Digitalization in the Renewable Energy Sector—New Market Players

Institute of Markets and Competition, SGH Warsaw School of Economics, al. Niepodległości 162, 02-554 Warsaw, Poland

*

Author to whom correspondence should be addressed.

Energies 2022, 15(13), 4714; https://doi.org/10.3390/en15134714

Submission received: 28 April 2022

/

Revised: 15 June 2022

/

Accepted: 23 June 2022

/

Published: 27 June 2022

(This article belongs to the Special Issue Energy and Business: New and Disruptive Business Models, Blockchain Experiments and Regulation)

Abstract

:Under the conditions of climate change and energy crisis stemming from the COVID-19 pandemic and the embargo on the supply of raw materials from Russia, high hopes are attached to the development of renewable energy in terms of meeting energy needs. Still, renewable energy has some drawbacks too. In the most dynamically growing solar and wind energy industries, the main problems that are indicated include this energy storage and ensuring the security of supplies. These are supposed to be solved by the digital transformation of renewable power generation plus the entry of market players that implement digital business models in renewable energy. The purpose of the article is to identify a framework “digital compass” of business models in renewable energy within a group of solar and wind energy start-ups, operating in energy storage and supply industries. At the base of this study there were: digital technologies, customer orientation, delivery of value and revenue stream. The research algorithm applied here enabled the identification and classification of startup business models based on secondary data using R software. The results show that the identified startups implement digital business models to a minor extent. Startups dealing with solar energy storage stand out in a quite positive manner. The low digital attractiveness of investing in wind energy storage and supply (which, to a smaller extent applies to solar energy), is also indicated the investment preferences of big-tech. Thus, the future of the digital transformation of these industries should be related to regulatory changes rather than technological ones.

1. Introduction

In the third decade of the 21st century, a new energy economy (NEE) is emerging, where the key role is supposed to be played by digital technologies [1,2]. These technologies create new possibilities to collect, manage, and analyse large amounts of data more efficiently [3], which in turn enables a certain energy shift from the traditional industry to digital business. Particularly big challenges are posed in this respect for renewable energy. In the environment of climate change [4,5] and the energy crisis of today, this aspect is becoming even more valid. The slowdown in the replenishment of fossil fuel reserves, which have not been completely replaced by unstable energy sources, is considered as the very source of this crisis. A new momentum to accelerate the digitalisation of renewable energy is created by the economic sanctions imposed on Russia as a consequence of its attack on Ukraine. The blockade on the import of raw energy materials from Russia translates into the increasing public interest and operations of companies that invest in renewable energy [6,7]. It is estimated that in Germany the increase of solar and wind energy could cover as much as 80% of the country’s demand for electricity by 2030 [8]. Still, it is necessary to increase the stability (i.e., independence from weather factors) of solar and wind energies, the efficiency of their storage, as well as to better integrate them into the existing power systems [9].

The renewable energy market and information technologies are combining, resulting in the emergence of enterprises offering digital energy services (Utilities 4.0) [10]. Thanks to the economic potential, the platform model and digital competences [11,12] have already found their place in this big-tech market [13]. The digitalization of the renewable energy industry can also be considered as a sort of a market niche [14] that meets the needs of customers eager to buy renewable energy [15]. Startups in this industry are introducing new business models [16], however, to a rather limited degree if compared with the actual needs of this energy industry [17].

The purpose of this article is an attempt to identify a framework “digital compass” of business models in renewable energy. At the base of this study, there were: digital technologies, customer orientation, delivery of value, and revenue stream. The empirical analysis herein includes startups dealing with solar and wind energy, i.e., the energy industry characterised by the greatest dynamics of growth dynamics within the group of unstable energy sources. Data for the start-ups used in this analysis were collected from the dealroom database [18]. The identification of the “digital compass” of business models will enable us to answer the following questions: (1) To what extent do renewable energy startups manage to implement digital business models, and if so, which ones exactly? (2) Do renewable energy startups fit into the solution to the primary challenges faced by the renewable energy industry, i.e., storage and integration of the distributed energy sources to ensure supply security? As a complement to the principal research area, an attempt has been made here to answer the question as to what degree do big-tech players support digital startups in renewable energy, since it is big-tech that plays a key role in the development of the digital economy.

The article begins with a discussion of the research methodology that consists of five steps: (1) a review of literature concerning business models aimed at the basic features in the network approach, (2) identification of: (a) the sectors that develop most dynamically in the field of renewable energy i.e., solar and wind energy, (b) challenges for solar and wind energy in terms of energy storage and integration of unstable and dispersed energy sources, (3) collection and selection of data concerning renewable energy startups, focused on solar and wind energy, that implement business models in terms of energy storage and energy providers, (4) the collected and selected database created the basis for defining the location of the target group of startups, defined at the final stage of the database selection, (5) developing a synthetic/comprehensive overview of the typology of business models, the so-called compass in solar and wind energy, in the section of the two industries characterized by the most serious technological challenges concerning the storage and security of supplies (energy storage and energy providers) using R software. Section 3 presents the results of this study, including: (a) innovative business models and their implications for the energy sector, (b) digitalisation versus renewable energy challenges, (c) startups in the renewable energy sector, (d) big-tech in the renewable energy sector. Section 4 concludes core results, and identifies further research questions. The issues addressed herein represent a part of the challenges that renewable energy is facing today. The applied research algorithm enables us to pinpoint the digital gap in renewable energy. The gap in question includes areas that require institutional support to increase the investment attractiveness of renewable energy for new players of the digital market, within the conditions offered by tools available on the market today.

2. Data and Methods

The research methodology includes the following five steps.

First, there is a review of literature concerning business models aimed at the basic features in the network approach. The following issues have been addressed: (a) digital technologies as a source of value, (b) customer orientation in which customers themselves have increasingly worked as the creators of value, (c) delivery of value, (d) models of revenue streams in digital startups. The above features can be adopted as the framework indicators of digital business models.

Secondly, the following are identified: (a) the sub-industries that develop most dynamically in the field of renewable energy, i.e., solar and wind energy, (b) challenges for solar and wind energy in terms of energy storage and the integration of unstable and dispersed energy sources. This identification has influenced the selection of the research areas in the empirical part.

Thirdly, data concerning renewable energy startups, focused on solar and wind energy, that implement business models in terms of energy storage and energy providers, are collected. The latter was preceded by the determination of a target group, i.e., start-ups in industries (or sub-industries), in which business models were defined.

For these data from the dealroom database [18] and The International Renewable Energy Agency (IRENA) were applied [19]. The first database was of the utmost importance, since it links investors and dynamically growing companies, to provide information on the latter, generally unavailable in any other sources, especially in the field of technologies used. The research was based on data concerning the entry of new players to the energy industry, being startups and the representatives of big-tech. This approach was taken due to the fact that, in the development of renewable (low-carbon) energy, the so-called leaders are viewed as the actual drivers of these changes. The other cause lies in various initiatives launched by small players, also considered in the literature as social initiatives [20]. In terms of the digital transformation supporting the energy market transformation, the former can be viewed from the big-tech angle. Meanwhile, the latter are represented by startups that create niches aimed at energy transformation.

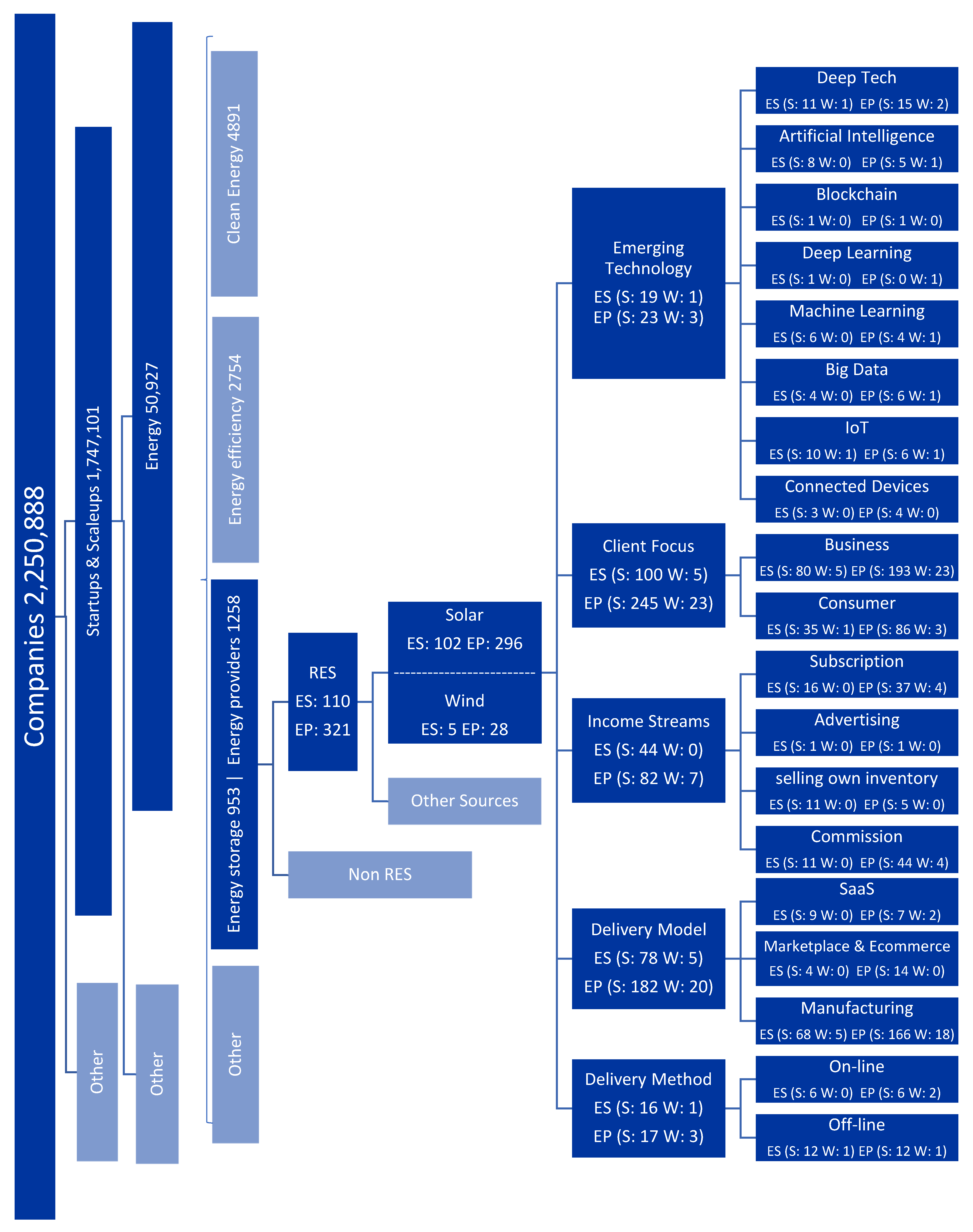

The collection of data on startups in the energy industry to allow their identification from the perspective of the framework digital business model included a number of stages of the starting base selection, illustrated in Figure 1. Purposive and stratified sampling was applied. The starting point was to extract data for startups from the energy industry as a whole, and then to narrow the scope of their penetration. First, the focus was limited to the sub-industries of clean energy, energy efficiency, energy providers, and energy storage. Based on the identification of their operations, these can be deemed representative of solutions particularly relevant to the energy transformation and the growth of renewable energy (the scope of the research did not include industries present in the energy industry of the Dealroom database, such as oil, oil and gas, and waste treatment solution). Then, startups within renewable energy were selected, with a particular focus on solar and wind energy. In the final stage, in agreement with the set purpose of the paper, the study area was further limited to startups in solar and wind energy in energy storage and energy provider industries.

