Estimating the Impact of Tobacco Parity and Harm Reduction Tax Proposals Using the Experimental Tobacco Marketplace

,

,  and

and

Abstract

:1. Introduction

2. Materials and Methods

2.1. Participants

2.2. Procedure

Experimental Tobacco Marketplace

2.3. Data Analysis

2.3.1. Sample Size Calculation

2.3.2. Participant Characteristics

2.3.3. Outcome Measures

2.3.4. Statistical Analysis

3. Results

3.1. Demographics and Smoking-Related Assessments

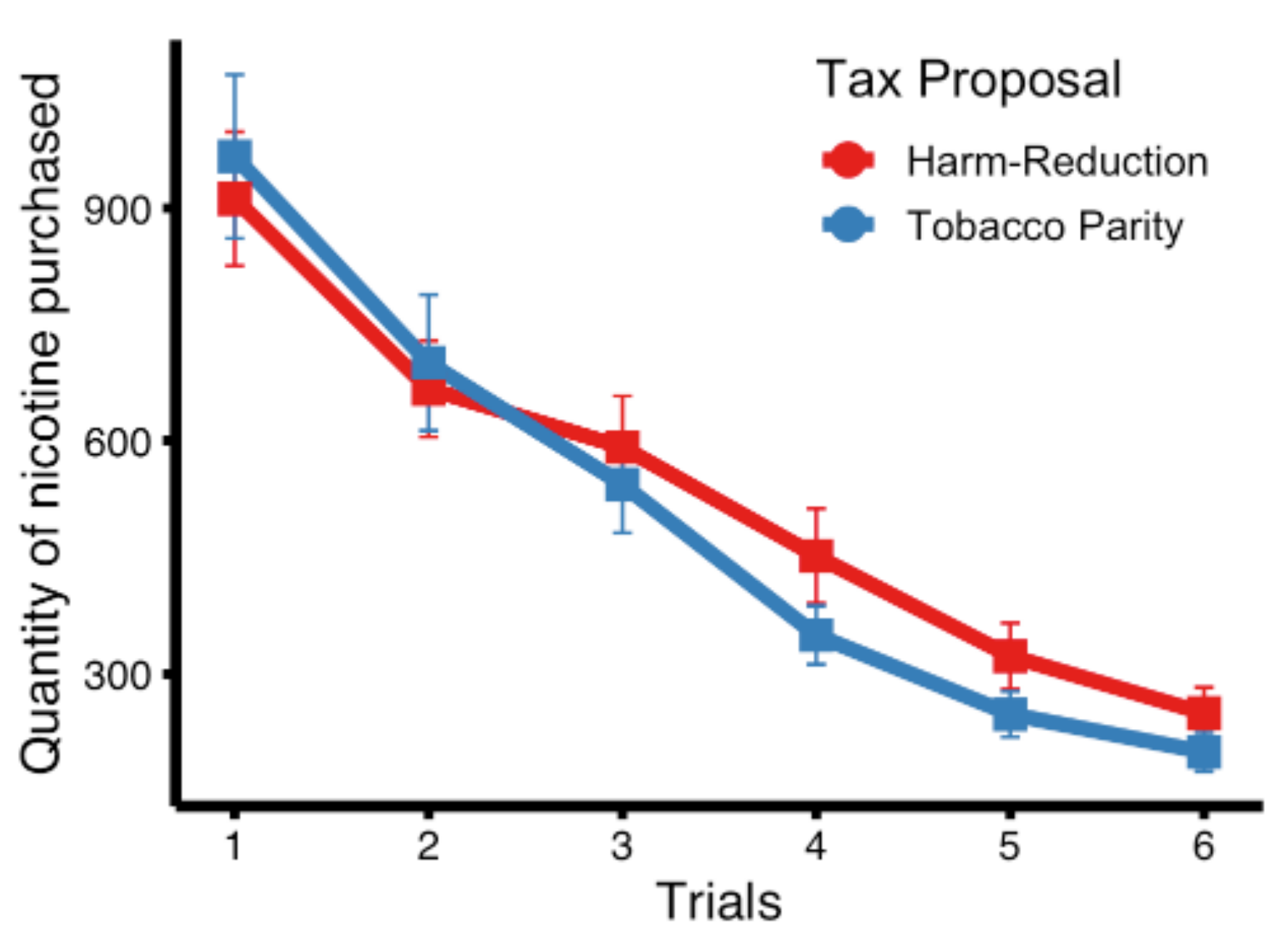

3.2. Total Quantity of Nicotine Purchased

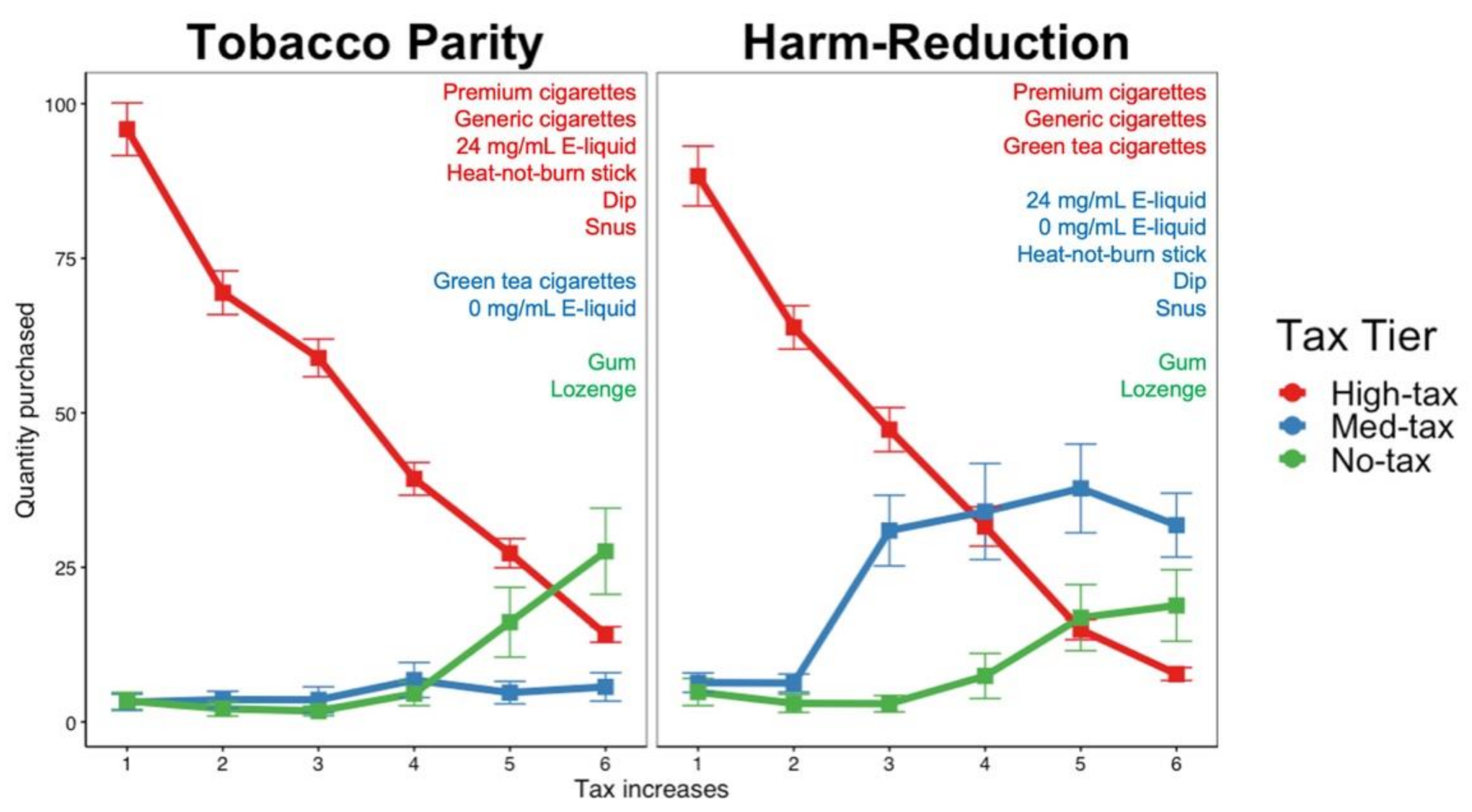

3.3. Tax Proposals

4. Discussion

4.1. Total Nicotine Purchased from Tobacco/NRT Products

4.2. Substitution between Products

4.3. Limitations

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| Brand | n of Users |

|---|---|

| Basic | 1 |

| Camel | 4 |

| Eagle | 1 |

| Marlboro | 18 |

| Natural American Spirit | 1 |

| Pall Mall | 2 |

| USA | 1 |

| Winston | 1 |

| Other | 6 |

Appendix B

| Tier | Tobacco Product | Market Price | MF 1 | MF 2 | MF 3 | MF 4 | MF 5 |

|---|---|---|---|---|---|---|---|

| High tax | Premium cigarette | 47.60 (54.91) | 23.60 (32.86) | 21.06 (38.20) | 11.00 (20.52) | 3.03 (6.20) | 1.71 (3.20) |

