Can the SOM Analysis Predict Business Failure Using Capital Structure Theory? Evidence from the Subprime Crisis in Spain

Abstract

:1. Introduction

2. Theoretical Framework

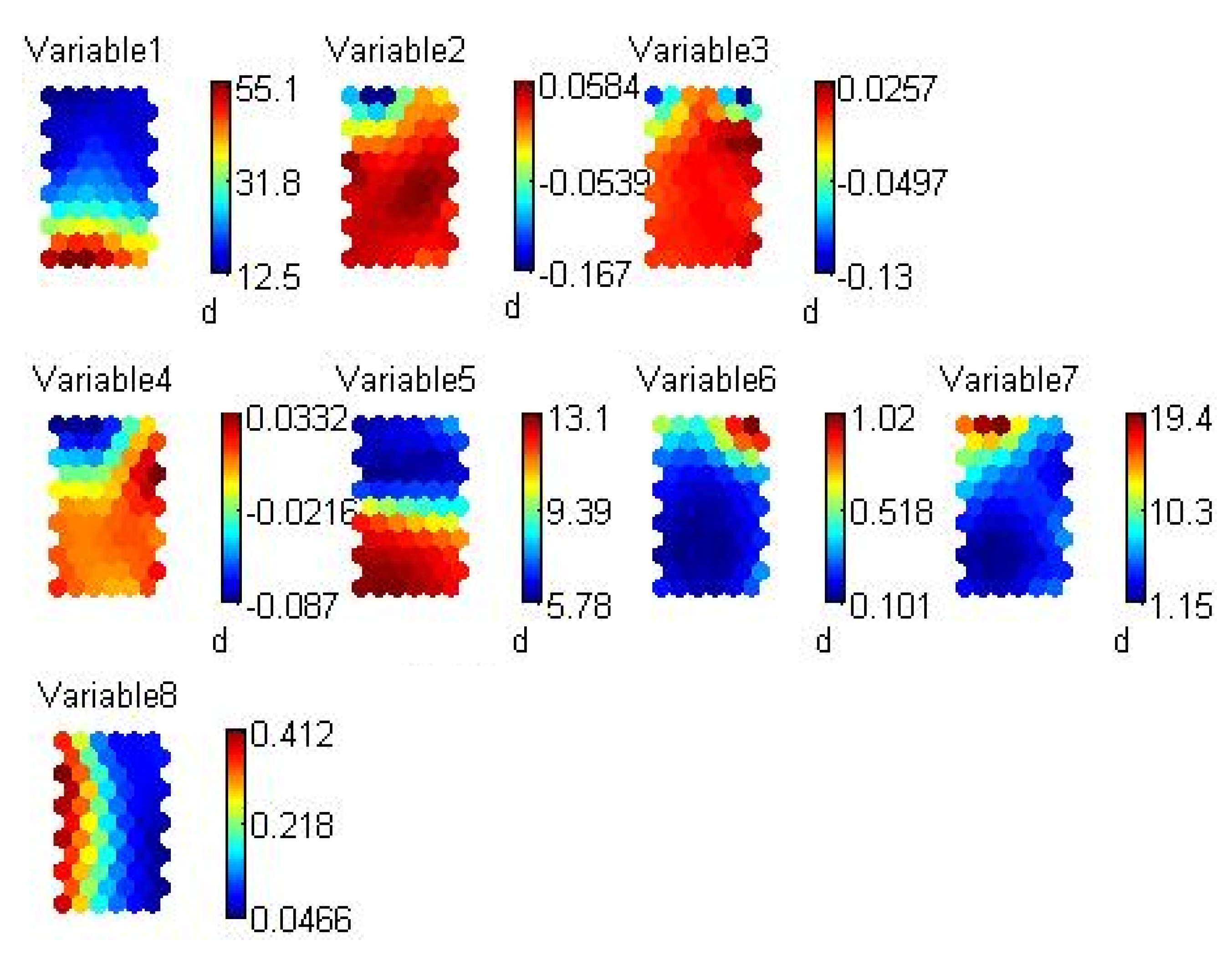

- Profitability: According to [25,26] the firms prefer to use internal resources to finance operations; in other words, more profitability is linked with cash flows, so the firms no need external debt to finance their investments. Therefore, there is a negative relation between profitability and leverage. However, [22] found the opposite statement, confirming that exists a positive relation because of the most profitable firms can take more debt, given the advantages of taxes. In this study profitability is measured though EBIT (earnings before interest and taxes) over assets taken as references [34,35,36,37], among others. Another measure of profitability is EBITDA (earnings before interest taxes depreciation and amortization) over assets. Thus, the following hypothesis was formulated:H1.Higher Profits (EBIT over Assets) Reduce Default Probability.