The layer which led to the selection of the target group was the criterion of technologies applied in all the above sections. The identification was limited to the technologies most frequently indicated by startups, considered as emerging, i.e., deep tech, artificial intelligence, blockchain, deep learning, machine learning, big data, IoT, and connected devices (each startup indicated more than one technology, and often omitted it, which resulted in the fact that the summing up of the startup structure by technology does not always give 100%). The collection and selection of data are shown in the following diagram.

Fourthly, the collected and selected database created the basis for defining the location of the target group of startups, defined at the final stage of the database selection. This in turn allowed the authors to define their role versus the background of the energy industry as a whole, the above industries, and finally the technologies applied.

Fifth, a synthetic/comprehensive overview of the typology of business models was developed, regarding the so-called compass in solar and wind energy in the section of the two industries characterized by the most serious technological challenges concerning the storage and security of supplies (energy storage and energy providers) using R software. The R environment enabled the authors to design the research architecture and conduct a statistical, multi-dimensional analysis which provided the basis for the graphical presentations in the form of data clusters and the classification of the phenomenon under the research, including the business models [21,22]. The above were based on business model components identified in the literature of the subject as the frameworks for digital models, i.e., technology, customer orientation, delivery of value, and revenue stream. Simultaneously, considering the impact on the development of these technologies in the energy industry of the big players, i.e., big-tech, business models were presented, implemented by startups in which big-tech invested.

3. Results

3.1. Innovative Business Models—Implications for the Energy Industry

The business model concept is often analysed in the literature of the subject, defined and classified in various ways [23,24,25,26]. In the most general terms, its essence is to define the way a company or enterprise delivers value to its customers, encourages them to pay for the value, and transforms their payments into its own profit [24]. New possibilities of business model creation are connected with the introduction of Internet techniques which result in the dynamic development of digital business [27]. The above means the transition of the business model from the standard resource-based approach [23] to a model based on network and ecosystem effects [28,29]. The more innovative and effective the model is, the more value a given company captures for itself [30]. The source of the value can be the factors which drive the development of a digital economy, including the Internet of Things (IoT), Internet of Everything (IoE), cloud-based applications and services, big data analytics, or artificial intelligence algorithms. The above narrative also covers Industry 4.0 business models which focus on streamlining the standard value chain by improving automation and increasing operational efficiency [31]. In general, digital technologies can be considered as either (a) value delivered to customers, (b) a digital tool that enables fundamental changes in the operation of an enterprise [30]. The latter can be, for instance, replacing a product with services, which stems from the intangible nature of any digital product. In the digital economy, one can observe a significant growth in the number of enterprises which implement e-models of business, creating and delivering value to their customers via online channels [32].

Digital technologies provide a source of innovative B2B (business-to-business) and primarily B2C (business-to-customer) models. In addition, they enable the creation of new models with the customer at the centre. These are, for instance: B2B2C (business-to-business-to-consumer) and D2C (direct-to-consumer) [33]. Thanks to digital technologies, in these new business models, the customer is considered a prosumer, i.e., both a customer and a creator of value [34,35].

The group of innovative business models includes the platform model. It is usually a set of subsystems and interfaces that all create the enterprise’s business ecosystem (customers, partners, software developers, institutions) owned or merely used by the enterprise [36,37,38]. In the first scenario, it is a technology platform or a group of technologies that constitute the basis for the development of other applications, processes, or technologies. The virtual environment is created by a cloud, in which case the most widespread models are: SaaS (software as a service), PaaS (platform as a service), Iaas (infrastructure as a service) [39]. In the latter scenario, platforms create value by supporting the exchange between two or more interdependent groups which would otherwise find it hard to locate one another [40].

The search for new and innovative business models also takes place in the energy industry. According to Doleski, the innovative model in this industry differs from the traditional model: it expands its orientation on services by integrating dedicated digital solutions [10]. At its core, there are products that have turned into complex systems. They combine equipment, sensors, data storage, microprocessors, software, and connectivity in a vast variety of ways [41]. This results in a growing number of digital energy products which, in the power industry, are made available online in the form of data and information, e.g., concerning the dispersed energy sources and their users [42,43]. The literature of the subject provides different classifications of the archetypes of innovative business models in renewable energy [15,44,45]. They are said to lead to the development of digital services in the energy industry, better use of assets, as well as increased efficiency of the implemented business models [17]. These classifications are based on a resource-based approach and show an obvious dependence of revenue sources on regulation, not on the business model applied [44]. The network-based approach of the business models is in agreement with the attempted identification of energy platforms. According to Kloppenburg and Boekelo, these can be: provenance platforms (which support energy flows by registering prosumers and their resources), community platforms (which cooperate with the dispersed resources and actually direct energy flows), and access platforms (which enable consumers to buy, i.e., have access to selected renewable assets; in this case customers can have specific financial benefits) [46].

In business models based on network effects and ecosystems, particular significance is attached to revenue sources. These models are characterized by more potential sources [of revenues] versus the traditional ones, and are easier to configure [47], especially in the case of a platform [28]. In 2022, the group of the top five revenue models for startups included: commission-based business model, i.e., a fee for providing a platform for transactions, subscription business model, i.e., a fee for a periodic service, SaaS, i.e., a fee for software use, arbitrage business model, i.e., one uses exchange rate differences from operations in different markets, and finally advertising revenue model, i.e., revenues from advertisement [48]. Studies performed to date concerning business models in renewable energy have ignored the revenue streams.

3.2. Digitalisation versus Renewable Energy Challenges

A number of factors have contributed to the dynamic growth of renewable energy. It is expected that this process may even gain strength with the entry of global Big-Tech players into the renewable energy market [49]. They declare their eagerness to switch to renewable energy completely [50,51] and sign contracts to purchase this form of energy for their subsidiaries located in various regions of the world [52,53,54,55]. Between 2015 and 2020, ICT companies accounted for approximately a half of global corporate procurements for renewable energy [56].

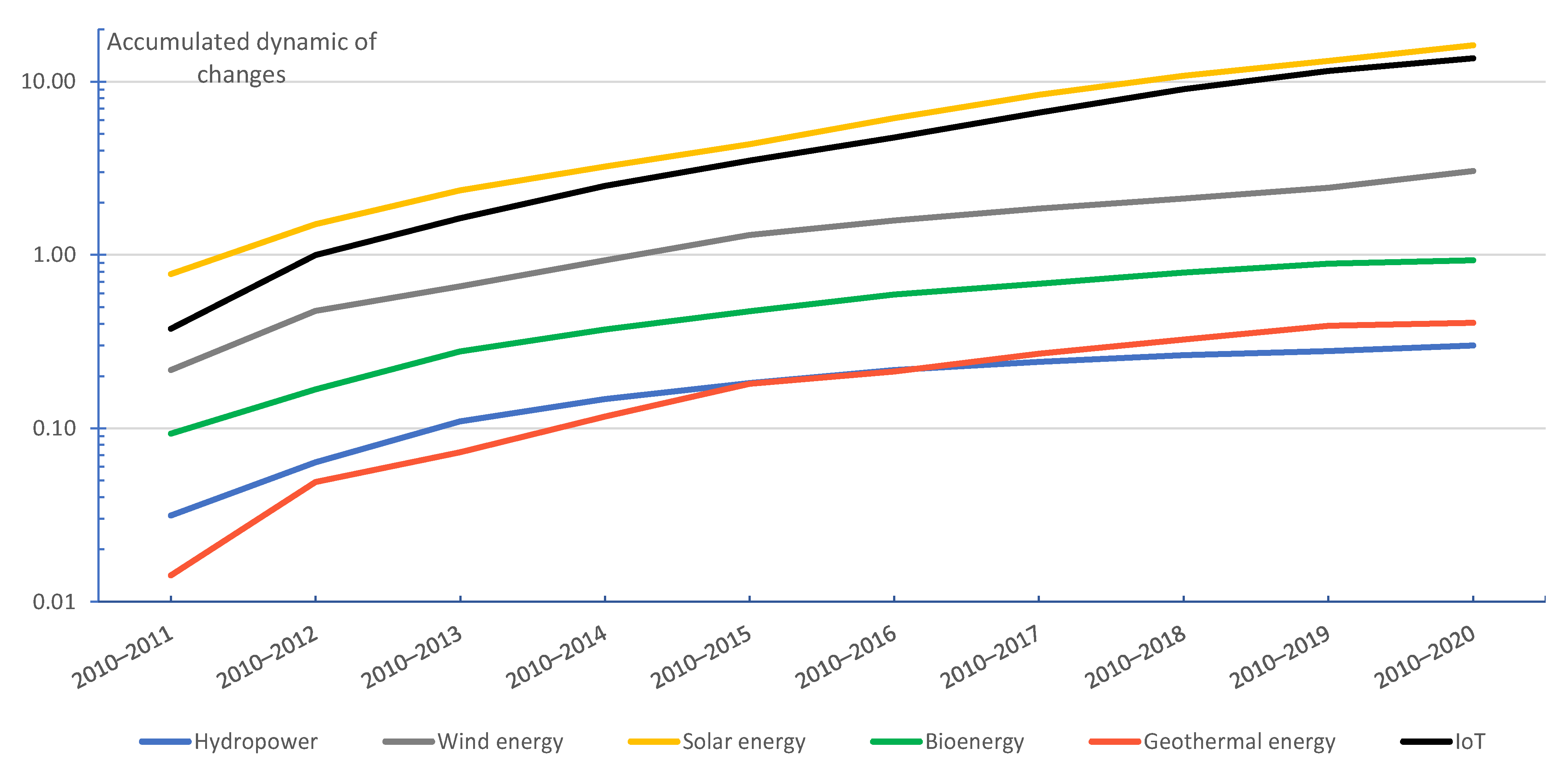

Such a transition to renewable energy which is based on unstable energy sources generates costs and creates new problems. Between 2010 and 2020, the total production capacity of RES energy increased from 1,226,853 MW to 2,799,094 MW (growth of 128%), while the number of devices connected to the grid globally increased from 16.2 billion to 23.5 billion (147%). The IoT, one of the technologies with the greatest growth (driven by new technology standards, e.g., 5 G) saw an over 13-fold increase in size (from 0.8 billion to 11.7 billion) [57], as shown in Figure 2. The International Energy Agency estimates that investments worth approximately USD 17 trillion will be required globally over the next 20 years, both in the new transmission and distribution networks and in emerging technologies [58].

In this section, great hopes are attached to the entry of players from outside the industry into the energy market, especially fin-tech’s financial support [59]. In 2020, the largest global investor (on an industrial scale) in renewable energy was Amazon [60].