| Generic cigarette | 46.86 (72.09) | 44.80 (57.20) | 29.94 (33.11) | 19.37 (19.77) | 12.09 (17.55) | 5.23 (10.26) | |

| E-Liquid 24 mg/mL | 0.26 (0.92) | 0.23 (0.55) | 6.91 (27.55) | 8.09 (34.48) | 11.57 (33.94) | 6.80 (17.65) | |

| Heat-not-burn | 0.46 (1.22) | 0.49 (1.22) | 0.66 (1.86) | 0.54 (1.46) | 0.29 (0.99) | 0.20 (0.58) | |

| Snus | 0.49 (2.06) | 0.17 (0.51) | 0.11 (0.40) | 0.14 (0.43) | 0.11 (0.40) | 0.09 (0.37) | |

| Dip | 0.23 (0.88) | 0.14 (0.43) | 0.20 (0.58) | 0.17 (0.51) | 0.20 (0.76) | 0.11 (0.40) | |

| Medium tax | Green tea Cigarette | 2.26 (10.22) | 3.00 (10.84) | 3.29 (17.72) | 6.00 (23.87) | 3.71 (14.36) | 2.46 (9.83) |

| E-Liquid 0 mg/mL | 0.91 (4.73) | 0.60 (2.72) | 0.29 (0.99) | 0.77 (3.40) | 1.03 (5.24) | 3.20 (16.93) | |

| No tax | Gum/Lozenge | 3.40 (8.09) | 2.14 (7.10) | 1.77 (4.56) | 4.57 (11.48) | 16.11 (33.36) | 27.60 (41.22) |

| Tier | Tobacco Product | Market Price | MF 1 | MF 2 | MF 3 | MF 4 | MF 5 |

|---|---|---|---|---|---|---|---|

| High tax | Premium cigarette | 53.49 (54.68) | 32.89 (40.46) | 19.23 (38.29) | 8.14 (14.54) | 6.34 (14.58) | 1.80 (3.50) |

| Generic cigarette | 34.03 (51.99) | 30.74 (39.38) | 27.80 (30.59) | 23.14 (34.17) | 8.03 (12.97) | 5.80 (11.10) | |

| Green tea Cigarette | 0.80 (3.71) | 0.20 (0.47) | 0.26 (0.56) | 0.31 (0.93) | 0.54 (2.54) | 0.14 (0.55) | |

| Medium tax | E-Liquid 24 mg/mL | 3.51 (17.92) | 4.94 (19.56) | 18.89 (59.35) | 31.46 (104.03) | 35.37 (95.82) | 28.91 (68.58) |

| Heat-not-burn | 0.57 (1.74) | 0.43 (1.04) | 4.29 (15.51) | 2.23 (11.14) | 1.77 (8.27) | 1.86 (6.00) | |

| Snus | 0.20 (0.53) | 0.31 (0.96) | 0.26 (0.89) | 0.14 (0.49) | 0.09 (0.28) | 0.23 (0.73) | |

| Dip | 0.20 (0.53) | 0.17 (0.51) | 0.14 (0.43) | 0.11 (0.40) | 0.11 (0.40) | 0.49 (1.87) | |

| E-Liquid 0 mg/mL | 1.86 (8.50) | 0.43 (1.31) | 7.37 (34.69) | 0.09 (0.28) | 0.43 (2.03) | 0.34 (1.08) | |

| No tax | Gum/Lozenge | 4.83 (12.99) | 3.00 (8.65) | 2.94 (7.84) | 7.43 (21.58) | 16.86 (31.61) | 18.83 (34.23) |

References

- Sung, H.-Y.; Wang, Y.; Yao, T.; Lightwood, J.; Max, W. Polytobacco Use and Nicotine Dependence Symptoms Among US Adults, 2012–2014. Nicotine Tob. Res. 2018, 20, S88–S98. [Google Scholar] [CrossRef]

- National Center for Chronic Disease Prevention. Preventing Tobacco Use among Young People: A Report of the Surgeon General; U.S. Department of Health and Human Services, Public Health Service, Centers for Disease Control and Prevention, National Center for Chronic Disease Prevention and Health Promotion, Office on Smoking and Health: Washington, DC, USA, 1994.

