |

| Affected by Freezing | 1444 | 1291 | 795 | 885 | 933 | 474 | 1179 | 312 | 1870 |

Table 4.

Changes in Foreign Trade of Agricultural Products in China from 2011 to 2019 (billion USD) 1.

Table 4.

Changes in Foreign Trade of Agricultural Products in China from 2011 to 2019 (billion USD) 1.

| Year | Import and Export Volume | Exports | Imports | Exports − Imports |

|---|---|---|---|---|

| 2011 | 1556.23 | 607.51 | 948.72 | −341.21 |

| 2012 | 1757.68 | 632.89 | 1124.79 | −491.90 |

| 2013 | 1866.92 | 678.25 | 1188.67 | −510.42 |

| 2014 | 199.29 | 719.60 | 1225.38 | −505.78 |

| 2015 | 1875.62 | 706.82 | 1168.81 | −461.99 |

| 2016 | 1845.55 | 729.86 | 115.69 | −385.83 |

| 2017 | 2013.88 | 755.32 | 1258.56 | −503.24 |

| 2018 | 2177.08 | 804.48 | 1372.60 | −568.12 |

| 2019 | 2300.68 | 790.98 | 1509.70 | −718.72 |

1 Ministry of Agriculture and Rural Affairs of the People’s Republic of China.

Table 5.

Farmland scale of farmers in China, 2020 1.

| Farmland Scale (mu) | Farm Household (Ten Thousand) |

|---|---|

| <10 | 23,661.7 (2.561 million households not operating cultivated land) |

| 10–30 | 2966.7 |

| 30–59 | 706.5 |

| 50–100 | 283.6 |

| 100–200 | 104.9 |

| >200 | 47.2 |

1 China Rural Policy and Reform Statistics Annual Report 2019.

Table 6.

Number of migrant workers in China during 2015–2019.

| Year | 2015 | 2016 | 2017 | 2018 | 2019 |

|---|---|---|---|---|---|

| Number of migrant workers, 10,000 | 27,747 | 28,171 | 28,652 | 28,836 | 29,077 |

| Number of migrant workers in the province, 10,000 | 9139 | 9268 | 9672 | 9510 | 9917 |

Data source: from 2015 to 2019 “migrant workers monitoring survey report”.

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Zheng, H.; Zhang, Z. Analyzing Characteristics and Implications of the Mortgage Default of Agricultural Land Management Rights in Recent China Based on 724 Court Decisions. Land 2021, 10, 729. https://doi.org/10.3390/land10070729

AMA Style

Zheng H, Zhang Z. Analyzing Characteristics and Implications of the Mortgage Default of Agricultural Land Management Rights in Recent China Based on 724 Court Decisions. Land. 2021; 10(7):729. https://doi.org/10.3390/land10070729

Chicago/Turabian StyleZheng, Hongguang, and Zhanbin Zhang. 2021. "Analyzing Characteristics and Implications of the Mortgage Default of Agricultural Land Management Rights in Recent China Based on 724 Court Decisions" Land 10, no. 7: 729. https://doi.org/10.3390/land10070729

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.