- Growth opportunities: On the one hand, the operating earnings’ variability and the variation of total assets can be used as measures of growth potential. In the case of earnings, some authors suggest that firms with more variations in sales have more possibilities of growth [21,30,38] and firms with more investments have more potential for growth [21,37,39]. According to the pecking order theory, a positive relationship is expected between leverage and growth opportunities. One study [40] suggested a positive relationship between the growth and the firm’s age because companies need more external financing when they are young. On the other hand, there are other indicators used in the literature to measure growth opportunities, such as market to book ratio and Tobin’s Q. Thus, the following statement was formulated:H2.A higher Variation in the Total Assets Decreases the Possibility of Bankruptcy.

- Size: According to the trade-off theory, firm size is positively related with external financing, but some empirical evidence shows a negative relationship with leverage. The positive relation is associated with reputation and information asymmetries that are smaller in large firms [40,41]. The size can be measured through the logarithm of total assets [30,34,37,39,41,42,43] or the logarithm of earnings ([29,30,35,38], among others). Thus, the following statement was formulated:H3.The Firm’s Size Decreases the Probability of Defaulting.

- Risk/Volatility: The pecking order theory and the trade-off theory argue that more risk is associated with less leverage. The risk can be measured through the standard deviation of ROA, that of EBIT, and/or the standard deviation of earnings ([36,39,42], among others). Thus, the following statement was formulated:H4.More Volatility Increases the Probability of Defaulting.

- Tangibility: This variable shows the proportion of fixed assets in the firm [25,30,35,36,38,42,43]. The literature review showed that companies with high proportions of fixed assets over total assets present more leverage because fixed assets can be used as guaranties. On the other hand, guaranties reduce agency problems and cost of default [35]. Thus, the following statement was formulated:H5.Higher Tangibility (Fixed Assets over Total Assets) Decreases Default Probability.

- Age: A Firm’s age can be measured as the logarithm of the number of years of business operation, following [35,44]. It also can be measured by the number of years since the firm’s founding [29,38]. On the other hand, authors such as [40] use a size–age index, a linear combination of firm size and age. The pecking order theory predicts a negative relationship between age and debt, arguing that the years of operation of business help the firm to accumulate retained earnings and generate internal resources over time, thereby minimizing the need for external finance. Thus, the following statement was formulated:H6.The Probability of Defaulting is Reduced with the Age of the Firms.