- Mantey, D.S.; Chido-Amajuoyi, O.G.; Omega-Njemnobi, O.; Montgomery, L. Cigarette Smoking Frequency, Quantity, Dependence, and Quit Intentions during Adolescence: Comparison of Menthol and Non-Menthol Smokers (National Youth Tobacco Survey 2017–2020). Addict. Behav. 2021, 121, 106986. [Google Scholar] [CrossRef] [PubMed]

- Yong, H.-H.; Borland, R.; Cummings, K.M.; Gravely, S.; Thrasher, J.F.; McNeill, A.; Hitchman, S.; Greenhalgh, E.; Thompson, M.E.; Fong, G.T. Reasons for Regular Vaping and for Its Discontinuation among Smokers and Recent Ex-Smokers: Findings from the 2016 ITC Four Country Smoking and Vaping Survey. Addiction 2019, 114 (Suppl. S1), 35–48. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Chaloupka, F.J.; Yurekli, A.; Fong, G.T. Tobacco Taxes as a Tobacco Control Strategy. Tob. Control 2012, 21, 172–180. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Chaloupka, F.; Warner, K.E. The economics of smoking. In Handbook of Health Economics; Culyer, A.J., Newhouse, J.P., Eds.; Elsevier: Amsterdam, The Netherlands, 2000; Volume 1, pp. 1539–1627. [Google Scholar]

- Saffer, H.; Dench, D.L.; Grossman, M.; Dave, D.M. E-Cigarettes and Adult Smoking: Evidence from Minnesota; National Bureau of Economic Research: Cambridge, MA, USA, 2019; Volume 60, pp. 207–228. [Google Scholar] [CrossRef]

- Boonn, A. State Excise Tax Rating for Non-Cigarette Tobacco Products; Campaign for Tobacco Free Kids: Washington, DC, USA, 2020. [Google Scholar]

- Apuzzo, M. Tobacco Execs Quickly Find Tax Loophole. Associated Press Writers AP IMPACT. San Diego Union-Tribune. 18 November 2009. Available online: https://www.heraldnet.com/news/tobacco-execs-quickly-find-tax-loophole/ (accessed on 20 July 2021).

- World Health Organization. WHO Technical Manual on Tobacco Tax Administration; WHO: Geneva, Switzerland, 2010. [Google Scholar]

- Campaign for Tobacco Free Kids. Creating Federal Tax Equity among All Tobacco Products Would Increase Federal Revenues & Promote Public Health; Campaign for Tobacco Free Kids: Washington, DC, USA, 2017; Available online: https://www.tobaccofreekids.org/assets/factsheets/0354.pdf (accessed on 20 July 2021).

- CASAA’s Mission. Available online: https://casaa.org/mission/ (accessed on 26 January 2021).

- Boesen, U. Taxing Nicotine Products: A Primer; The Tax Foundation: Washington, DC, USA, 2020; Available online: https://taxfoundation.org/taxing-nicotine-products/ (accessed on 20 July 2021).

- Smith, T.T.; Hatsukami, D.K.; Benowitz, N.L.; Colby, S.M.; McClernon, F.J.; Strasser, A.A.; Tidey, J.W.; White, C.M.; Donny, E.C. Whether to Push or Pull? Nicotine Reduction and Non-Combusted Alternatives—Two Strategies for Reducing Smoking and Improving Public Health. Prev. Med. 2018, 117, 8–14. [Google Scholar] [CrossRef]

- Zeller, M.; Hatsukami, D. Strategic Dialogue on Tobacco Harm Reduction Group the Strategic Dialogue on Tobacco Harm Reduction: A Vision and Blueprint for Action in the US. Tob. Control 2009, 18, 324–332. [Google Scholar] [CrossRef]

- McDaniel, P.A.; Smith, E.A.; Malone, R.E. The Tobacco Endgame: A Qualitative Review and Synthesis. Tob. Control 2016, 25, 594–604. [Google Scholar] [CrossRef]