In renewable energy, the challenge, especially for the sub-industries most dramatically growing in recent times, i.e., solar and wind energy, is to increase renewable energy stability. In this section, three issues are addressed most frequently: (1) increased predictability and the need for independence from weather factors [61], (2) storage of energy from renewable sources [62], (3) integration with dispersed users-producers and the existing energy system [63]. Even today, satellite data are applied for developing insulation forecasts, whereas satellite mapping and LIDAR (light detection and ranging) tools enable a more efficient design of the entire sun- and wind-based energy systems. Thanks to sensors with a new, higher level of control (e.g., drones, laser measurements), the amount of data provided by PV systems and wind turbines is growing exponentially [46]. This translates into an increasing demand for analytical solutions for large data sets in the energy industry.

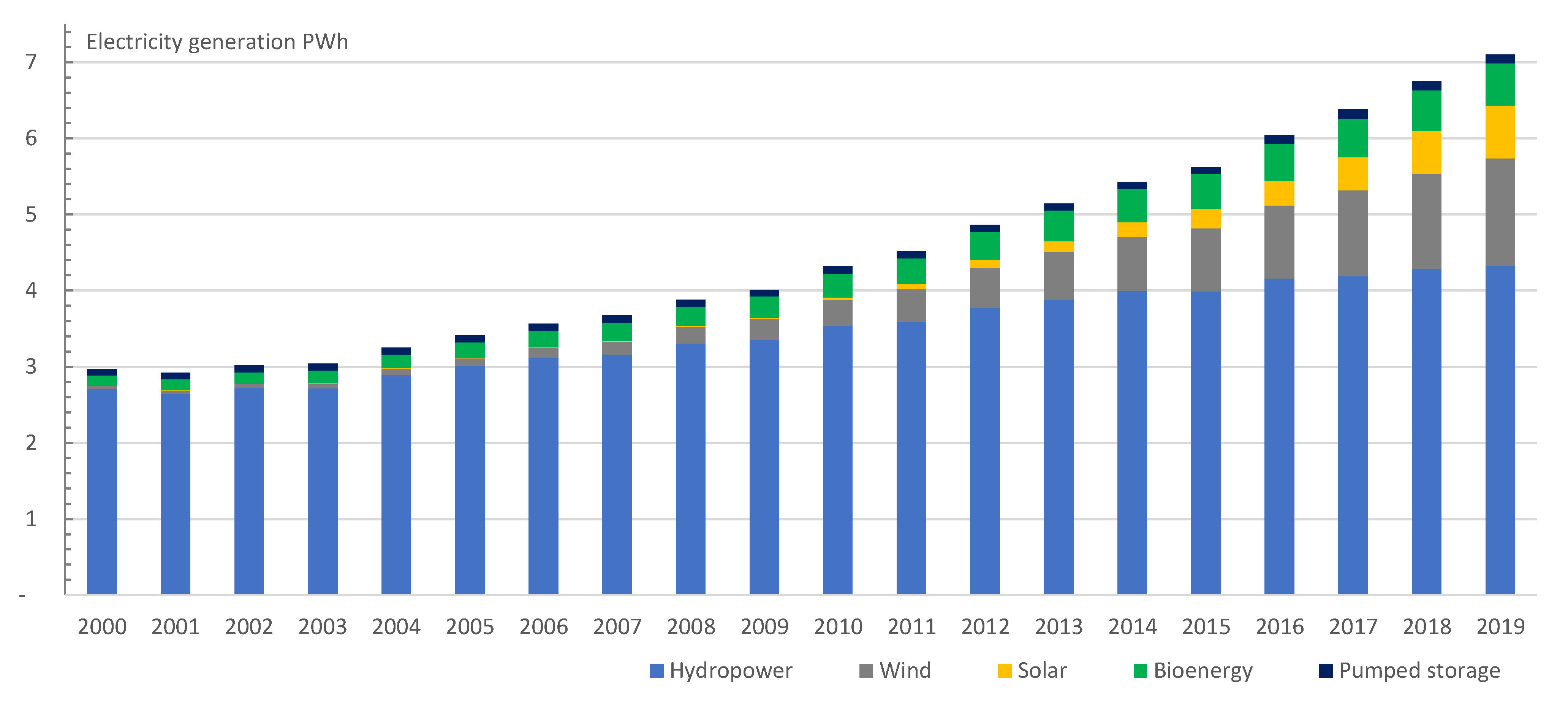

The problem of energy storage concerns primarily PV and wind energy, which accounted for the greatest dynamics of growth in the recent period (2010–2020) (approximately 16.2-fold and approximately three-fold growth, respectively) [64], as presented in Figure 2. The dynamic development of battery technology is linked with decreasing battery costs [65]. However, renewable energy storage capacity still does not meet the needs. This applies particularly to electricity. The largest, but still small, storage capacity of this form of energy is recorded for water turbine plants, which still represent the most significant source of renewable electricity in the world (about 94.6% in 2000 and 62.1% in 2019). Between 2010 and 2019, the storage of energy in pumped storage power plants accounted for between approximately 3.1% and 2.6% of the world’s total hydropower generation, as shown in Figure 3. Furthermore, new research shows that the massive storage of renewable energy increases CO2 emissions [66].

The penetration of nondispatchable PV and wind power is estimated at the level of 20% and 30%, respectively [67]. The situation can be improved with flexible renewable energy storage systems [68], as well as more efficient analytical tools and the application of artificial intelligence algorithms [69] for the real-time management of energy systems. The digitalisation of energy management is also associated with lower losses in transmission, and thus lower costs [70]. The future success in this respect depends on large platforms, and not only the implementation of digital tools by energy enterprises [67].

3.3. Startups in the Renewable Energy Industry

Digital transformation is also the result of startups being involved in digital technologies. This especially applies to those startups whose ideas and technological solutions provide the optimum answer to the challenges that the energy industry is facing. A manifestation of this is, i.a., the growing number of startups that apply virtual reality in the energy industry [71]. Moreover, they are interested in AI, machine learning, deep learning, and blockchain [15].

The global number of startups and scaleups that have targeted their operations to activities directly related to the energy industry, found in the Dealroom database [18], was 50,927 in January 2022. The clean energy, energy efficiency, energy providers, and energy storage sub-industries accounted for 7954 startups (i.e., 15.6% of the total number). Renewable energy was represented by 2645 (5% of the total number) startups, including solar and wind energy, by 2234 and 331 (4% and 1% of the total number) startups, respectively.