3. Methodology: Self-Organizing Maps

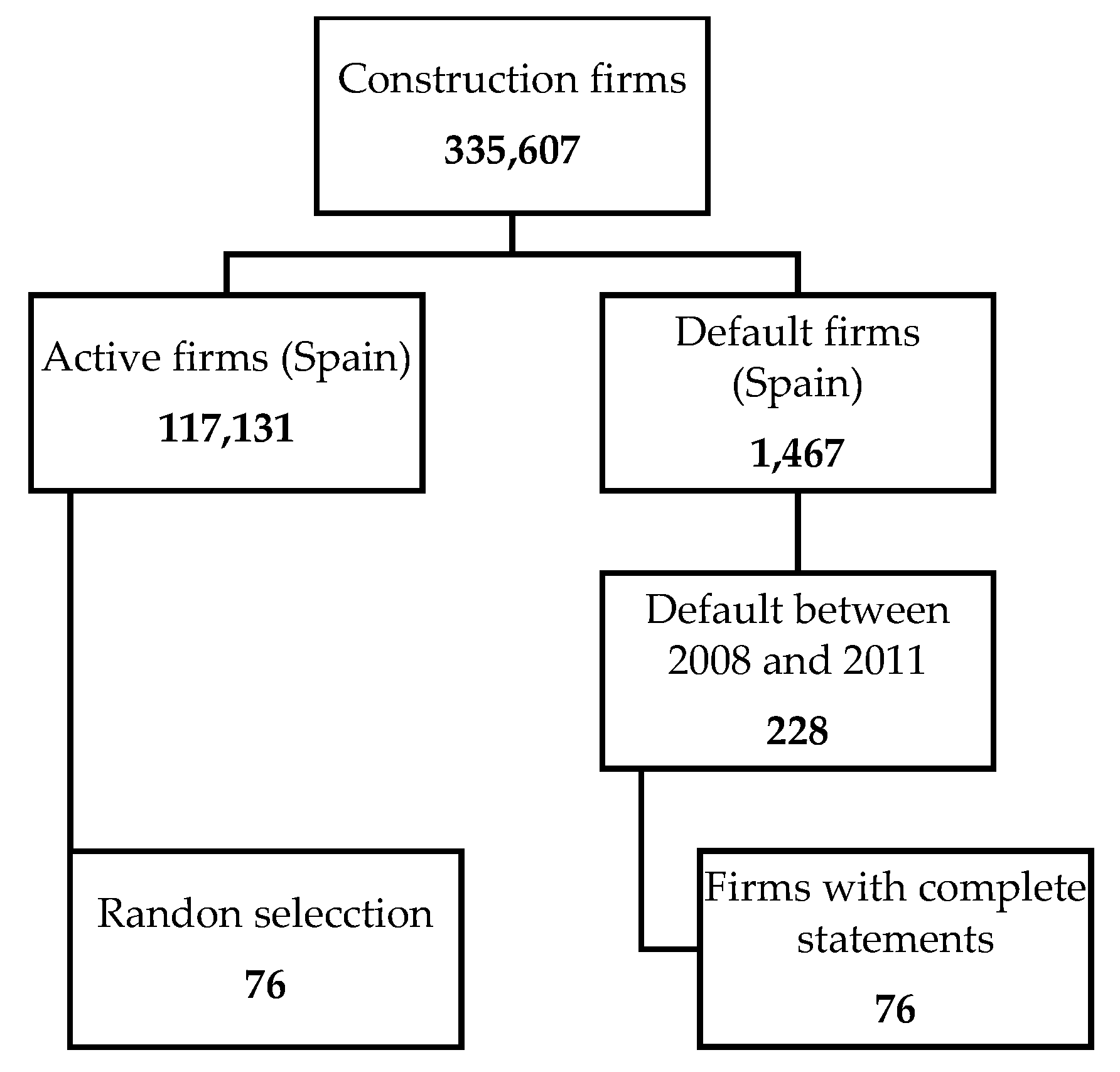

4. Data and Variables Selection

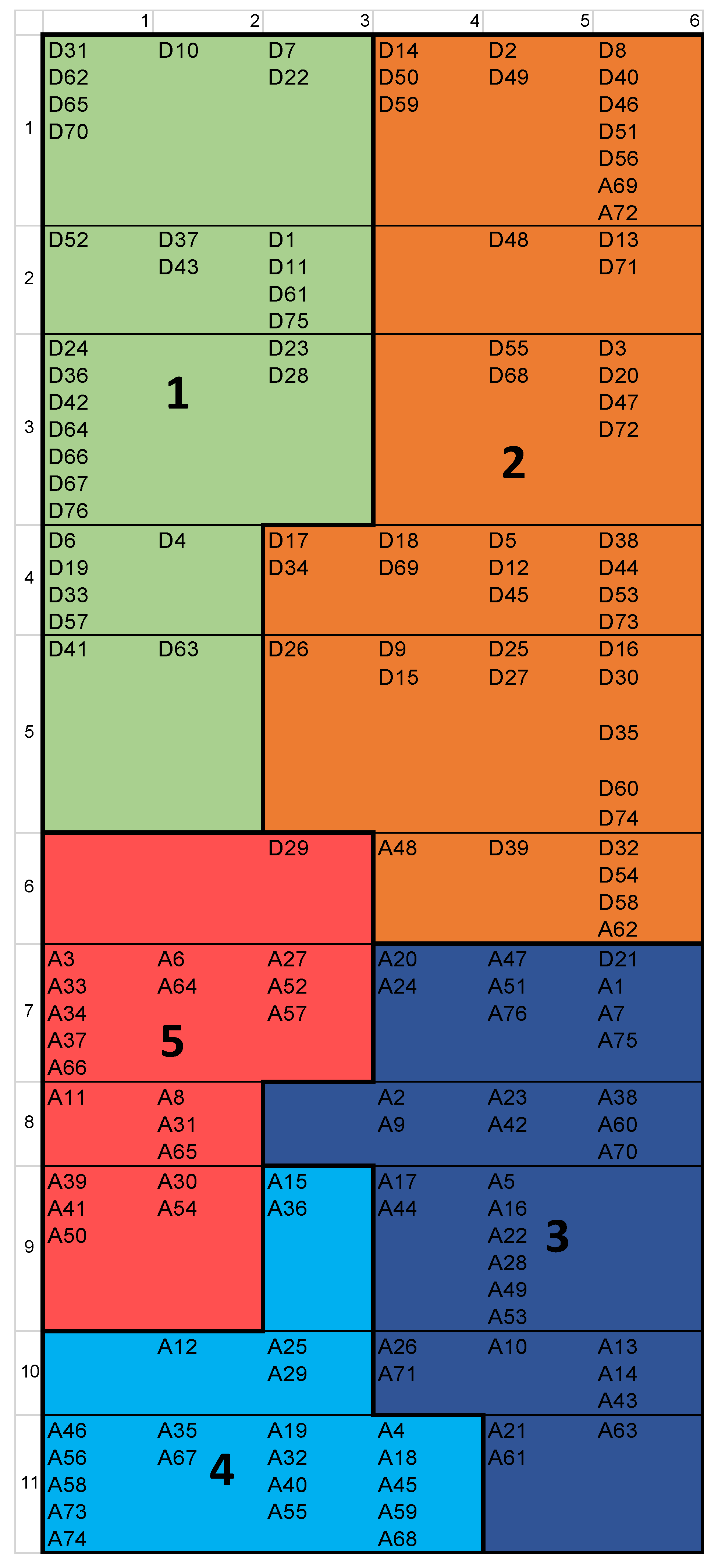

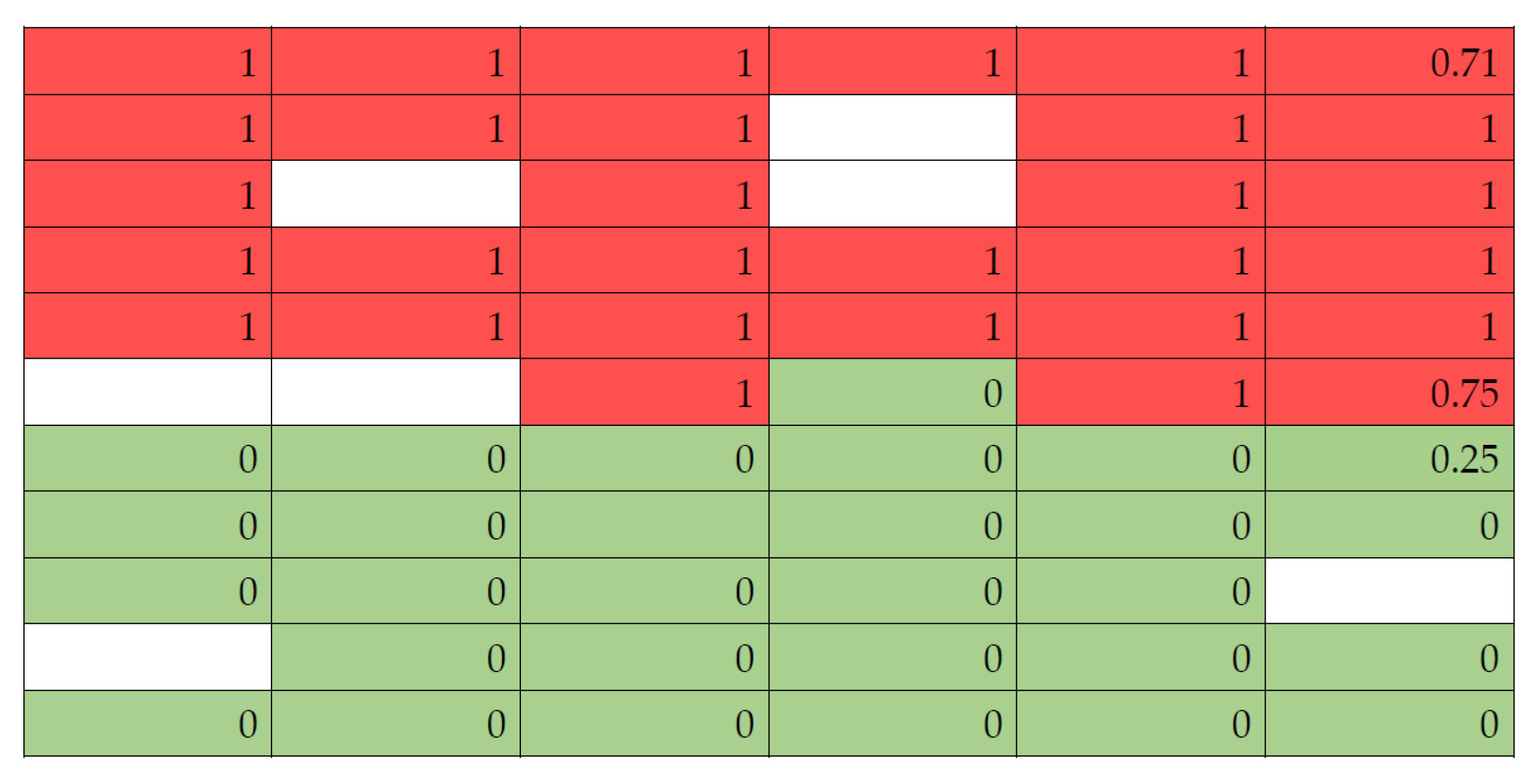

5. Application

6. Discussion and Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Beaver, W.H. Financial ratios as predictors of failure. J. Account. Res. 1966, 4, 71–111. [Google Scholar] [CrossRef]

- Altman, E.I. Financial ratios, discriminant analysis and the prediction of corporate bankruptcy. J. Financ. 1968, 23, 589–609. [Google Scholar] [CrossRef]

- Balcaen, S.; Ooghe, H. 35 years of studies on business failure: An overview of the classic statistical methodologies and their related problems. Br. Account. Rev. 2006, 38, 63–93. [Google Scholar] [CrossRef]

- Kumar, P.R.; Ravi, V. Bankruptcy prediction in banks and firms via statistical and intelligent techniques: A review. Eur. J. Oper. Res. 2007, 180, 1–28. [Google Scholar] [CrossRef]

