1. Introduction

Haze pollution is a serious problem in China. For example, in 12–17 January 2018, Beijing and its surrounding areas suffered from severe regional heavy haze pollution, where the highest concentrations of PM

2.5 reached over 900 μg/m

3 [

1]. Numerous studies in China have revealed that there is mutual influence between industry development (mostly in the form of economic growth) and haze pollution; however, particular relationships between different industry sectors and haze pollution differs. The classification of different industry sectors is defined by the National Bureau of Statistics of China, which divides industry into primary, secondary, and tertiary industry according to their economic activities [

2]. The primary industry refers to agriculture, forestry, animal husbandry, and fishery (excluding relevant services, which belongs to the tertiary industry). The secondary industry refers to the mining industry (excluding mining assistance services), manufacturing (excluding metal-related production services, machinery, and equipment repair services, etc.), energy production and supply (e.g., electricity, heat, gas, and water), and architecture, engineering, and construction. The tertiary industry refers to those that are not classified into the primary and secondary industry, such as transportation, information, finance, commerce, catering, education, public services, and other non-material production sectors [

3].

Stubble burning in the primary industry can release a lot of persistent pollutants in the air [

4] and, therefore, cause air pollution with a certain circulation background and ground meteorological characteristics [

5]. Air pollution caused by stubble burning has significant characteristics of explosiveness, heavy pollution, short durations, and increased particulate matter concentration [

6]. According to stubble burning data from 31 provinces in China during 1997 to 2013, 1.036 million tons of PM

2.5 have been released per year due to stubble burning [

7]. Zhao et al. [

8] also suggested that agricultural activities were an important source of haze-pollutant emissions. Meanwhile, haze pollution is taken as one of the major disasters that constitute agricultural production [

9]. China’s grain output was reduced by about 3 billion kilograms annually as a result of atmospheric pollution [

10]. Dust that covers the surface of leaves would shield 60% of light intensity, resulting in about a 20% reduction in photosynthetic product [

11], and eventually lead to yield loss [

12,

13]. Trace-metals such as lead and mercury in haze can damage cell membranes [

14], inhibit mineral absorption [

15,

16], and inhibit photosynthesis and transpiration as well [

17]. Zeng et al. [

18] adopted a market value method to estimate agricultural economic losses related to atmospheric pollution in Xi’an in 2013, which was up to 1.985 billion yuan.

In the secondary industry, industrial emissions and construction dust are the main sources of haze pollution. Power trade and metallurgical trade are the two major pollutant emissions from industrial sources in Beijing [

19]. An increase in the proportion of industry in social economy would lead to severe haze pollution [

20,

21,

22]. A case study conducted in Beijing showed that construction dust contributed 31.3 μg/m

3 and 9.6 μg/m

3 to concentrations of PM

10 and PM

2.5, respectively [

23]. Another study conducted in Langfang City, Hebei Province, China, concluded that annual emissions of PM

2.5 and PM

10 caused by construction dust reached 7546 tons and 19,968 tons in 2014, respectively [

24]. In terms of the significance of haze pollution, it can promote the transformation of industrial production methods [

25], improve energy efficiency [

26], and optimize industry structure [

27]. Haze can also reduce the flashover performance of insulators and thereby easily lead to pollution flashover [

28,

29]. Moreover, reduced visibility caused by haze pollution may threaten the safety of construction, the efficiency of construction operations, and increase the cost of construction [

30,

31,

32,

33,

34].

In the tertiary industry, transportation is an important contributor to haze pollution [

35,

36]. Exhaust emissions of motor vehicles are the direct cause of outdoor PM

2.5 and PM

10 [

37,

38,

39,

40]. Although haze pollution would, to a certain extent, stimulate the output of health services [

41], it is far less than the damage it causes. In the tertiary industry, transportation and tourism are the most vulnerable sectors [

42] because of reduced visibility and potential health damage [

43,

44]. In January 2013, direct economic losses in the national transportation industry of China were approximately 76.6 million USD because of the haze pollution [

45]. Inbound tourists’ perceptions of China’s environment were generally low because of haze weather [

46]. Most importantly, haze pollution has a negative impact on both tourism resources and its transportation [

47].