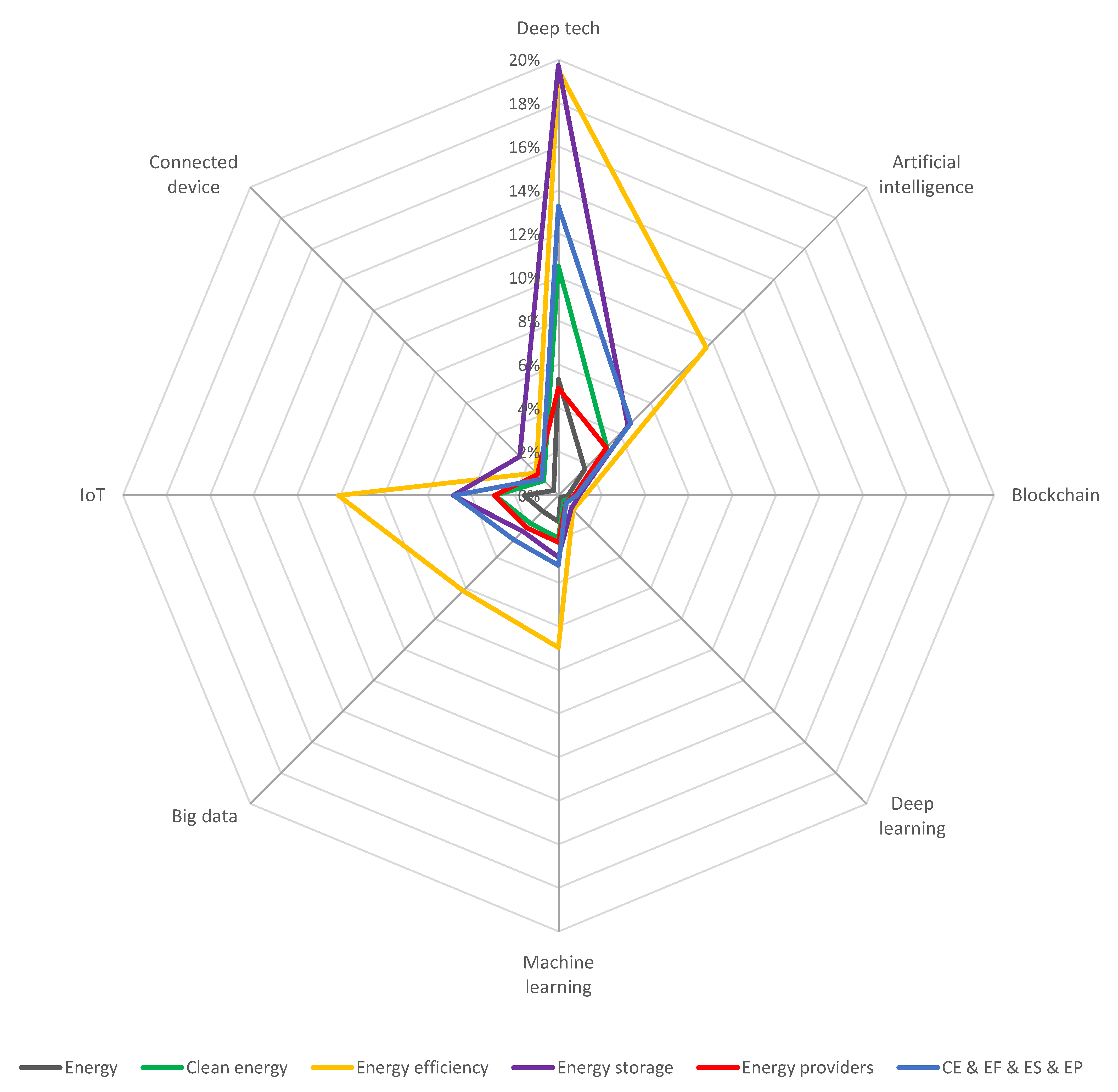

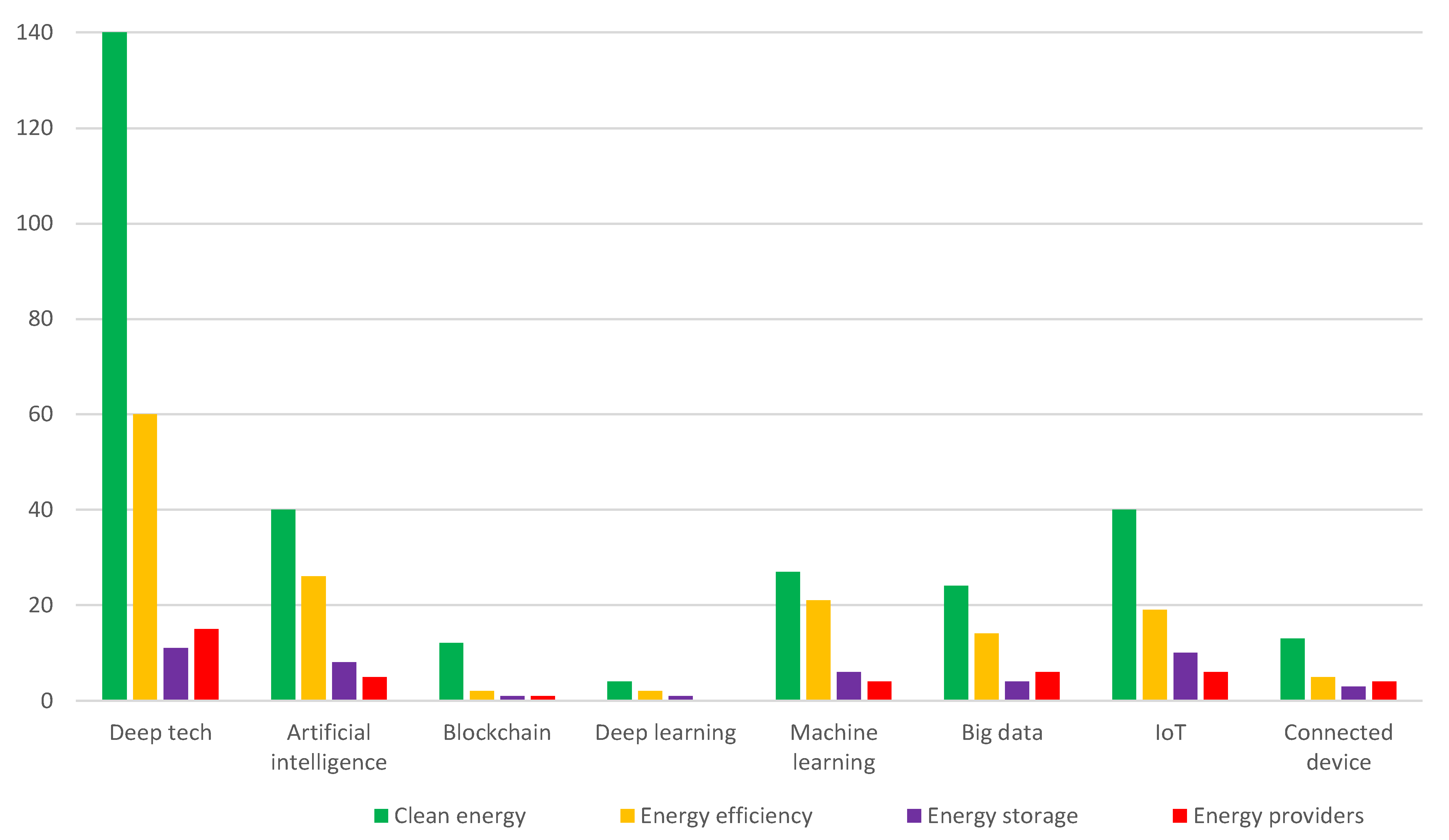

Unfortunately, the digital technologies applied in their business models are rare. The most widely used are deep tech, artificial intelligence, blockchain, deep learning, machine learning, big data, IoT, and connected devices. The number of startups in the energy industry involved in at least one of the above solutions was only 3262, i.e., less than 6.4% of the total number of startups in the industry. Simultaneously, among the four energy sub-industries shown above, they accounted for 16.6% (1322 within a group of 7954) and directly in renewable energy: 386 (15% of the total number). Their greater technological involvement in the energy industry as a whole can be observed primarily in the energy efficiency and storage sub-industries rather than in the clean energy sub-industries, particularly in energy suppliers (Figure 4).

Although technologies, such as IoT/IoE, big data analytics, AI, and machine learning, are considered as digital development drivers of the energy industry and as those which shape business models, among the potentially usable technologies, the identified startups mainly indicate the application of deep tech (13.9% in the four above sub-industries). Thus, startups focus on a single technological option, which is also reflected in other research [45]. In addition, companies based on deep tech create their value primarily by developing new solutions and not merely by modifying the existing business models. They are characterised by a high impact (on their environment), long time to reach market maturity, and significant capital requirements. This technology plays the most significant role among startups in energy industry, such as storage (19.7%, which indicated the application of at least one technology out of their total number of 953), followed by IoT, and finally AI, as illustrated Figure 4. It is worth stressing here that in the sub-industry, significant for the energy transformation, i.e., energy providers, represented by 1258 startups, technologies are much less important than in the energy storage sub-industry. In the latter case, fewer than 5% subjects indicated deep tech and about 3%—respectively AI and IoT, while the other technologies, also significant for the industry, in the form of connected device, proved to be the area of involvement for about 1.4% of the total indications.

In terms of renewable energy, in particular solar and wind, it is worth noting that the vast majority of companies were startups dealing with solar energy (2234 out of 2645 of total RES, i.e., 84.5%), followed by wind energy with merely 12.5% of the total pool. The interest of startups in other RES sources (e.g., geothermal energy, hydropower, marine, energy, or biomass) is negligible. Within solar energy, the majority of the subjects focused their operations on clean energy (1424 out of 2234, i.e., 63.7% of the total), while the interest in energy storage and providers was significantly lower (102 startups, 4.5% of the total; and 296 startups, 13.3% of the total, respectively).

The majority of startups that apply at least one of the above technologies in terms of RES-based energy operate in the field of solar energy (81% of the total number of startups that use technologies in RES), primarily in clean energy and efficiency industries. Still, they account for 14% of the total number of startups in solar energy, whereas in wind energy startups applying at least one technology account for 23% of all wind energy startups; see Table 1.

The majority of startups in solar energy use deep tech (276 startups out of 312 that indicated the application of at least one technology out of a total of 2234). A few more such startups are found in solar energy delivery rather than in storage, but still, it is in storage that their share is slightly higher (respectively 15 and 11 out of 296 and 102 of total startups in solar energy). The application of the other technologies is significantly lower. Among these technologies, AI and IoT are a bit more significant. Apart from clean energy, the above applies to energy storage (eight and 10 startups, respectively), while in the case of energy providers their application is lower (five in AI and six in IoT, respectively), as illustrated in Figure 5.

The total number of startups in solar energy dealing with at least one of the technologies in question was 19 startups in energy storage and 23 in energy provision, i.e., 90% and 96% respectively in the total group of subjects using RES technologies.

A significantly smaller number of startups operating on the basis of at least one technology is characteristic for wind energy. Only 65 startups (out of 75 that declared the application of at least one technology) out of 331 indicated their use of deep tech. This technology dominates in such sections (sub-industries) as clean energy and energy efficiency. In the energy storage and energy providers sub-industries deemed as key for the energy transformation, the application of this technology, as well as others, is negligible (Figure 6). In total, modern technologies in these two energy sub-industries were represented by only four startups: three in energy supply and one in energy storage.

In conclusion, the significantly higher interest in technology shown by startups in these sub-industries is characteristic of solar power, with the predominant application in the supply area (in numbers) and a generally higher relative share in energy storage. Moreover, worth noting is the negligible number of startups that apply connected device technologies, significant for operations within any platform system (seven in solar power and zero indication in wind power).

Considering the initially posed research questions, it becomes important to specify the business models used by startups that apply at least one of the above technologies found in solar and wind energy in storage and providers sub-industries (19 startups in storage and 23 in the energy providers in solar energy, and one and three in wind energy, respectively).

The identification of these digital business models was performed according to the adopted research algorithm, while referring to the purposive research sample described above. The results are presented in the sections shown below which make the key components of the digital business model:

- (1)

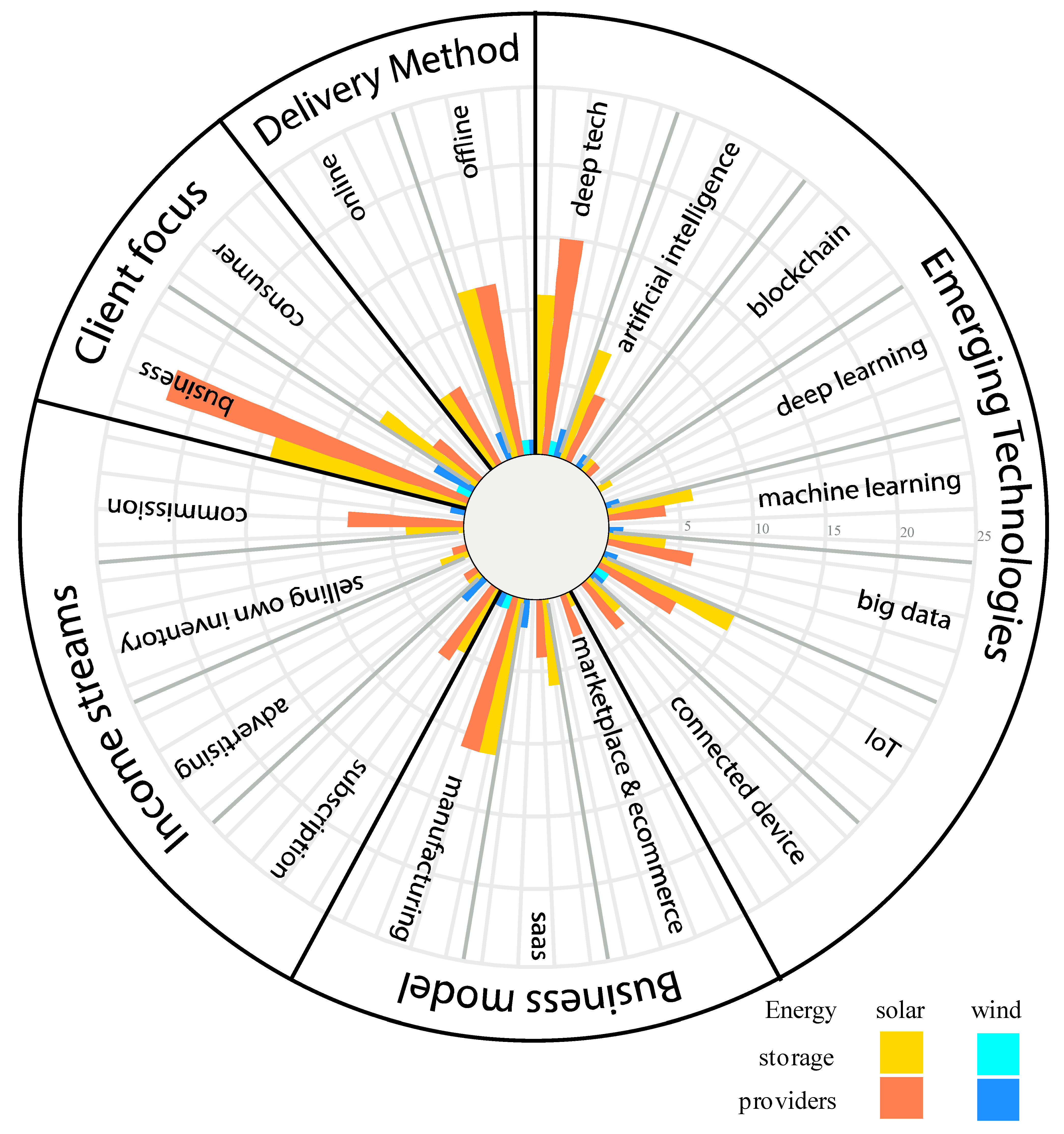

- Technology: Deep tech is of primary importance in solar energy, being slightly less significant in IoT (respectively 57.9% and 52.6% of indications by startups in the storage sub-industry, while 65.2% and 26.1% in the providers sub-industry). As it can be construed from the figure, the other technologies are applied (regardless of the sub-industry) rather sporadically (Figure 7).