- Wang, X.; Xu, X.; Tynan, M.A.; Gerzoff, R.B.; Caraballo, R.S.; Promoff, G.R. Tax Avoidance and Evasion: Cigarette Purchases from Indian Reservations Among US Adult Smokers, 2010–2011. Public Health Rep. 2017, 132, 304–308. [Google Scholar] [CrossRef]

- DeCicca, P.; Kenkel, D.; Liu, F. Who Pays Cigarette Taxes? The Impact of Consumer Price Search. Rev. Econ. Stat. 2013, 95, 516–529. [Google Scholar] [CrossRef]

- Licht, A.S.; Hyland, A.J.; O’Connor, R.J.; Chaloupka, F.J.; Borland, R.; Fong, G.T.; Nargis, N.; Cummings, K.M. Socio-Economic Variation in Price Minimizing Behaviors: Findings from the International Tobacco Control (ITC) Four Country Survey. Int. J. Environ. Res. Public Health 2011, 8, 234–252. [Google Scholar] [CrossRef]

- Boonn, A. How to Make State Cigar Tax Rates Fair and Effective; Campaign for Tobacco-Free Kids: Washington, DC, USA, 2020; Available online: https://www.tobaccofreekids.org/assets/factsheets/0335.pdf (accessed on 20 July 2021).

- Government Accountability Office. Illicit Tobacco: Various Schemes Are Used to Evade Taxes and Fees; Government Accountability Office: Washington, DC, USA, 2011.

- Government Accountability Office. Tobacco Taxes: Large Disparities in Rates for Smoking Products Trigger Significant Market Shifts to Avoid Higher Taxes; Government Accountability Office: Washington, DC, USA, 2012.

- Choi, K.; Hennrikus, D.; Forster, J.; St Claire, A.W. Use of Price-Minimizing Strategies by Smokers and Their Effects on Subsequent Smoking Behaviors. Nicotine Tob. Res. 2012, 14, 864–870. [Google Scholar] [CrossRef]

- Boonn, A. The Problem with Roll-Your-Own (RYO) and Other Smoking Tobacco; Campaign for Tobacco Free Kids: Washington, DC, USA, 2020; Available online: https://www.tobaccofreekids.org/assets/factsheets/0336.pdf (accessed on 20 July 2021).

- Keith, R.J.; Fetterman, J.L.; Orimoloye, O.A.; Dardari, Z.; Lorkiewicz, P.K.; Hamburg, N.M.; DeFilippis, A.P.; Blaha, M.J.; Bhatnagar, A. Characterization of Volatile Organic Compound Metabolites in Cigarette Smokers, Electronic Nicotine Device Users, Dual Users, and Nonusers of Tobacco. Nicotine Tob. Res. 2020, 22, 264–272. [Google Scholar] [CrossRef]

- National Academies of Sciences, Engineering and Medicine. Public Health Consequences of E-Cigarettes; Stratton, K., Kwan, L.Y., Eaton, D.L., Eds.; The National Academies Press: Washington, DC, USA, 2018; ISBN 9780309468343. [Google Scholar]

- Shahab, L.; Goniewicz, M.L.; Blount, B.C.; Brown, J.; McNeill, A.; Alwis, K.U.; Feng, J.; Wang, L.; West, R. Nicotine, Carcinogen, and Toxin Exposure in Long-Term E-Cigarette and Nicotine Replacement Therapy Users: A Cross-Sectional Study. Ann. Intern. Med. 2017, 166, 390–400. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Stepanov, I.; Jensen, J.; Hatsukami, D.; Hecht, S.S. New and Traditional Smokeless Tobacco: Comparison of Toxicant and Carcinogen Levels. Nicotine Tob. Res. 2008, 10, 1773–1782. [Google Scholar] [CrossRef]

- Xia, B.; Blount, B.C.; Guillot, T.; Brosius, C.; Li, Y.; Van Bemmel, D.M.; Kimmel, H.L.; Chang, C.M.; Borek, N.; Edwards, K.C.; et al. Tobacco-Specific Nitrosamines (NNAL, NNN, NAT, and NAB) Exposures in the US Population Assessment of Tobacco and Health (PATH) Study Wave 1 (2013–2014). Nicotine Tob. Res. 2020. [Google Scholar] [CrossRef] [PubMed]

- Holman, M.R. FDA Regulating Tobacco Products along a Continuum of Risk. In Proceedings of the Tobacco Science Research Conference, Leesburg, VA, USA, 15–18 September 2019. [Google Scholar]

- Office of the Commissioner FDA. Announces Comprehensive Regulatory Plan to Shift Trajectory of Tobacco-Related Disease, Death. Available online: https://www.fda.gov/news-events/press-announcements/fda-announces-comprehensive-regulatory-plan-shift-trajectory-tobacco-related-disease-death (accessed on 3 February 2021).