Most of the existing research outcomes focus on the mechanism of haze influences, but rarely do they study the dynamic characteristics between haze pollution and particular industry sectors. Several scholars have tried to study the relationship between environmental pollution and economic development through vector autoregression (VAR) models, panel data models, or other methods [

48,

49,

50,

51,

52]. However, most of these studies failed to consider industry refinement, and they used per capita gross domestic product (GDP) only as an indicator of economic progress. How to properly investigate, describe, and sculpt the relationship between industry development and haze (PM

2.5) pollution is a challenging question; therefore, this becomes the main research purpose in this paper. Precisely, by studying the relationship between haze pollution and various industry sectors, a further dynamic interrelation is explored in this paper. Based on Beijing’s PM

2.5 concentration and the gross outputs from the three major sectors of industry from the first quarter of 2010 to the second quarter of 2017, a VAR model has been established in this paper. By utilizing the impulse response function and variance decomposition, the dynamic interconnection between the PM

2.5 pollution levels and the development of the three main industry sectors has been analyzed. This study can offer a new perspective for studying the relationship between haze pollution and economic development, and it can provide new ideas for haze pollution management as well.

2. Materials and Methods

2.1. A Vector Autoregression (VAR) Model

Sims [

53] introduced a popular VAR model to econometrics in 1980, and the VAR model has been widely used since then [

54,

55]. In the VAR model, endogenous variables were used to regress the lag value of each variable in the system for studying the dynamic relationship between these system variables and the endogenous variables. The

p-order VAR model is denoted as VAR (

p), which is generally given in (1).

where

is the sample size.

is a

dimensional endogenous variable vector.

is a

dimensional endogenous variable vector.

are the unknown

parametric matrices.

is a

dimensional estimated coefficient matrix.

is a

dimensional random error vector (i.e., a white noise process). It satisfies:

where

; and

.

is a

-th order identity matrix.

Determining the optimal lag order is especially important for establishing the VAR model. Increasing the lag order appropriately can increase the autocorrelation in the error term, but it also easily affects the degree of freedom of the model. Therefore, a comprehensive method was proposed to determine the lag order of the model, based on the likelihood ratio (LR) test statistic, final prediction error (FPE), Akaike information criterion (AIC), Schwarz information criterion (SC), and Hannan-Quinn (HQ) information criterion.

2.2. Checking the Model

2.2.1. Stability Test

The stability is characterized by the variation in the values of the parameters in a given model.

When

, the characteristic equation of the VAR model shown in (1) is shown in (3).

For the VAR model, an equivalent condition for the stability can be defined because the solutions of Equation (3) are within the unit circle.

When

, the following equation can be established:

Combining Equations (3) and (4) can lead to (5).

Equation (5) can be written as a VAR model of a one-order partitioned matrix, as shown in (7):

where the characteristic equation is shown in (8).

For the VAR model, an equivalent condition for the stability was that the solutions of Equation (8) were within the unit circle.

2.2.2. Cointegration Test

The cointegration relationship expresses the long-term dynamic equilibrium relationship between the multiple economic variables interacting with each other and their evolution [

56]. Typical cointegration test methods mainly include the Engle-Granger (E-G) two-step method and the Johansen–Juselius (JJ) test method [

57,

58]. Compared with the EG method, the JJ method cannot only test the multi-cointegration relationship, but also impose constraints on the cointegration relationship, which was therefore employed in this paper.

Assume that the series is an order integration. If there exists a dimension vector , such that is an order integration, i.e., , then is an order cointegration and is a cointegration vector.

For instance, when

, the series

is integrated of order one. After the differential transform, Equation (1) can be rewritten as (9).

where

and

. Since

is a vector of order zero, whether a cointegration relationship exists or not depends on the rank of

, as explained below.

Denote the rank of

by

. When

,

is a null matrix, so there is no cointegration relationship between variables. When

,

is a full rank matrix, then

is a stationary series, which contradicts with hypotheses. When

, there exist

cointegration relationships. The matrix

can be written as in (10).

where both the ranks of

and

are

. By inserting Equation (10) into Equation (9), it yields:

where

refers to the vector of cointegration relationship.

refers to a matrix of cointegration vectors.

The number of eigenvalues of

is usually judged from the trace test and the max-eigenvalue test. The eigenvalues of

are

, where

. The null hypothesis was that there existed

cointegration relationships at most; the alternative hypothesis was that there existed

cointegration relationships at least. The statistics of the trace test and max-eigenvalue test are shown in (12) and (13), respectively.