In the case of wind energy, a too small sample was used to draw any conclusions as to the technologies applied.

- (2)

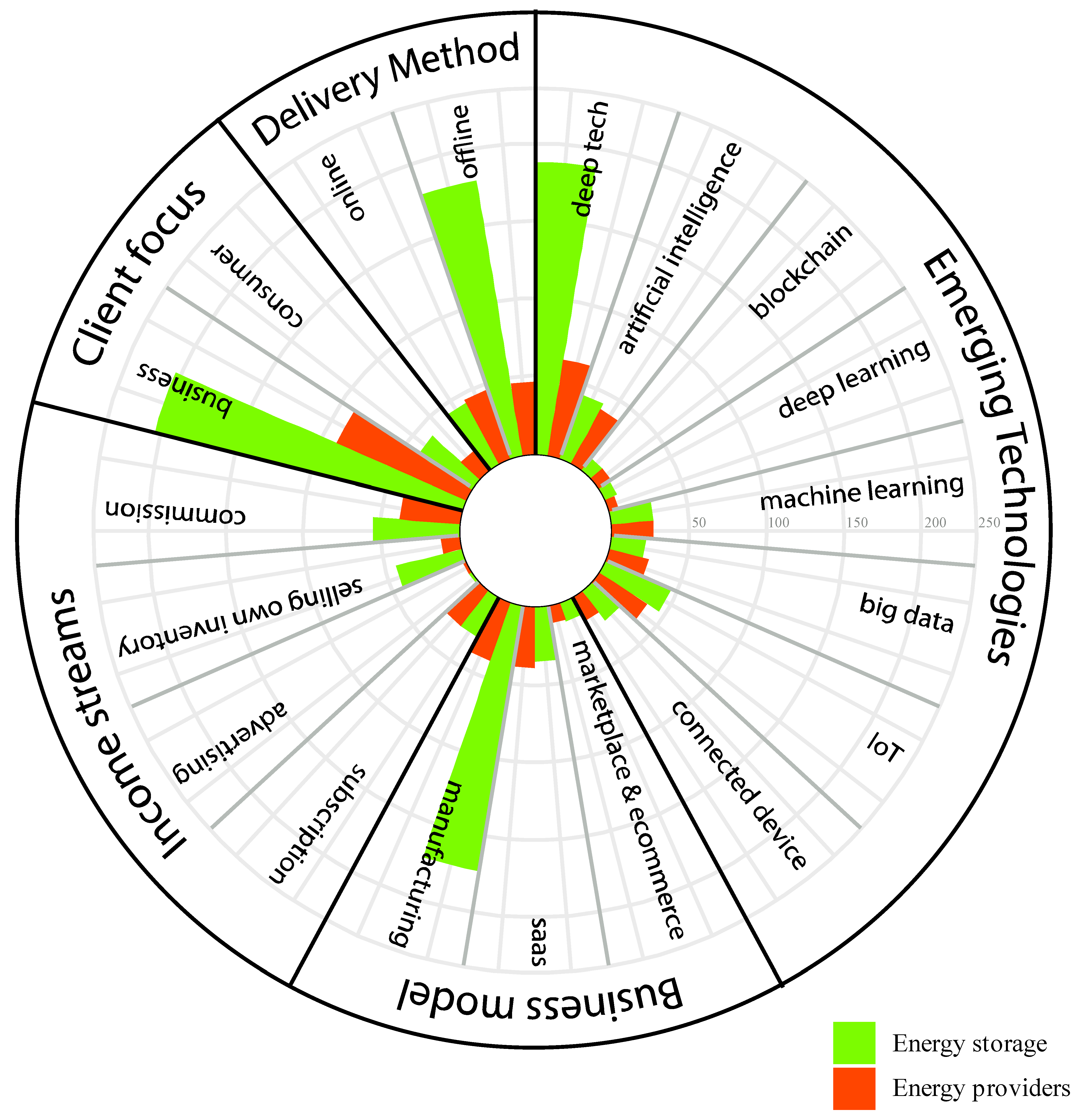

- Target customer. The business models in solar and wind energy applied by startups using at least one of the above technologies are primarily B2B models (i.e., 96% of the total subjects in solar energy, storage sub-industry, and 64% in the energy providers sub-industry, and by all the few subjects in wind energy), as shown in Figure 7. With regard to the models in the energy industry as a whole, the above means that B2B models are frequently found in the solar energy and energy providers sub-industry, while in the energy storage sub-industry the percentage using the B2B model is lower than the average in this energy industry, as illustrated in Figure 8.

- (3)

- The type of services provided. Due to the specific features of the identified startups (the application of digital technologies) and the limited nature of the database used for the research, the authors focused on indicating the scope of the SaaS service. The analysed start-ups to a relatively small degree fit into SaaS-based models, although the solar energy storage sub-industry stands out quite positively in this regard against the entire energy industry (37.5% of the total in this industry, with a much smaller percentage of startups, 3.5% in the solar energy providers sub-industry). Considering a negligible number of startups that apply at least one of the above technologies in these two sub-industries, such a model in wind energy is implemented by two out of three subjects in the energy providers sub-industry and is not found at all in the energy storage sub-industry.

Figure 7.

Compass of business models in solar and wind energy.

Figure 8.

Compass of business models in the energy storage and providers sub-industries.

- (4)

- Revenue stream. Most of the startups in the identified group in solar energy base their revenues on subscriptions or commissions. In the energy storage sub-industry, they accounted for 55.6% of the startups within the group that applies at least one technology. About 44% subjects indicated commission as their source of revenue. In the energy providers sub-industry, the opposite situation was observed, with the majority of subjects indicating commission as their revenue stream (61.5% of the total number), followed by subscription at 46.2%. The sale of the company’s own resources and advertising were much less important in both sub-industries (about 22% and 11% respectively in the storage industry and 7.7% each in the providers industry). In wind energy, in the small group of startups that apply at least one technology, the actual identification of revenue sources was recorded only in the energy providers sub-industry. As their revenue sources, these start-ups indicated only subscription and commission. In the revenue model of the “technological” solar sector startups as compared to the energy industry as a whole, subscription prevails in both sub-industries under analysis, especially in energy storage (55.6% vs. 16.9% in this energy sub-industry and respectively in the energy providers sub-industry: 46.2% vs. 25.7%). Commission, in turn, is a more frequently indicated source of revenue in the discussed energy sub-industries as a whole than in solar and wind energy. Simultaneously, in the energy industry, the sale of the company’s own resources is indicated by startups (right after subscription) as their source of revenue more frequently than commission.

- (5)

- Manner of provision (online, offline). The actual provision of customer value in the group of startups in solar and wind energy indicates the traditional business models. The above confirms the previous observations concerning the infrequent application of digital technologies and the focus of the provided services on selling manufactured goods and services to customers (manufacturing).

3.4. BigTech in Renewable Energy

The 21st century is the era of the platform economy, in which the leading role has been attributed to big-tech. Big-tech players are present in almost all market segments, including the energy market [12]. Platforms related to the energy industry do not focus only on energy but operate at the borderline between energy and other industries. A relatively large number of these entities operate in financial technology (i.e., FinTech), transport, software for enterprises, and the Internet of Things (IoT) [72].

The energy crisis has accelerated the attempts to find new opportunities to develop renewable energy and improve its efficiency. Big-tech has been actively involved in these works. The leading players in this field are Microsoft, Apple, Facebook, IBM, Amazon, and Google, the so-called G-MAFIA, which monopolises the global economy [73]. They are investing in various fields of the energy industry. Their aim includes financial benefits [74] and/or creating their pro-environmental image as, i.e., greenspinning [75]. The company size [76] and the declared CSR are conducive to environment-friendly investment strategies. The most common projects here are implemented in the field of solar and wind energy on an industrial scale, often combined with the storage of the generated energy [51,77,78,79]. Moreover, providers to big-tech players are expected to take a shift towards renewable energy [80]. At times, these actions are considered as building a corporate image. For instance, Apple has declared their transition to a zero-carbon economy [81], whereas Apple data centres run on 100% reliable local utility power, to a large extent fired with coal (e.g., in China) [82]. Additionally, the clouds hosted by Amazon, Google, IBM, and Microsoft offered for public access, despite their operators’ declarations, are not completely green [83]. Still, these platforms meet the challenges that NGEs face, i.e., managing the increased potential in the conditions of the volatility (in supply as well as demand) of the energy equation [84]. An example here can be Amazon Web Service, which provides companies from the energy industry with a basis (cloud-based) to transform their complex business and operational systems [85].

Big-Tech players invest in innovative startups and acquire those which show high growth potential [86]. The Dealroom database shows that out of the total of 50,927 startups in the energy industry, big-tech companies have engaged in merely 59. The largest investor here is Google (33 startups, including 12 in the above four sub-industries of key importance for the energy transition, i.e., clean energy, energy efficiency, energy storage and energy providers). Smaller investment interest is shown by Amazon (the company invested in 16 startups, including nine in the above industries) and Microsoft (eight and three startups, respectively). No investments of this kind were reported by Facebook, whereas Apple and IBM have invested in a negligible number of startups (two and one, respectively). In the energy storage and energy providers sub-industries, only seven startups in total have become the subject of big-tech’s investments, of which Amazon invested in four startups, followed by Microsoft, in two, and Apple in one (see Table 2). It is worth mentioning here that solar energy was the subject of the investment interest of only Microsoft (1 startup). Not a single big-tech investment in wind energy has been found.

The majority of the startups in which big-tech players have engaged based their model on deep tech. While engaging in the energy transformation, they focused their operations primarily on business-to-business (B2B) customers. Most of them obtained their revenues mainly from commissions. Simultaneously, these startups, unlike the ones identified in the target group of this research, performed only industrial operations, basically limited to the manufacture of products sold to customers (manufacturing). The above means their lack of involvement in SaaS solutions, specific for the digital business model.