- Nutt, D.J.; Phillips, L.D.; Balfour, D.; Curran, H.V.; Dockrell, M.; Foulds, J.; Fagerstrom, K.; Letlape, K.; Milton, A.; Polosa, R.; et al. Estimating the Harms of Nicotine-Containing Products Using the MCDA Approach. Eur. Addict. Res. 2014, 20, 218–225. [Google Scholar] [CrossRef] [PubMed]

- Tomar, S.L.; Alpert, H.R.; Connolly, G.N. Patterns of Dual Use of Cigarettes and Smokeless Tobacco among US Males: Findings from National Surveys. Tob. Control 2010, 19, 104–109. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Cirino, P.T.; Chin, C.E.; Sevcik, R.A.; Wolf, M.; Lovett, M.; Morris, R.D. Measuring Socioeconomic Status: Reliability and Preliminary Validity for Different Approaches. Assessment 2002, 9, 145–155. [Google Scholar] [CrossRef] [PubMed]

- Siahpush, M.; Yong, H.-H.; Borland, R.; Reid, J.L.; Hammond, D. Smokers with Financial Stress Are More Likely to Want to Quit but Less Likely to Try or Succeed: Findings from the International Tobacco Control (ITC) Four Country Survey. Addiction 2009, 104, 1382–1390. [Google Scholar] [CrossRef] [Green Version]

- Siahpush, M.; Farazi, P.A.; Maloney, S.I.; Dinkel, D.; Nguyen, M.N.; Singh, G.K. Socioeconomic Status and Cigarette Expenditure among US Households: Results from 2010 to 2015 Consumer Expenditure Survey. BMJ Open 2018, 8, e020571. [Google Scholar] [CrossRef] [Green Version]

- Bickel, W.K.; Pope, D.A.; Kaplan, B.A.; DeHart, W.B.; Koffarnus, M.N.; Stein, J.S. Electronic Cigarette Substitution in the Experimental Tobacco Marketplace: A Review. Prev. Med. 2018, 117, 98–106. [Google Scholar] [CrossRef]

- Quisenberry, A.J.; Koffarnus, M.N.; Hatz, L.E.; Epstein, L.H.; Bickel, W.K. The Experimental Tobacco Marketplace I: Substitutability as a Function of the Price of Conventional Cigarettes. Nicotine Tob. Res. 2016, 18, 1642–1648. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Quisenberry, A.; Koffarnus, M.N.; Bianco, A.; Perry, E.; Bickel, W.K. The Experimental Tobacco Marketplace II: Substitutability in Dual E-Cigarette and Cigarette Users. Drug Alcohol Depend. 2017, 171, e171. [Google Scholar] [CrossRef]

- Pope, D.A.; Poe, L.; Stein, J.S.; Kaplan, B.A.; Heckman, B.W.; Epstein, L.H.; Bickel, W.K. Experimental Tobacco Marketplace: Substitutability of E-Cigarette Liquid for Cigarettes as a Function of Nicotine Strength. Tob. Control 2019, 28, 206–211. [Google Scholar] [CrossRef] [PubMed]

- Kaplan, B.A.; Pope, D.A.; Dehart, W.B. Estimating Uptake for Reduced-Nicotine Cigarettes Using Behavioral Economics. Tob. Regul. Sci. 2019, 5, 264–279. [Google Scholar] [CrossRef]

- Pope, D.A.; Poe, L.; Stein, J.S.; Kaplan, B.A.; DeHart, W.B.; Mellis, A.M.; Heckman, B.W.; Epstein, L.H.; Chaloupka, F.J.; Bickel, W.K. The Experimental Tobacco Marketplace: Demand and Substitutability as a Function of Cigarette Taxes and E-Liquid Subsidies. Nicotine Tob. Res. 2019, 22, 782–790. [Google Scholar] [CrossRef]