At significance level , the values of statistics and were compared with the corresponding critical values from . The null hypothesis was accepted if the values of statistics were smaller than the critical values, which meant that there existed cointegration relationships at most. Otherwise, the null hypothesis was rejected, which meant that there existed cointegration relationships at least. The order was increased in turn until the null hypothesis was accepted.

2.2.3. Granger Causality Test

For economic variables, some were highly correlated, but this did not necessarily mean there was a causal relationship between them. The causal relationship was defined as follows [

59]: if

is the cause of the change in

, then when regressing

on its past values, additional past values of

will remarkably improve the explanatory power of the regression.

Given a

-dimensional VAR(

p) model, as shown in (14):

the variable

was not the Granger cause of the variable

if and only if

,

, and it holds that

.

Therefore, the null hypothesis of the test was

; the alternative hypothesis was that there at least existed a

, such that

. The statistic is written as (15).

where

is the residual square sum of

in Equation (14).

is the residual square sum of

without the lagged variable

.

is the sample number, and

is the lag order.

At significance level , the value of S was compared with the critical value. When S was smaller than the critical value, the null hypothesis was accepted, which meant that the variable was not the Granger cause of ; otherwise, the null hypothesis was rejected (i.e., the variable was the Granger cause of variable .)

2.3. Stationary Sequences

In a stationary sequence the statistical law does not change over time. For a time series generated from a random process, , if the sequence is stationary, the following conditions must be satisfied:

(1) , ;

(2) , ;

(3) , , where is only related to .

In practical applications, the economic and financial sequences encountered are often non-stationary time series. If they are forced to return, they may lead to “false return” problems. Therefore, stationary data needs to be tested before modeling. Stationary sequences were examined by the augmented Dickey–Fuller (ADF) test method.

An ADF test is used to control a higher order correlation by adding the lag difference term of

on the right side of the regression equation. Consider the following three models:

where

is a constant term.

is a linear trend function.

is a random error term.

is the lag order, which is usually determined by AIC.

Subtract

from both ends of Equations (16)–(18),

where

,

.

Model (20) contained intercept items without time trend items, while Model (21) contained both intercept and time trend terms. In practical applications, Model (21) was usually established to test the significance of intercept and trend terms. If they were significant, then they can be retained; otherwise, they should be rejected, and the model can be simplified to the form of (19) or (20).

The null hypothesis of this test was

; that is, there existed a unit root in the sequence. The alternative hypothesis was

; that is, there existed no unit root. The test statistic is shown in (22).

where

is the estimate of

is the standard deviation of

.

At significance level , if the null hypothesis was not rejected, there was a unit root in the sequence; otherwise, this sequence was stationary.

2.4. Impulse Response Function

An impulse response function was employed to study the dynamic effects of disturbance items on the current and future of endogenous variables. It was also employed to analyze the influential relationships between variables, since exogenous variables were not affected by system shocks [

60]. Consider the VAR(

p) model in (1) without exogenous variables, as shown in (23):

where

is the sample size.

is a

dimensional endogenous variable vector.

are

estimated coefficient matrices.

is

dimensional random error vector.

Equation (23) can be rewritten as an infinite-order vector moving average model, as in (24).

where

is a casual operator.

satisfies:

, .

Equation (24) can be transformed into:

According to Equation (25), the following holds:

Then the element of the

th row and the

th column of

can be denoted as below:

where

is an element of matrix

. This indicated that on the condition that other error terms remain unchanged, it would have an impact on endogenous variable

at time

when

received a shock at time

t.

However, the covariance matrix was not necessarily a diagonal matrix; that is, the elements in the random error term changed with a certain element, which contradicted with the assumption of the impulse response function. Therefore, by introducing a transformation matrix, the covariance matrix can be converted into a diagonal matrix, so as to achieve the goal of orthogonalizing the error term.

2.5. Variance Decomposition

Variance decomposition was used to analyze the contribution of each endogenous variable to the variance decomposition, so as to reveal the relationship between the variables in the system. According to Equation (25), it holds that:

Assume that the covariance matrix

of

is a diagonal matrix. By applying

, the variance of

can be obtained as:

where

are the elements of the covariance matrix

.

In this way, the variance of

is decomposed into

unrelated effects. Then the relative variance contribution rate is defined as in (30).

The relative variance contribution rate describes the contribution of the disturbance term to variables. The larger is, the greater the influence of the disturbance on the variable.