4. Conclusions and Perspectives for Further Research

The third decade of the 21st century marks a period called the new digital economy (NDE) [87]. In the area of energy, the idea is to be reflected in the NEE, to be accompanied by the entry of digital enterprises into the energy market. These enterprises implement digital business models based on a network approach, which, for the sake of this research, were limited to the following four elements: digital technologies, customer orientation, delivery of value, and revenue stream. With the entry of digital companies into the energy market, a great deal of benefits is expected in renewable energy, especially solar and wind industries. Recent investments in this market segment have frequently been of industrial nature, but are performed in the conditions of the still present challenge of their storage and an integrated supply system that would guarantee the security of this storage. The research performed in the group of startups in the renewable energy industry, within the scope expanded to include big-tech’s investment directions, question the appeal of renewable energy for new digital players. The above is proven by the small number of startups in the renewable energy industry (5% of the total number of startups). Their interest in new technologies is equally low (15% of the total from RES). Similar observations apply to handling issues related to storage and supply. Thus, the significantly higher number of technology startups operating in solar energy than in the wind energy industry failed to translate into a correspondingly high interest of the subjects in the energy storage or energy provider industries. However, it is worth pointing out that they accounted for a significantly bigger share in the total number of solar-industry startups active in the energy storage industry. The startups used, in particular, deep tech solutions. The other technologies, especially those required for ensuring the stability of supply from dispersed sources and for energy storage were of negligible importance. Those startups that engage in modern technologies combine them with participation in energy projects aimed at increasing efficiency (using less energy to provide the same energy level by means of energy-saving technologies, smart grid, energy-efficient buildings) as well as the so-called clean energy (reduction of CO2 emissions by improving energy efficiency and the use of environmentally friendly resources or activities), whose scope is not limited to renewable energy sources as such.

The low rate of digital technology application makes one think: to what extent do startups in renewable energy really implement digital business models? The findings from the authors’ own compass of business models in solar and wind energy in the two sub-industries, i.e., energy storage and energy providers, show that the degree of their digitalisation is negligible. The vast majority of the subjects operated like traditional energy companies, i.e., in the B2B model, offering their business partners manufactured/provided goods and services (manufacturing) using offline delivery method. Against this background, as it was already indicated above, the business models in solar energy and energy storage stand out as a bit more favourable. To some degree, this results from a significantly higher growth rate of investments in solar projects vs. wind ones. The research also confirms the fact that startups in renewable energy, like other companies of this kind, base their revenues on subscription or commission schemes.

The role of big-tech seems ambiguous when it comes to its assessment along the path towards the digital transformation of the energy industry. First, it is associated with its growing degree of privatisation [20]. In 2021, Amazon became the largest corporate buyer of renewable energy in Europe [77]. However, in the US, the leading technology behemoths, including Amazon, Apple, Facebook, Google, and Microsoft, accounted for 38% of the total renewable energy contracts concluded between 2015 and 2020 [88]. Experience from the other industries shows that, in the long term, this can result in big-tech players taking on a greater role than the state itself, bearing in mind the utmost significance of this market for every country [73]. Furthermore, the appearance of new players from outside of the industry may entail the decline and fall of the established, traditional business models [89] and, in consequence, hamper the transition to sustainable energy systems in many regions of the world [20]. Second, the empirical research shows that big-tech players fail to show their interest, as it is the case in other innovative economic industries, in financing or purchasing startups operating in solar and wind energy which aim at improving the efficiency of energy storage and provision. This is an indirect proof of these startups’ low appeal. The latter aspect could change if big-tech companies supported the startups with their digital competences instead of limiting their actions to manufacturing only.

In conclusion, the expansion of digital technologies in renewable energy leads to a more dynamic energy transformation as well as to a proliferation of entities that apply new business models [90]. Still, the extent of these changes is slow and also conditioned by certain non-technological factors. According to other research, business models in renewable energy are deeply rooted in the frameworks of politics and regulations. In solar energy, these are, among others, tariff policies. The existence of capacity remuneration mechanisms established by regulators and legislatures play an important role in the distribution of energy [44]. Therefore, an important research question that emerges is not how digital tools are changing the business models in renewable energy, but rather why these tools, so available and widely applied in other industries, are not used in renewable energy?

It seems necessary to improve the conditions for business model innovation, especially for start-ups and new entrants. The tools in the section are grants and funds available for start-ups, funded mentors, a number of organizations that bridge start-ups and industry, and a number of policies promoting innovation [91]. The rapidity and stability of the energy transformation depend largely on the adaptation speed of the regulatory framework and on the ability of market players to develop appropriate business models.

Author Contributions

Conceptualization, T.P. and M.P.-J.; methodology, T.P. and M.P.-J.; formal analysis, T.P. and M.P.-J.; investigation T.P. and M.P.-J. resources; writing—original draft preparation, T.P. and M.P.-J.; writing—review and editing, T.P. and M.P.-J.; visualization, T.P. and M.P.-J.; supervision, T.P. and M.P.-J. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Publicly available datasets were analyzed in this study. This data can be found here: https://www.irena.org/Statistics (accessed on 19 January 2022); https://www.iea.org/data-and-statistics (accessed on 19 January 2022); https://dealroom.co (accessed on 2 March 2022); https://iot-analytics.com/ (accessed on 1 February 2022).

Conflicts of Interest

The authors declare no conflict of interest.

References

- World Energy Outlook 2021—Analysis. Available online: https://www.iea.org/reports/world-energy-outlook-2021 (accessed on 19 January 2022).

- Schoklitsch, H. Digitalization Is Revolutionizing the Renewable Energy Sector. Renewable Energy World. 2018. Available online: https://www.renewableenergyworld.com/storage/digitalization-is-revolutionizing-the-renewable-energy-sector/ (accessed on 19 January 2022).

- IEA. Digitalisation Making Energy Systems Smarter, More Connected, Efficient and Resilient. Available online: https://www.iea.org/topics/digitalisation (accessed on 20 February 2022).

- IRENA. Climate Change and Renewable Energy: National Policies and the Role of Communities, Cities and Regions. A Report from the International Renewable Energy Agency (IRENA) to the G20 Climate Sustainability Working Group (CSWG). Available online: https://www.irena.org/-/media/Files/IRENA/Agency/Publication/2019/Jun/IRENA_G20_climate_sustainability_2019.pdf (accessed on 20 February 2022).

- Bruckner, T.; Bashmakov, I.A.; Mulugetta, Y.; Chum, H.; de la Vega Navarro, A.; Edmonds, J.; Faaij, A.; Fungtammasan, B.; Garg, A.; Hertwich, E.; et al. Energy Systems. In Climate Change 2014: Mitigation of Climate Change; Contribution of Working Group III to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change; Edenhofer, O., Pichs-Madruga, R., Sokona, Y., Farahani, E., Kadner, S., Seyboth, K., Adler, A., Baum, I., Brunner, S., Eickemeier, P., et al., Eds.; Cambridge University Press: Cambridge, UK, 2014; pp. 513–597. [Google Scholar]

- Nilsen, E. Even before Ukraine Crisis, Majority of Americans Wanted Country to Prioritize Renewable Energy Development, Poll Shows. Available online: https://www.cnn.com/2022/03/01/politics/renewable-energy-poll-ukraine-climate/index.html (accessed on 2 March 2022).

- Msika, M. European Renewables Stocks Surge as Ukraine War Fuels Energy Reckoning. Available online: https://www.bloombergquint.com/technology/european-renewables-surge-as-ukraine-war-fuels-energy-reckoning (accessed on 2 March 2022).

- Germany Speeds up Renewable Energy Push Due to Ukraine Invasion. Available online: https://www.euronews.com/green/2022/02/28/germany-to-speed-up-renewable-energy-push-amid-ukraine-invasion (accessed on 2 March 2022).

- Carroll, D. New Report Identifies Digitalization as Renewable Energy Driver. PV Magazine, 19 March 2021. Available online: https://www.pv-magazine-australia.com/2021/03/19/new-report-identifies-digitalization-as-renewable-energy-driver/ (accessed on 12 August 2021).

- Doleski, O.D. Utility 4.0: Transformation Vom Versorgungs-Zum Digitalen Energiedienstleistungsunternehmen; Essentials; Springer Vieweg: Wiesbaden, Germany, 2016; ISBN 978-3-658-11550-0. [Google Scholar]

- Evans, D.S.; Hagiu, A.; Schmalensee, R. Invisible Engines: How Software Platforms Drive Innovation and Transform Industries; Social Science Research Network: Rochester, NY, USA, 2016; ISBN 978-0262550680. [Google Scholar]

- Kenney, M.; Rouvinen, P.; Seppälä, T.; Zysman, J. Platforms and Industrial Change. Ind. Innov. 2019, 26, 871–879. [Google Scholar] [CrossRef]

- Croutzet, A.; Dabbous, A. Do FinTech Trigger Renewable Energy Use? Evidence from OECD Countries. Renew. Energy 2021, 179, 1608–1617. [Google Scholar] [CrossRef]

- Renzi, E.; Michele, S.; Zheng, S.; Jin, S.; Greaves, D. Niche Applications and Flexible Devices for Wave Energy Conversion: A Review. Energies 2021, 14, 6537. [Google Scholar] [CrossRef]

- Küfeoğlu, S.; Liu, G.; Anaya, K.; Pollitt, M.G. Digitalisation and New Business Models in Energy Sector; Energy Policy Research Group, University of Cambridge: Cambridge, UK, 2019. [Google Scholar] [CrossRef]

- Chasin, F.; Paukstadt, U.; Gollhardt, T.; Becker, J. Smart Energy Driven Business Model Innovation: An Analysis of Existing Business Models and Implications for Business Model Change in the Energy Sector. J. Clean. Prod. 2020, 269, 122083. [Google Scholar] [CrossRef]

- DNV GL. Digitalization and The Future Of Energy. Beyond the Hype—How to Create Value by Combining Digital Technology, People and Business Strategy. Available online: https://smartenergycc.org/wp-content/uploads/2019/07/Digitalization_report_pages.pdf (accessed on 2 March 2022).

- Dealroom.Co|Identify Promising Companies before Everyone Else. Available online: https://dealroom.co/ (accessed on 2 March 2022).

- IRENA. Data & Statistics. Available online: https://www.irena.org/Statistics (accessed on 6 March 2022).

- Kloppenburg, S.; Boekelo, M. Digital Platforms and the Future of Energy Provisioning: Promises and Perils for the next Phase of the Energy Transition. Energy Res. Soc. Sci. 2019, 49, 68–73. [Google Scholar] [CrossRef]

- Freeman, M.; Joel, R. Data Science. Programowanie, Analiza i Wizualizacja Danych z Wykorzystaniem Języka R; Wyd. Helion: Gliwice, Poland, 2019. [Google Scholar]

- Nowosad, J. Geostatystyka w R; UAM: Poznan, Poland, 2019; ISBN 978-83-953296-0-9. [Google Scholar]

- Osterwalder, A.; Pigneur, Y. Business Model Generation: A Handbook for Visionaries, Game Changers and Challengers; John Wiley & Sons: Hoboken, NJ, USA, 2010; ISBN 13 978-0470876411. [Google Scholar]

- Teece, D.J. Business Models, Business Strategy and Innovation. Long Range Plan. 2010, 43, 172–194. [Google Scholar] [CrossRef]

- Chesbrough, H. Business Model Innovation: Opportunities and Barriers. Long Range Plan. 2010, 43, 354–363. [Google Scholar] [CrossRef]

- Nagumo, T. Innovative Business Models in the Era of Ubiquitous Networks. Nomura Res. Inst. 2002, 49, 1–13. [Google Scholar]

- Chaffey, D. Digital Business and E-Commerce Management; Pearson: London, UK, 2019; ISBN 13 9780273786542. [Google Scholar]

- MIT CSIR. Three Types of Value Drive Performance in Digital Business. Available online: https://cisr.mit.edu/publication/2021_0301_ValueinDigitalBusiness_SebastianWeillWoerner (accessed on 17 February 2022).