- Bahrammirzaee, A. A comparative survey of artificial intelligence applications in finance: Artificial neural networks, expert systems and hybrid intelligent systems. Neural Comput. Appl. 2010, 19, 1165–1195. [Google Scholar] [CrossRef]

- Sun, J.; Li, H.; Huang, Q.H.; He, K.Y. Predicting financial distress and corporate failure: A review from the state of the art definitions, modeling, sampling, and featuring approaches. Knowl. Based Syst. 2014, 57, 41–56. [Google Scholar] [CrossRef]

- Appiah, K.O.; Chizema, A.; Arthur, J. Predicting corporate failure: A systematic literature review of methodological issues. Int. J. Law Manag. 2015, 57, 461–485. [Google Scholar] [CrossRef]

- Alaka, H.A.; Oyedele, L.O.; Owolabi, H.A.; Kumar, V.; Ajayi, S.O.; Akinade, O.O.; Bilal, M. Systematic review of bankruptcy prediction models: Towards a framework for tool selection. Expert Syst. Appl. 2018, 94, 164–184. [Google Scholar] [CrossRef]

- Scherger, V.; Terceño, A.; Vigier, H. A systematic overview of the prediction of business failure. Int. J. Technol. Policy Manag. 2019, 19, 196–211. [Google Scholar] [CrossRef]

- Vigier, H.; Scherger, V.; Terceño, A. An application of OWA operators in fuzzy business diagnosis. Appl. Soft. Comput. 2017, 54, 440–448. [Google Scholar] [CrossRef]

- Scherger, V.; Terceño, A.; Vigier, H. The OWA distance operator and its application in business failure. Kybernetes 2017, 46, 114–130. [Google Scholar] [CrossRef]

- Terceño, A.; Vigier, H.; Scherger, V. Prediction of business failure with fuzzy models. Int. J. Uncertain. Fuzziness Knowl. Based Syst. 2018, 26, 21–38. [Google Scholar] [CrossRef]