4. Discussion

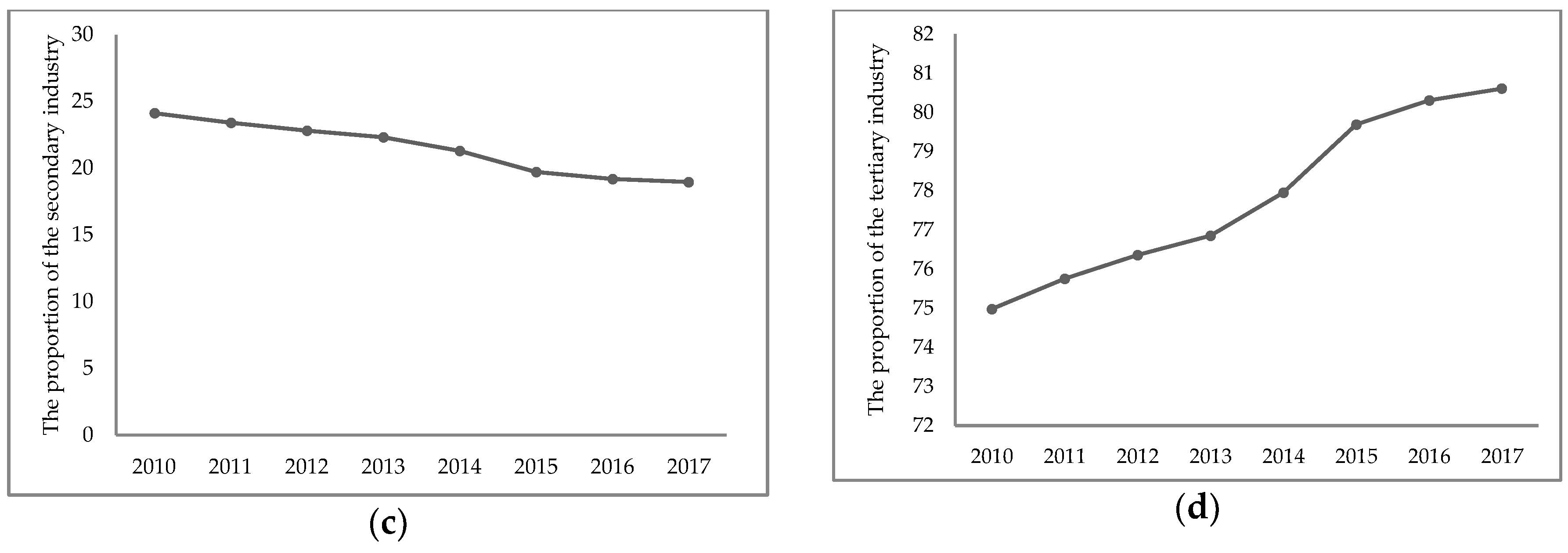

The impulse response function indicated that economic growth of the primary and secondary industries can raise PM

2.5 emissions, whilst the tertiary industry had an inhibitory effect. This result is consistent with the findings of Cao [

67] and Zhao [

68]. Therefore, it can be found that industry improvement (defined as economic growth) is an important factor affecting the intensity and direction of PM

2.5 emissions. More efforts should be undertaken to implement innovation-driven development strategies, promote industry transformation and upgrade, vigorously develop the tertiary industry, and actively cultivate high-end service industries in order to mitigate PM

2.5 pollution.

In addition, PM2.5 pollution itself can hinder the development of the primary and secondary industries. In the long run, it can promote the development of the tertiary industry, which reveals that PM2.5 pollution can influence industry growth as well. With the intensification of pollution and the enhancement of environmental awareness, the advancement of tertiary industry would become one of the most effective ways to alleviate PM2.5 pollution.

Liu et al. [

48], Duan et al. [

52], and Li et al. [

69] all observed that indicators of economic growth had good predictions of environmental pollution, while indicators of environmental pollution had less ability to interpret the variance of economic growth. Results indicated by variance decomposition is supported by their studies, which shows that the industry development of Beijing leans over the cost of PM

2.5 pollution. Capital and labor input are important driving forces for the improvement of Beijing’s industries, whereas the impact of PM

2.5 pollution is relatively small. Environmental quality preference will also restrict the adverse effects of PM

2.5 pollution on industry growth. Therefore, while the industry is developing rapidly, it is necessary to pay attention to alleviating the negative effects of environmental pollution.