- Jacobides, M.; Cennamo, C.; Gawer, A. Towards a Theory of Ecosystems. Strateg. Manag. J. 2018, 39, 2255–2276. [Google Scholar] [CrossRef] [Green Version]

- Amit, R.H.; Zott, C. Business Model Innovation: Creating Value in Times of Change; IESE Business School Working Paper; IESE Business School: Barcelona, Spain , 2010; p. 870. Available online: https://ssrn.com/abstract=1701660 (accessed on 1 February 2022).

- Burmeister, C.; Luettgens, D.; Piller, F.T. Business Model Innovation for Industrie 4.0: Why the “Industrial Internet” Mandates a New Perspective on Innovation. Die Unternehm. 2016, 6, 124–152. [Google Scholar] [CrossRef]

- Weill, P.; Vitale, M.R. Place to Space: Migrating EBusiness Models-Making Clicks Become Bricks. Available online: http://hbswk.hbs.edu/archive/2381.htmlplace-to-space-migrating-ebusiness-models-making-clicks-become-bricks (accessed on 17 March 2022).

- Changing Business Models 2019. Available online: https://info.sana-commerce.com/rs/908-SKZ-106/images/Changing%20Business%20Models%20WP%20EN.pdf (accessed on 17 March 2022).

- Wiechoczek, J. Creating Value for Customer in Business Networks of High-Tech Goods Manufacturers. J. Econ. Manag. 2016, 23, 76–90. [Google Scholar]

- Xie, C.; Bagozzi, R.P.; Troye, S.V. Trying to Prosume: Toward a Theory of Consumers as Co-Creators of Value. J. Acad. Mark. Sci. 2008, 36, 109–122. [Google Scholar] [CrossRef]

- Gawer, A. Bridging Differing Perspectives on Technological Platforms: Toward an integrative framework. Res. Policy 2014, 43, 1239–1249. [Google Scholar] [CrossRef] [Green Version]

- Rochet, J.C.; Tirole, J. Platform Competition in Two-Sided Markets. J. Eur. Econ. Ass. 2003, 1, 990–1029. [Google Scholar] [CrossRef] [Green Version]

- Parker, G.G.; Van Alstyne, M.W. Two-Sided Network Effects: A Theory of Information Product Design. Manag. Sci. 2005, 51, 1494–1504. [Google Scholar] [CrossRef] [Green Version]

- Knorr, E.; Gruman, G. What Cloud Computing Really Means. Available online: https://www.coursehero.com/file/52422256/What-Cloud-Computing-Really-Meanspdf/ (accessed on 5 March 2022).

- Evans, P.C.; Gawer, A. The Rise of the Platform Enterprise. Energing Platf. Econ. Ser. 2016, 1, 1–27. [Google Scholar]

- Porter, M.E.; Heppelmann, J.E. How Smart, Connected Products Are Transforming Competition. Harv. Busines Rev. 2014, 92, 64–88. [Google Scholar]

- Kularatna, N.; Gunawardane, K. Energy Storage Devices for Renewable Energy-Based Systems. Rechargeable Batteries and Supercapacitors, 2nd ed.; Elsevier: Amsterdam, The Netherlands, 2021; ISBN 13 9780128207789. [Google Scholar]

- Blaabjerg, F.; Ionel, D.M. Renewable Energy Devices and Systems: State-of-the-Art Technology, Research and Development, Challenges and Future Trends. Electr. Power Componen. Syst. 2015, 43, 1319–1328. [Google Scholar] [CrossRef]

- Burger, S.P.; Luke, M. Business Models for Distributed Energy Resources: A Review and Empirical Analysis. Energy Policy 2017, 109, 230–248. [Google Scholar] [CrossRef]

- Giehl, J.; Göcke, H.; Grosse, B.; Kochems, J.; Müller-Kirchenbauer, J. Survey and Classification of Business Models for the Energy Transformation. Energies 2020, 13, 2981. [Google Scholar] [CrossRef]

- Weiller, C.M.; Pollitt, M.G. Platform markets and energy services. Camb. Work. Pap. Econ. 2013, 1361, 1–38. [Google Scholar]

- Smith, P.R.; Chaffey, D. EMarketing EXcellence; Routledge: London, UK, 2001; ISBN 978-0-08-050489-6. [Google Scholar]

- Best Revenue Model for Startups|Business Model in 2020. Available online: https://startuptalky.com/best-revenue-model-startups/ (accessed on 8 March 2022).

- Merchant, E.F. ‘Largest Ever’: Google Announces 1.6 GW of Renewables Purchases. Available online: https://www.greentechmedia.com/articles/read/google-announces-1600-megawatt-in-renewables-purchases (accessed on 28 January 2022).

- Achieving 100 Percent Renewable Energy with 24/7 Monitoring in Microsoft Sweden. Available online: https://azure.microsoft.com/en-us/blog/achieving-100-percent-renewable-energy-with-247-monitoring-in-microsoft-sweden/ (accessed on 26 January 2022).

- Apple Now Globally Powered by 100 Percent Renewable Energy. Available online: https://www.apple.com/pl/newsroom/2018/04/apple-now-globally-powered-by-100-percent-renewable-energy/ (accessed on 26 January 2022).

- Facebook Signs First Deal to Buy Renewable Energy in India. Available online: https://www.livemint.com/companies/news/facebook-signs-first-deal-to-buy-renewable-energy-in-india-11618470952508.html (accessed on 26 January 2022).

- Sylwia, T. Facebook Announced Nearly 1 GW in New Renewable Contracts. Available online: https://pv-magazine-usa.com/2020/08/10/facebook-announced-nearly-1-gw-in-new-renewable-contracts/ (accessed on 26 January 2022).

- 24/7 Clean Energy—Data Centers—Google. Available online: https://www.google.com/about/datacenters/cleanenergy/ (accessed on 28 January 2022).

- Katz, J. Building the Renewable Energy Industry—Google. Available online: //www.google.com/intl/en-GB/stories/renewable-energy-is-boosting-economies/ (accessed on 28 January 2022).

- IEA. World Energy Investment 2021 Datafile-Data Product. Available online: https://www.iea.org/data-and-statistics/data-product/world-energy-investment-2021-datafile (accessed on 1 February 2022).

- Lueth, K.L. State of the IoT 2020: 12 Billion IoT Connections, Surpassing Non-IoT for the First Time. IoT Anal. 2020. Available online: https://iot-analytics.com/state-of-the-iot-2020-12-billion-iot-connections-surpassing-non-iot-for-the-first-time/ (accessed on 1 February 2022).

- A World Finance Report: Technological Advances in Renewable Energy. Available online: http://reports.worldfinance.com/technological-advances-in-renewable-energy/ (accessed on 31 January 2022).

- Liu, H.; Yao, P.; Latif, S.; Aslam, S.; Iqbal, N. Impact of Green Financing, FinTech, and Financial Inclusion on Energy Efficiency. Environ. Sci. Pollut. Res. 2022, 29, 18955–18966. [Google Scholar] [CrossRef] [PubMed]

- Staff, A. Amazon Is Making Big Global Investments in Renewable Energy. Available online: https://www.aboutamazon.com/news/sustainability/amazon-is-making-big-global-investments-in-renewable-energy (accessed on 26 January 2022).

- Dóci, G.; Vasileiadou, E.; Petersen, A.C. Exploring the Transition Potential of Renewable Energy Communities. Futures 2015, 66, 85–95. [Google Scholar] [CrossRef] [Green Version]

- Denholm, P.; Mai, T. Timescales of Energy Storage Needed for Reducing Renewable Energy Curtailment. Renew. Energy 2019, 130, 388–399. [Google Scholar] [CrossRef]

- Dai, L.; Sun, S.; Li, T.; Gholami Farkoush, S. Probabilistic Model for Nondispatchable Power Resource Integration with Microgrid and Participation in the Power Market. Energy Strat. Rev. 2021, 33, 100611. [Google Scholar] [CrossRef]

- IRENA. Renewable Capacity Statistics 2021. Available online: https://www.irena.org/publications/2021/March/Renewable-Capacity-Statistics-2021 (accessed on 19 January 2022).

- Battery Pack Prices Fall to an Average of $132/KWh, But Rising Commodity Prices Start to Bite. Available online: https://about.bnef.com/blog/battery-pack-prices-fall-to-an-average-of-132-kwh-but-rising-commodity-prices-start-to-bite/ (accessed on 19 January 2022).

- Hittinger, E.S.; Azevedo, I.M.L. Bulk Energy Storage Increases United States Electricity System Emissions. Environ. Sci. Technol. 2015, 49, 3203–3210. [Google Scholar] [CrossRef]

- BCG. Digital for Renewable Energy Companies. Available online: https://www.bcg.com/industries/energy/center-digital-transformation-power-utilities/digital-for-renewable-energy-companies (accessed on 18 January 2022).

- Mirzaei, M.A.; Yazdankhah, A.S.; Mohammadi-Ivatloo, B.; Marzband, M.; Shafie-khah, M.; Catalão, J.P.S. Stochastic Network-Constrained Co-Optimization of Energy and Reserve Products in Renewable Energy Integrated Power and Gas Networks with Energy Storage System. J. Clean. Product. 2019, 223, 747–758. [Google Scholar] [CrossRef] [Green Version]

- EY. Why Artificial Intelligence Is a Game-Changer for Renewable Energy. Available online: https://www.ey.com/en_gl/power-utilities/why-artificial-intelligence-is-a-game-changer-for-renewable-energy (accessed on 24 January 2022).

- Grisales-Noreña, L.F.; Montoya, O.D.; Ramos-Paja, C.A. An Energy Management System for Optimal Operation of BSS in DC Distributed Generation Environments Based on a Parallel PSO Algorithm. J. Energy Stor. 2020, 29, 101488. [Google Scholar] [CrossRef]

- StartUs. How Augmented Reality Startups Transform The Energy Industry. Available online: https://www.startus-insights.com/innovators-guide/how-augmented-reality-startups-transform-the-energy-industry/ (accessed on 25 January 2022).

- Duch-Brown, N.; Rossetti, F. Digital Platforms across the European Regional Energy Markets. Energy Policy 2020, 144, 111612. [Google Scholar] [CrossRef]

- Niyazov, S. AI-Powered Monopolies and the New World Order. Available online: https://towardsdatascience.com/ai-powered-monopolies-and-the-new-world-order-1c56cfc76e7d (accessed on 30 January 2022).

- Apergis, N.; Sorros, J. The Role of R&D Expenses for Profitability: Evidence from U.S. Fossil and Renewable Energy Firms. Inter. J. Econ. Financ. 2014, 6, 8–15. [Google Scholar] [CrossRef] [Green Version]

- Vetter, D. Big Tech’s Renewable Energy Spend: Is This ‘Greenspinning’? Available online: https://www.forbes.com/sites/davidrvetter/2019/10/27/big-techs-renewable-energy-spend-is-this-greenspinning/?sh=34608a06259f (accessed on 30 January 2022).