- Hu, C.K.; Liu, F.B.; Hu, C.F. A set covering-based diagnostic expert system to economic and financial applications. Int. J. Uncertain. Fuzziness Knowl. Based Syst. 2016, 24, 91–107. [Google Scholar] [CrossRef]

- Scarlat, E.; Delcea, C. Complete analysis of bankruptcy syndrome using grey systems theory. Grey Syst. Theory Appl. 2011, 1, 19–32. [Google Scholar]

- Scherger, V.; Terceño, A.; Vigier, H.; Barberá-Mariné, M.G. Detection and assessment of causes in business diagnosis. Econ. Comp. Econ. Cybern. Stud. Res. 2015, 49, 211–229. [Google Scholar]

- Tseng, F.M.; Hu, Y.C. Comparing four bankruptcy prediction models: Logit, quadratic interval logit, neural and fuzzy neural networks. Expert Syst. Appl. 2010, 37, 1846–1853. [Google Scholar] [CrossRef]

- Odom, M.D.; Sharda, R. A neural network model for bankruptcy prediction. In Proceedings of International Joint Conference on Neural Networks; IEEE: San Diego, CA, USA, 1990; pp. 163–168. [Google Scholar]

- Modigliani, F.; Miller, M.H. The cost of capital, corporation finance and the theory of investment. American 1958, 48, 261–297. [Google Scholar]

- Martinez, L.B.; Scherger, V.; Guercio, M.B. SMEs capital structure: Trade-off or pecking order theory: A systematic review. J. Small Bus. Enterp. Dev. 2018, 26, 105–132. [Google Scholar] [CrossRef]

- Ardalan, K. Capital structure theory: Reconsidered. Res. Int. Bus. Financ. 2017, 39, 696–710. [Google Scholar] [CrossRef]

- Camara-Turull, X.; Fernández-Izquierdo, M.A.; Sorrosal-Forradellas, M.T. Analysing capital structure of spanish chemical companies using self-organizing maps. Kybernetes 2017, 46, 947–965. [Google Scholar] [CrossRef]

- Modigliani, F.; Miller, M.H. Corporate Income Taxes and the Cost of Capital: A Correction. Am. Econ. Rev. 1963, 53, 433–443. [Google Scholar]

- Stiglitz, J.E. A re-examination of the Modigliani-Miller theorem. Am. Econ. Rev. 1969, 59, 784–793. [Google Scholar]

- Fama, E.F. The effects of a firm’s investment and financing decisions on the welfare of its security holders. Am. Econ. Rev. 1978, 68, 272–284. [Google Scholar]

- Myers, S.C. The capital structure puzzle. J. Financ. 1984, 39, 574–592. [Google Scholar] [CrossRef]

- Myers, S.C.; Majluf, N.S. Corporate financing and investment decisions when firms have information that investors do not have. J. Financ. Econ. 1984, 13, 187–221. [Google Scholar] [CrossRef] [Green Version]

- Berger, A.N.; Udell, G.F. The economics of small business finance: The roles of private equity and debt markets in the financial growth cycle. J. Bank. Financ. 1998, 22, 613–673. [Google Scholar] [CrossRef] [Green Version]

- Briozzo, A.; Vigier, H. A demand-side approach to SMES’ capital structure: Evidence from Argentina. J. Bus. Entrep. 2009, 21, 30–56. [Google Scholar]

- Alves, P.; Francisco, P. The impact of institutional environment on the capital structure of firms during recent financial crises. Q. Rev. Econ. Financ. 2015, 57, 129–146. [Google Scholar] [CrossRef]

- Daskalakis, N.; Balios, D.; Dalla, V. The behaviour of SMEs’ capital structure determinants in different macroeconomic states. J. Corp. Financ. 2017, 46, 248–260. [Google Scholar] [CrossRef]

- Balios, D.; Eriotis, N.; Fragoudaki, A.; Giokas, D. Economic efficiency of Greek retail SMEs in a period of high fluctuations in economic activity: A DEA approach. Appl. Econ. 2015, 47, 3577–3593. [Google Scholar] [CrossRef]

- Van Hoang, T.H.; Gurău, C.; Lahiani, A.; Seran, T.L. Do crises impact capital structure? A study of French micro-enterprises. Small Bus. Econ. 2018, 50, 181–199. [Google Scholar]