- Strickland, J.C.; Stoops, W.W. The Use of Crowdsourcing in Addiction Science Research: Amazon Mechanical Turk. Exp. Clin. Psychopharmacol. 2019, 27, 1–18. [Google Scholar] [CrossRef]

- Craft, W.H.; Tegge, A.N.; Bickel, W.K. Episodic Future Thinking Reduces Chronic Pain Severity: A Proof of Concept Study. Drug Alcohol Depend. 2020, 215, 108250. [Google Scholar] [CrossRef] [PubMed]

- Athamneh, L.N.; Stein, M.D.; Lin, E.H.; Stein, J.S.; Mellis, A.M.; Gatchalian, K.M.; Epstein, L.H.; Bickel, W.K. Setting a Goal Could Help You Control: Comparing the Effect of Health Goal versus General Episodic Future Thinking on Health Behaviors among Cigarette Smokers and Obese Individuals. Exp. Clin. Psychopharmacol. 2020, 29, 59–72. [Google Scholar] [CrossRef] [PubMed]

- Stein, J.S.; Tegge, A.N.; Turner, J.K.; Bickel, W.K. Episodic Future Thinking Reduces Delay Discounting and Cigarette Demand: An Investigation of the Good-Subject Effect. J. Behav. Med. 2018, 41, 269–276. [Google Scholar] [CrossRef] [PubMed]

- Sze, Y.Y.; Stein, J.S.; Bickel, W.K.; Paluch, R.A.; Epstein, L.H. Bleak Present, Bright Future: Online Episodic Future Thinking, Scarcity, Delay Discounting, and Food Demand. Clin. Psychol. Sci. 2017, 5, 683–697. [Google Scholar] [CrossRef]

- Qualtrics. Qualtrics Survey Software; Qualtrics: Provo, UT, USA, 2021. [Google Scholar]

- Fagerstrom, K. Determinants of Tobacco Use and Renaming the FTND to the Fagerstrom Test for Cigarette Dependence. Nicotine Tob. Res. 2012, 14, 75–78. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Cox, L.S.; Tiffany, S.T.; Christen, A.G. Evaluation of the Brief Questionnaire of Smoking Urges (QSU-Brief) in Laboratory and Clinical Settings. Nicotine Tob. Res. 2001, 3, 7–16. [Google Scholar] [CrossRef] [PubMed]

- Mooney, M.E.; Leventhal, A.M.; Hatsukami, D.K. Attitudes and Knowledge about Nicotine and Nicotine Replacement Therapy. Nicotine Tob. Res. 2006, 8, 435–446. [Google Scholar] [CrossRef] [PubMed]

- Koffarnus, M.N.; Wilson, A.G.; Bickel, W.K. Effects of Experimental Income on Demand for Potentially Real Cigarettes. Nicotine Tob. Res. 2015, 17, 292–298. [Google Scholar] [CrossRef] [Green Version]

- DeHart, W.B.; Kaplan, B.A.; Pope, D.A.; Mellis, A.M.; Bickel, W.K. The Experimental Tobacco Marketplace: Narrative Influence on Electronic Cigarette Substitution. Exp. Clin. Psychopharmacol. 2019, 27, 115–124. [Google Scholar] [CrossRef] [PubMed]

- DeHart, W.B.; Mellis, A.M.; Kaplan, B.A.; Pope, D.A.; Bickel, W.K. The Experimental Tobacco Marketplace: Narratives Engage Cognitive Biases to Increase Electronic Cigarette Substitution. Drug Alcohol Depend. 2019, 197, 203–211. [Google Scholar] [CrossRef]

- Kaplan, B.A.; Koffarnus, M.N.; Franck, C.T.; Bickel, W.K. Effects of Reduced-Nicotine Cigarettes Across Regulatory Environments in the Experimental Tobacco Marketplace: A Randomized Trial. Nicotine Tob. Res. 2020, 23, 1123–1132. [Google Scholar] [CrossRef] [PubMed]

- Freitas-Lemos, R.; Stein, J.S.; Pope, D.A.; Brown, J.; Feinstein, M.; Stamborski, K.M.; Tegge, A.N.; Heckman, B.W.; Bickel, W.K. E-Liquid Purchase as a Function of Workplace Restriction in the Experimental Tobacco Marketplace. Exp. Clin. Psychopharmacol. 2021. [Google Scholar] [CrossRef]

- Retail Analytics. Available online: https://www.nielsen.com/apac/en/solutions/measurement/retail-analytics/ (accessed on 31 May 2021).