- Fareed, Z.; Ali, Z.; Shahzad, F.; Nazir, M.I.; Ullah, A. Determinants of Profitability: Evidence from Power and Energy Sector. Stud. Univer. Babe-Bolyai Oeconom. 2016, 61, 59. [Google Scholar] [CrossRef] [Green Version]

- Amazon Is Europe’s Largest Corporate Renewable Energy Buyer. Available online: https://press.aboutamazon.com/news-releases/news-release-details/amazon-becomes-europes-largest-corporate-buyer-renewable-energy (accessed on 30 January 2022).

- Facebook Makes First Direct Investment in Renewable Energy Project. Available online: https://ieefa.org/facebook-makes-first-direct-investment-in-renewable-energy-project/ (accessed on 28 January 2022).

- Mechant, F.M. Google Promises $150 M for Renewables to Green Manufacturing Footprint. Available online: https://www.greentechmedia.com/articles/read/google-promises-150-million-renewables-investment-to-bolster-global-manufac (accessed on 28 January 2022).

- Holbroock, E. Apple Supply Chain Emissions: Suppliers Turn to Renewables. Available online: https://www.environmentalleader.com/2021/03/more-than-100-of-apples-global-suppliers-are-moving-to-100-renewable-energy/ (accessed on 28 January 2022).

- Apple’s Renewable Energy Journey. Available online: https://www.there100.org/our-work/news/apples-renewable-energy-journey (accessed on 28 January 2022).

- Epstein, A. The Truth About Apple’s “100% Renewable” Energy Usage. Forebes, 8 January 2016. Available online: https://www.forbes.com/sites/alexepstein/2016/01/08/the-truth-about-apples-100-renewable-energy-usage/ (accessed on 28 January 2022).

- Mytton, D. How Green Is Your Cloud? Available online: https://www.infoworld.com/article/3015632/how-green-is-your-cloud.html (accessed on 29 January 2022).

- IEA. A New Energy Economy Is Emerging–World Energy Outlook 2021–Analysis. Available online: https://www.iea.org/reports/world-energy-outlook-2021/a-new-energy-economy-is-emerging (accessed on 1 February 2022).

- AWS Energy. Available online: https://aws.amazon.com/energy/ (accessed on 26 January 2022).

- Prado, T.S.; Bauer, J.M. Effects of Big Tech Acquisitions on Start-up Funding and Innovation. Quello Cent. Work. Pap. 2021, 4. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3787127 (accessed on 1 February 2022).

- UNCTAD. The New Digital Economy and Development; UNCTAD Technical Note No 8; UNCTAD: New York, NY, USA, 2017. [Google Scholar]

- Vara, V. US Tech Giants to Lead Renewable Energy Business in the next Five to Ten Years: Poll. Power Technology, 24 May 2021. Available online: https://www.power-technology.com/news/us-tech-giants-to-lead-renewable-energy-business-in-the-next-five-to-ten-years-poll/ (accessed on 1 February 2022).

- Markard, J. The next Phase of the Energy Transition and Its Implications for Research and Policy. Nat. Energy 2018, 3, 628–633. [Google Scholar] [CrossRef]

- Turnheim, B.; Wesseling, J.; Truffer, B.; Rohracher, H.; Carvalho, L.; Binder, C. Challenges Ahead: Understanding, Assessing, Anticipating and Governing Foreseeable Societal Tensions to Support Accelerated Low-Carbon Transitions in Europe. In Advancing Energy Policy: Lessons on the Integration of Social Sciences and Humanities; Foulds, C., Robison, R., Eds.; Springer International Publishing: Cham, Switzerland, 2018; pp. 145–161. ISBN 978-3-319-99097-2. [Google Scholar]

- Bürer, M.; de Lapparent, M.; Capezzali, M.; Carpita, M. Governance Drivers and Barriers for Business Model Transformation in the Energy Sector. In Swiss Energy Governance; Hettich, P., Kachi, A., Eds.; Springer: Cham, Switzerland, 2022; pp. 195–243. [Google Scholar] [CrossRef]

Figure 1.

Data collection and selection model. ES—Energy storage, EP—energy providers, W—Wind, S—Solar.

Figure 1.

Data collection and selection model. ES—Energy storage, EP—energy providers, W—Wind, S—Solar.

Figure 2.

Global changes in the total renewable energy capacity by technology as compared to connected IoT.

Figure 2.

Global changes in the total renewable energy capacity by technology as compared to connected IoT.

Figure 3.

Electricity generation from renewable energy sources including pumped storage power plants.

Figure 3.

Electricity generation from renewable energy sources including pumped storage power plants.

Figure 4.

Technologies in power industry startups by energy sub-industry.

Figure 5.

Startups in solar energy by technology and sub-industry in January 2022. Source: dealroom data-based study.

Figure 5.

Startups in solar energy by technology and sub-industry in January 2022. Source: dealroom data-based study.

Figure 6.

Startups dealing with wind energy by technology and sub-industry in January 2022.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Energy startups applying at least one technology (Emerging Technology) by sub-industry.

| Industry | Number of Startups | Energy | CE | EF | ES | EP |

|---|---|---|---|---|---|---|

| RES (ET) | 386 | 221 | 94 | 21 | 24 | |

| Solar (ET) | 312 | 171 | 73 | 19 | 23 | |

| Wind (ET) | 75 | 50 | 26 | 1 | 3 | |

| Share | ||||||

| Total (ET) | in total | 6% | 13% | 25% | 24% | 8% |

| RES (ET) | in total using ET | 12% | 34% | 13% | 9% | 24% |

| in RES | 15% | 13% | 25% | 19% | 7% | |

| Solar (ET) | in RES using ET | 81% | 77% | 78% | 90% | 96% |

| in solar energy industry | 14% | 12% | 22% | 19% | 8% | |

| Wind (ET) | in RES using ET | 19% | 23% | 28% | 5% | 13% |

| in wind energy industry | 23% | 20% | 59% | 20% | 11% |

CE—Clean Energy, EE—Energy Efficiency, ES—Energy Storage, EP—Energy Providers, ET—using Emerging Technology.

Table 2.

Energy startups in the energy storage and energy providers industries in which G-MAFIA has invested (accessed on 2 March 2022 [18]).

Table 2.

Energy startups in the energy storage and energy providers industries in which G-MAFIA has invested (accessed on 2 March 2022 [18]).

| Startup | Key | Value |

|---|---|---|

| Emerging technologies: | deep tech |

| Income streams: | N.A. | |

| Client focus: | B2B | |

| Business model: | manufacturing | |

| Industry: | energy | |

| Amogy | Sub-industry: | energy storage transportation mobility |

| HQ: New York, NY, USA | Launch year: | 2021 |

| Website: https://www.amogy.co/ | Employees: | 11–50 |

| Valuation: | $77—116 m | |

| Investor: Amazon | Funding: | $19.3 m |

| Innovative Clean Energy Solution using Ammonia as a Fuel. | ||

| Emerging technologies: | - |

| Income streams: | commission | |

| Client focus: | B2B | |

| Business model: | manufacturing | |

| Industry: | energy | |

| Resilient Power Systems | Sub-industry: | energy providers transportation mobility clean energy |

| HQ: Atlanta, GA, USA | Launch year: | 2015 |

| Website: http://resilientpower.com | Employees: | N.A. |

| Valuation: | $20—30 m | |

| Investor: Amazon | Funding: | $5.0 m |

| Introducing the latest in solid-state technology, radically streamlining access to the power grid for visionary companies leading the EV fleet revolution. | ||

| Emerging technologies: | - |

| Income streams: | commission | |

| Client focus: | B2B | |

| Business model: | manufacturing | |

| Industry: | energy | |

| Redwood Materials | Sub-industry: | energy storage waste solution |

| HQ: Carson City, NV, USA | Launch year: | 2017 |

| Website: https://www.redwoodmaterials.com/ | Employees: | 51–200 |

| Valuation: | $3.7 b | |

| Investor: Amazon | Funding: | $792 m |

| Providing advanced technology and process development services for materials recycling, re-manufacturing, and reuse. | ||

| Emerging technologies: | - |

| Income streams: | commission | |

| Client focus: | B2B | |

| Business model: | manufacturing | |

| Industry: | energy | |

| ION Energy | Sub-industry: | energy storage energy efficiency |

| HQ: Mumbai, Maharashtra, India | Launch year: | 2017 |

| Website: http://ionenergy.co | Employees: | 50–200 |

| Valuation: | $14–22 m | |

| Investor: Amazon | Funding: | $4.8 m |

| An advanced battery management and intelligence platform focused on building technologies that improve the life and performance of lithium-ion batteries that power electric vehicles and energy storage systems. | ||

| Emerging technologies: | IoT deep tech |

| Income streams: | subscription | |

| Client focus: | B2 C | |

| Business model: | manufacturing | |

| Industry: | energy | |

| BuffaloGrid | Sub-industry: | energy storage clean energy solar energy telecom |

| HQ: Belfast, Northern Ireland | Launch year: | 2011 |

| Website: https://www.buffalogrid.com/ | Employees: | 11–50 |

| Valuation: | $17–25 m | |

| Investor: Microsoft | Funding: | $9.1 m |

| Our solar-powered technology makes phone charging and internet services available to all. | ||

| Emerging technologies: | deep tech |

| Income streams: | N.A. | |

| Client focus: | B2B | |

| Business model: | manufacturing | |

| Industry: | energy | |

| Twelve | Sub-industry: | energy storage |

| HQ: Berkeley, CA, USA | Launch year: | 2021 |

| Employees: | 51–200 | |

| Valuation: | $228–342 m | |

| Investor: Microsoft | Funding: | $60.4 m |

| Captures carbon emissions where pollution is generated and turns the CO2 into chemicals like methane, ethylene, and ethanol. | ||

| Emerging technologies: | deep tech |

| Income streams: | commission | |

| Client focus: | B2B | |

| Business model: | manufacturing | |

| Industry: | energy | |

| PowerbyProxi | Sub-industry: | energy providers |

| HQ: Auckland, New Zealand | Launch year: | 2007 |

| Website: https://www.amogy.co/ | Employees: | 11–50 |

| Valuation: | $16–24 m | |

| Investor: Apple | Funding: | $9 m |

| Offering wireless power solutions for consumer electronics and industrial applications. | ||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Pakulska, T.; Poniatowska-Jaksch, M. Digitalization in the Renewable Energy Sector—New Market Players. Energies 2022, 15, 4714. https://doi.org/10.3390/en15134714

AMA Style

Pakulska T, Poniatowska-Jaksch M. Digitalization in the Renewable Energy Sector—New Market Players. Energies. 2022; 15(13):4714. https://doi.org/10.3390/en15134714

Chicago/Turabian StylePakulska, Teresa, and Małgorzata Poniatowska-Jaksch. 2022. "Digitalization in the Renewable Energy Sector—New Market Players" Energies 15, no. 13: 4714. https://doi.org/10.3390/en15134714

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.