- Zeitun, R.; Temimi, A.; Mimouni, K. Do financial crises alter the dynamics of corporate capital structure? Evidence from GCC countries. Q. Rev. Econ. Financ. 2017, 63, 21–33. [Google Scholar] [CrossRef]

- Crespí, R.; Martín-Oliver, A. Do family firms have better access to external finance during crises? Corp. Gov. Int. Rev. 2015, 23, 249–265. [Google Scholar] [CrossRef]

- Dasilas, A.; Papasyriopoulos, N. Corporate governance, credit ratings and the capital structure of Greek SME and large listed firms. Small Bus. Econ. 2015, 45, 215–244. [Google Scholar] [CrossRef]

- Ebrahim, M.S.; Girma, S.; Shah, M.E.; Williams, J. Dynamic capital structure and political patronage: The case of Malaysia. Int. Rev. Financ. Anal. 2014, 31, 117–128. [Google Scholar] [CrossRef] [Green Version]

- Kim, H.; Heshmati, A.; Aoun, D. Dynamics of capital structure: The case of Korean listed manufacturing companies. Asian Econ. J. 2006, 20, 275–302. [Google Scholar] [CrossRef]

- Ramalho, J.J.; Rita, R.M.; Vidigal da Silva, J. The impact of family ownership on capital structure of firms: Exploring the role of zero-leverage, size, location and the global financial crisis. Int. Small Bus. J. Res. Entrep. 2018, 36, 574–604. [Google Scholar] [CrossRef] [Green Version]

- Mirza, S.S.; Jebran, K.; Yan, Y.; Iqbal, A. Financing behavior of firms in tranquil and crisis period: Evidence from China. Cogent Econ. Financ. 2017, 5. [Google Scholar] [CrossRef]

- Dang, V.A.; Kim, M.; Shin, Y. Asymmetric adjustment toward optimal capital structure: Evidence from a crisis. Int. Rev. Financ. Anal. 2014, 33, 226–242. [Google Scholar] [CrossRef]

- Hernández, C.G.; Ríos Bolivar, H.; Garrido Noguera, C. Determinantes microeconómicos del acceso al financiamiento externo de la estructura de capital de empresas del sector industrial. Contad. Y Adm. 2015, 60, 326–345. [Google Scholar] [CrossRef] [Green Version]

- Danso, A.; Adomako, S. The financing behaviour of firms and financial crisis. Manag. Financ. 2014, 40, 1159–1174. [Google Scholar] [CrossRef]

- Fernández, A.I.; González, F.; Suárez, N. Bank supply shocks and the substitution between bank and nonbank debt. J. Corp. Financ. 2017, 48, 122–147. [Google Scholar] [CrossRef]

- Kyriazopoulos, G. Corporate governance and capital structure in the periods of financial distress. Evidence from Greece. Invest. Manag. Financ. Innov. 2017, 14, 254–262. [Google Scholar] [CrossRef] [Green Version]

- Kohonen, T.K. Self-organized formation of topologically correct feature maps. Biol. Cybern. 1982, 4, 59–69. [Google Scholar] [CrossRef]

- Chen, N.; Ribeiro, B.; Vieira, A.; Chen, A. Clustering and visualization of bankruptcy trajectory using self-organizing map. Expert Syst. Appl. 2013, 40, 385–393. [Google Scholar] [CrossRef]

- Serrano-Cinca, C. Self organizing neural networks for financial diagnosis. Decis. Support Syst. 1996, 17, 227–238. [Google Scholar] [CrossRef]

- du Jardin, P. Bankruptcy prediction using terminal failure processes. Eur. J. Oper. Res. 2015, 242, 286–303. [Google Scholar] [CrossRef]

- Judge, A.; Korzhenitskaya, A. Credit market conditions and the impact of access to the public debt market on corporate leverage. Int. Rev. Financ. Anal. 2012, 25, 28–63. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Classification | Variable | Description | Expected Relationship |

|---|---|---|---|

| Age | Age (Var1) | Number of years elapsed between the firm creation and its insolvency situation or the end of the study period if the firm is still active. | (-) |

| Profitability | EBIT/A (Var2) | EBIT over assets | (-) |

| Growth opportunities | Var. earnings (Var3) | % change in ln of sales | (-) |

| Var. assets (Var4) | % change in ln of total assets | (-) | |

| Size | Assets (Var5) | Ln of assets | (-) |

| Earnings (Var6) | Ln of earnings | (-) | |

| Risk/Volatility | Std of earnings (Var7) | Standard deviation of ln of earnings | (+) |