Nonetheless, results in this paper were based on statistical characteristics of the data, which were limited by the characteristics of the VAR model, and were not closely integrated with related economic theories. Additionally, several impact factors of industry development and PM2.5 pollution, such as policy environment and environmental quality preference, are not considered in this paper. Therefore, the explanation of impact mechanisms in this paper can be further investigated with in-depth data mining. Overall, conclusions drawn in this paper emphasized the economic losses caused by PM2.5 as well as the interaction of PM2.5 with industry development, which cannot be overlooked.

5. Conclusions

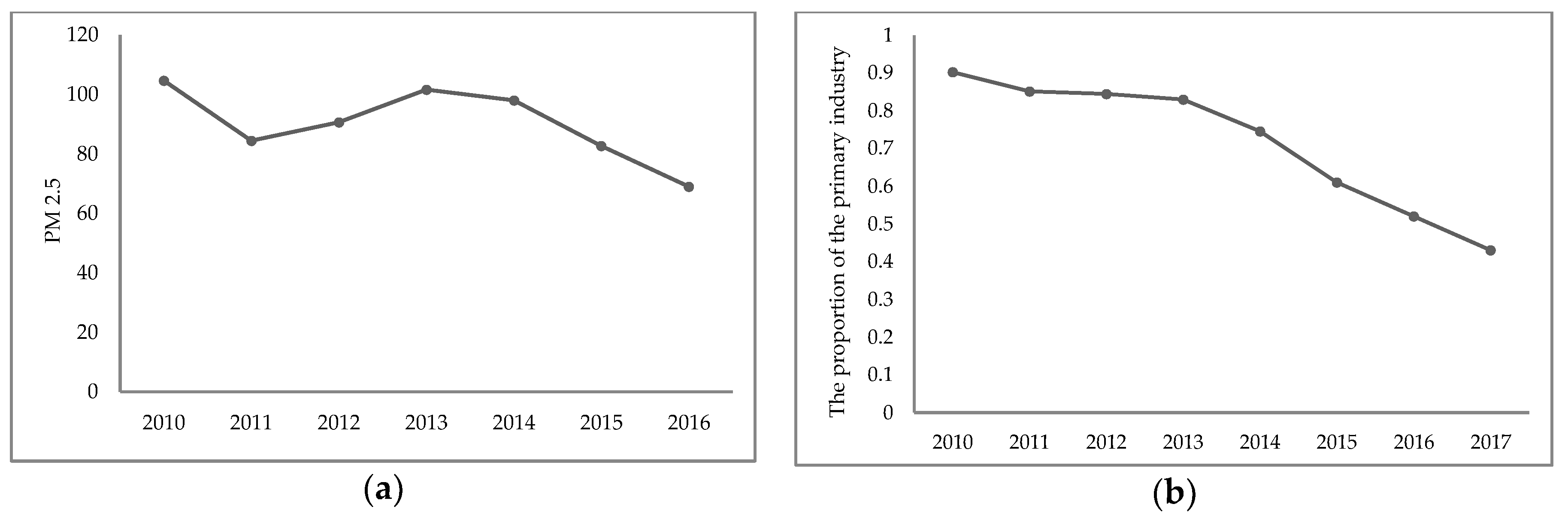

From the perspective of industry development, a VAR model has been proposed in this paper to examine the dynamic relation between the level of haze pollution and industry progress in 2010–2017 through an impulse response function and a variance decomposition method. Results have shown that a long-term equilibrium relationship existed between PM2.5 pollution and the improvement of the primary, secondary, and tertiary industries.

The three industries are the one-way Granger causes of PM2.5. The development of the three industries have shown different degrees of impact on the PM2.5 pollution, with the duration of about one to two years. The development of the primary and secondary industries would increase PM2.5 emission, whilst the tertiary industry would reduce.

The research work in this paper focuses on analyzing the two-way mechanism between PM2.5 pollution and the three industries from the perspective of time dynamics, so as to provide theoretical support for Beijing’s industry development and environmental planning. The foundation of haze management is to adjust industrial development to promote industry transformation and upgrade. Emergency measures, such as suspending the production of heavy polluting enterprises and restricting motor vehicle operation in the city, can only alleviate heavy pollution in the short-term. The long-term solution to the problem of haze requires transforming the extensive economic development model, optimizing the industry structure, vigorously developing the tertiary industry, and forcing the transformation and upgrade enterprises so as to achieve coordinated economic and environmental development.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}