- Benjamini, Y.; Hochberg, Y. Controlling the False Discovery Rate: A Practical and Powerful Approach to Multiple Testing. J. R. Stat. Soc. Ser. B (Methodol.) 1995, 57, 289–300. [Google Scholar] [CrossRef]

- R Core Team. R: A Language and Environment for Statistical Computing; R Foundation for Statistical Computing: Vienna, Austria, 2018. [Google Scholar]

- Quisenberry, A.J.; Koffarnus, M.N.; Epstein, L.H.; Bickel, W.K. The Experimental Tobacco Marketplace II: Substitutability and Sex Effects in Dual Electronic Cigarette and Conventional Cigarette Users. Drug Alcohol Depend. 2017, 178, 551–555. [Google Scholar] [CrossRef] [Green Version]

- Freitas-Lemos, R.; Stein, J.S.; Tegge, A.N.; Kaplan, B.A.; Heckman, B.W.; Cummings, K.M.; Bickel, W.K. The Illegal Experimental Tobacco Marketplace I: Effects of VapingProduct Bans. Nicotine Tob. Res. 2021. [Google Scholar] [CrossRef] [PubMed]

- Wilson, A.G.; Franck, C.T.; Koffarnus, M.N.; Bickel, W.K. Behavioral Economics of Cigarette Purchase Tasks: Within-Subject Comparison of Real, Potentially Real, and Hypothetical Cigarettes. Nicotine Tob. Res. 2016, 18, 524–530. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Heckman, B.W.; Cummings, K.M.; Hirsch, A.A.; Quisenberry, A.J.; Borland, R.; O’Connor, R.J.; Fong, G.T.; Bickel, W.K. A Novel Method for Evaluating the Acceptability of Substitutes for Cigarettes: The Experimental Tobacco Marketplace. Tob. Regul. Sci. 2017, 3, 266–279. [Google Scholar] [CrossRef] [PubMed]

| n | 35 | |

|---|---|---|

| Demographics | Age (mean (SD)) | 44.06 (13.36) |

| Gender = male (n (%)) | 17 (48.6) | |

| Race (n (%)) | ||

| White | 33 (91.4) | |

| Black or African American | 1 (2.9) | |

| Asian | 1 (2.9) | |

| Ethnicity = NOT Hispanic or Latino (n (%)) | 32 (91.4) | |

| Education (n (%)) | ||

| High school (12 years) | 4 (11.4) | |

| Some college (13–15 years) | 15 (42.9) | |

| College (16 years) | 11 (31.4) | |

| Graduate school (18 years) | 5 (14.3) | |

| Tobacco-related measures | Age of initiation (mean (SD)) | 17.57 (6.32) |

| Cigarettes per day (mean (SD)) | 17.06 (8.98) | |

| FTCD (mean (SD)) | 5.60 (1.94) | |

| QSU cigarettes (mean (SD)) | 43.91 (16.63) | |

| PHR cigarettes (mean (SD)) | 70.23 (20.25) | |

| Willingness to try OTPs (%) | 30 (85.71) |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Freitas-Lemos, R.; Keith, D.R.; Tegge, A.N.; Stein, J.S.; Cummings, K.M.; Bickel, W.K. Estimating the Impact of Tobacco Parity and Harm Reduction Tax Proposals Using the Experimental Tobacco Marketplace. Int. J. Environ. Res. Public Health 2021, 18, 7835. https://doi.org/10.3390/ijerph18157835

Freitas-Lemos R, Keith DR, Tegge AN, Stein JS, Cummings KM, Bickel WK. Estimating the Impact of Tobacco Parity and Harm Reduction Tax Proposals Using the Experimental Tobacco Marketplace. International Journal of Environmental Research and Public Health. 2021; 18(15):7835. https://doi.org/10.3390/ijerph18157835

Chicago/Turabian StyleFreitas-Lemos, Roberta, Diana R. Keith, Allison N. Tegge, Jeffrey S. Stein, K. Michael Cummings, and Warren K. Bickel. 2021. "Estimating the Impact of Tobacco Parity and Harm Reduction Tax Proposals Using the Experimental Tobacco Marketplace" International Journal of Environmental Research and Public Health 18, no. 15: 7835. https://doi.org/10.3390/ijerph18157835