| Std of ROA (Var8) | Standard deviation of EBIT over assets in 2008 (year) | (+) | |

| Tangibility | FA/A (Var9) | Fixed assets over assets | (-) |

| Minimum | Maximum | Mean | Standard Deviation | |

|---|---|---|---|---|

| A) Default companies | ||||

| Age | 7.64 | 34.01 | 15.29 | 6.12 |

| EBIT/A | −7.85 | 0.52 | −0.10 | 0.91 |

| Var. earnings | −1.18 | 0.65 | −0.03 | 0.20 |

| Var. assets | −0.28 | 0.11 | −0.02 | 0.06 |

| Assets | 0.00 | 10.35 | 6.18 | 2.20 |

| Earnings | −0.97 | 9.93 | 7.27 | 1.58 |

| Std. earnings | 0.01 | 4.51 | 0.48 | 0.64 |

| Std ROA | 0.00 | 569.15 | 13.59 | 65.32 |

| FA/A | 0.00 | 0.81 | 0.18 | 0.18 |

| B) Active companies | ||||

| Age | 12.12 | 112.99 | 36.69 | 20.91 |

| EBIT/A | −0.42 | 0.19 | 0.04 | 0.08 |

| Var. earnings | −0.15 | 0.11 | −0.00 | 0.04 |

| Var. assets | −0.04 | 0.08 | 0.01 | 0.02 |

| Assets | 9.30 | 15.53 | 12.19 | 1.40 |

| Earnings | 9.41 | 15.34 | 11.98 | 1.38 |

| Std. earnings | 0.00 | 1.23 | 0.18 | 0.23 |

| Std ROA | 0.01 | 37.75 | 3.34 | 5.74 |

| FA/A | 0.00 | 0.55 | 0.19 | 0.15 |

| 1 | 0.098 | 0.072 | 0.260 | 0.714 | 0.705 | −0.263 | −0.116 | 0.030 | |

| 0.098 | 1 | 0.050 | 0.490 | 0.083 | 0.101 | −0.001 | −0.991 | 0.046 | |

| 0.072 | 0.050 | 1 | 0.093 | 0.233 | 0.034 | −0.493 | −0.032 | −0.030 | |

| 0.260 | 0.490 | 0.093 | 1 | 0.291 | 0.247 | −0.120 | −0.504 | −0.113 | |

| 0.714 | 0.083 | 0.233 | 0.291 | 1 | 0.832 | −0.547 | −0.088 | 0.019 | |

| 0.705 | 0.101 | 0.034 | 0.247 | 0.832 | 1 | −0.246 | −0.117 | 0.012 | |

| −0.263 | −0.001 | −0.493 | −0.120 | −0.547 | −0.246 | 1 | −0.007 | −0.086 | |

| −0.116 | −0.991 | −0.032 | −0.504 | −0.088 | −0.117 | −0.007 | 1 | −0.043 | |

| 0.030 | 0.046 | −0.030 | −0.113 | 0.019 | 0.012 | −0.086 | −0.043 | 1 |

| Error (%) | Accuracy (%) | |

|---|---|---|

| Type I | 1.4 | 98.6 |

| Type II | 3.8 | 96.2 |

| Total error | 2.6 | 97.4 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Lucanera, J.P.; Fabregat-Aibar, L.; Scherger, V.; Vigier, H. Can the SOM Analysis Predict Business Failure Using Capital Structure Theory? Evidence from the Subprime Crisis in Spain. Axioms 2020, 9, 46. https://doi.org/10.3390/axioms9020046

Lucanera JP, Fabregat-Aibar L, Scherger V, Vigier H. Can the SOM Analysis Predict Business Failure Using Capital Structure Theory? Evidence from the Subprime Crisis in Spain. Axioms. 2020; 9(2):46. https://doi.org/10.3390/axioms9020046

Chicago/Turabian StyleLucanera, Juan Pedro, Laura Fabregat-Aibar, Valeria Scherger, and Hernán Vigier. 2020. "Can the SOM Analysis Predict Business Failure Using Capital Structure Theory? Evidence from the Subprime Crisis in Spain" Axioms 9, no. 2: 46. https://doi.org/10.3390/axioms9020046