The Impact of Women Power on Firm Value

ISEG Lisbon School of Economics & Management, Universidade de Lisboa & Advance/CSG, 1200-781 Lisboa, Portugal

*

Author to whom correspondence should be addressed.

Adm. Sci. 2022, 12(3), 93; https://doi.org/10.3390/admsci12030093

Submission received: 1 July 2022

/

Revised: 24 July 2022

/

Accepted: 27 July 2022

/

Published: 2 August 2022

(This article belongs to the Special Issue Gender, Relational Capital and Technology. Present State and Historical Perspectives in Business and Economics)

Abstract

:Companies have been encouraged by policy to place women on board and top management positions. Proposals from regulators and governance reforms explicitly stress the importance of gender diversity in the boardroom. This paper analyzes the impact of the presence of women in executive and non-executive positions, as Chairs, CEOs or CFOs, on firm value in the context of European public companies. The results suggest that the presence of women impacts firm value positively. The results also suggest that, in countries governed by women, firm values are higher. A further analysis provides evidence that, when women CEOs and Chairs are simultaneously shareholders, firm value is negatively impacted. In contrast, when a Chair changes from a man to a woman, firm value is positively impacted. This study contributes to the ongoing debate on whether appointing women to board positions and management positions has positive valuation effects, and it is of the interest to policymakers and investors, among others.

1. Introduction

According to data from the European Commission, in 2019, 73.3% of members belonging to the boards of directors (boards) of listed European companies are men. Only 6.7% of women hold the position of Chairperson (Chair), and 6.5% hold the position of chief executive officer (CEO). The underrepresentation of women in senior corporate positions has become a topic of interest in society, especially when the European Commission began to promote greater equality between men and women in the business environment. These efforts culminated in decisions to implement quota laws to ensure a greater representation of women, especially in state-owned and listed firms.

Firm performance may be affected by two roles related to boards: the monitoring role and the provision of resources role, highlighted by the resource dependence and stakeholder theory. In fact, boards have the most influence on a company’s strategic decision making and have a supervisory role that avoids less appropriate management practices and decisions.

Habib and Hossain (2013) present two reasons for the integration of women on boards: moral justice and business reasons. For the former, we can argue that society views the inclusion of women as a social issue, and, therefore, increasing the number of women is perceived as a goal to be achieved in a social context (Gonçalves et al. 2021). For the latter, board diversity is normally associated with new ideas, more debates, better communication, and new business management processes (Gaio and Gonçalves 2022), and, therefore, it can improve financial performance and enhance firm value. Adams and Ferreira (2009) state that a diversified board improves the monitoring of managers, allowing them to detect and avoid bad management practices. Because women bring unique and valuable skills to boards, board performance improves, which positively impacts firm value (Carter et al. 2003; Campbell and Mínguez-Vera 2008). Moreover, women directors on boards can provide a valuable form of legitimacy.

However, research on the impact of board diversity and firm value has provided mixed evidence. In particular, in terms of gender diversity, some studies have found a positive relationship between the presence of women on board, financial performance and firm value (Carter et al. 2003; Abdelzaher and Abdelzaher 2019; Campbell and Mínguez Vera 2010; Reguera-Alvarado et al. 2017), whereas others have found a negative relationship (Adams and Ferreira 2009; Shehata et al. 2017) or even no relationship at all (Jedi and Nayan 2018; Marinova et al. 2016).

Moreover, most of the studies analyze gender diversity in terms of women representation on Board. Indeed, the literature on the role of Chairs, CEOs or CFOs positions being held by women on firm value is still scarce and also provides mixed results. Peni (2014) reports a positive relationship between the presence of women CEOs or Chairs and firm performance, whereas Bennouri et al. (2018) find that women’s leadership in the board is negatively associated with firm value. Therefore, theoretical and empirical questions remain surrounding the relationship between gender diversity and firm value.

Adams et al. (2015) call for more international studies on the effects of gender diversity at Board level, since most studies focus on a single country. Indeed, there is a considerable variation across Europe regarding policies to promote gender diversity on Boards. Some countries have enforced mandatory quotas, others have only made recommendations, and still others have left it up to companies to set their own goals.

The proposal presented by European Commission in 2012 to increase women’s representation on Board to 40% by 2020 in publicly listed companies, through the introduction of gender quotas, is not only motivated by equity considerations, but also by business motives, since it is claimed that gender diversity is a driving force of performance. This raises the question of whether the increase of women representation on Board, as well as the positions of Chairs, CEOs, or CFOs being held by women, bring economic benefits to the company.

Therefore, this study aims to analyze the association between firm value and the presence of women on the Board, namely in non-executive positions (Chair) and executive positions, CEO and CFO, in the context of European listed firms. We also analyze the role that a country governed by a woman may play in these relationships, since there is evidence that political actors can drive changes in women representation on boards (Seierstad et al. 2017).

Following prior literature, firm value is measured by Tobin’s Q. Indeed, Tobin’s Q is considered the closest representation of firm value (Adams and Ferreira 2009; Carter et al. 2010; Isidro and Sobral 2015) and is the predominant measure used in corporate governance literature, mainly in that related to the impact of (gender) diversity (Marinova et al. 2016). Our sample comprises firms from 14 European countries and 15 different industries, covering the period between 2011 and 2018.

The results suggest that the presence of women on boards positively impacts firm value and that companies in countries governed by women have a higher market valuation. Additional analyses provide evidence that gender changes and the presence of women shareholders on boards have different impacts depending on the executive or non-executive position held by women.

This study contributes to the debate on whether appointing women to Board positions has positive valuation effects in several ways. Firstly, we attend Adams et al. (2015) call for more international studies on the effects of gender diversity on firm value, since most prior studies focus on a single country. Secondly, we analyze a dimension of gender diversity less study in the literature: the role of Chair, CEO, and CFO positions being held by women on firm value. Most studies focus on the percentage of women directors on the Board. Thirdly, as far as we know, our research is one of the first that studies whether the association between the presence of women and firm value is different in countries governed by women.

Our findings are of interest for policymakers and investors. The adaptation of quota laws for women on Boards has costs of implementation and enforcement. Therefore, it is important for European policymakers to understand whether the costs are offset by the potential benefits that can affect firm value. Results are also relevant to investors who value gender diversity in their investment decisions.

2. Literature Review

2.1. Gender Diversity in the Largest Companies of the EU14

The presence of women in executive and non-executive positions has become a subject of great social interest, and a significant increase in studies focusing on it in the business context has been observed. The various approaches and regulations that have emerged in order to promote gender equity, both in terms of representation and remuneration levels, represent the growing importance of this issue.

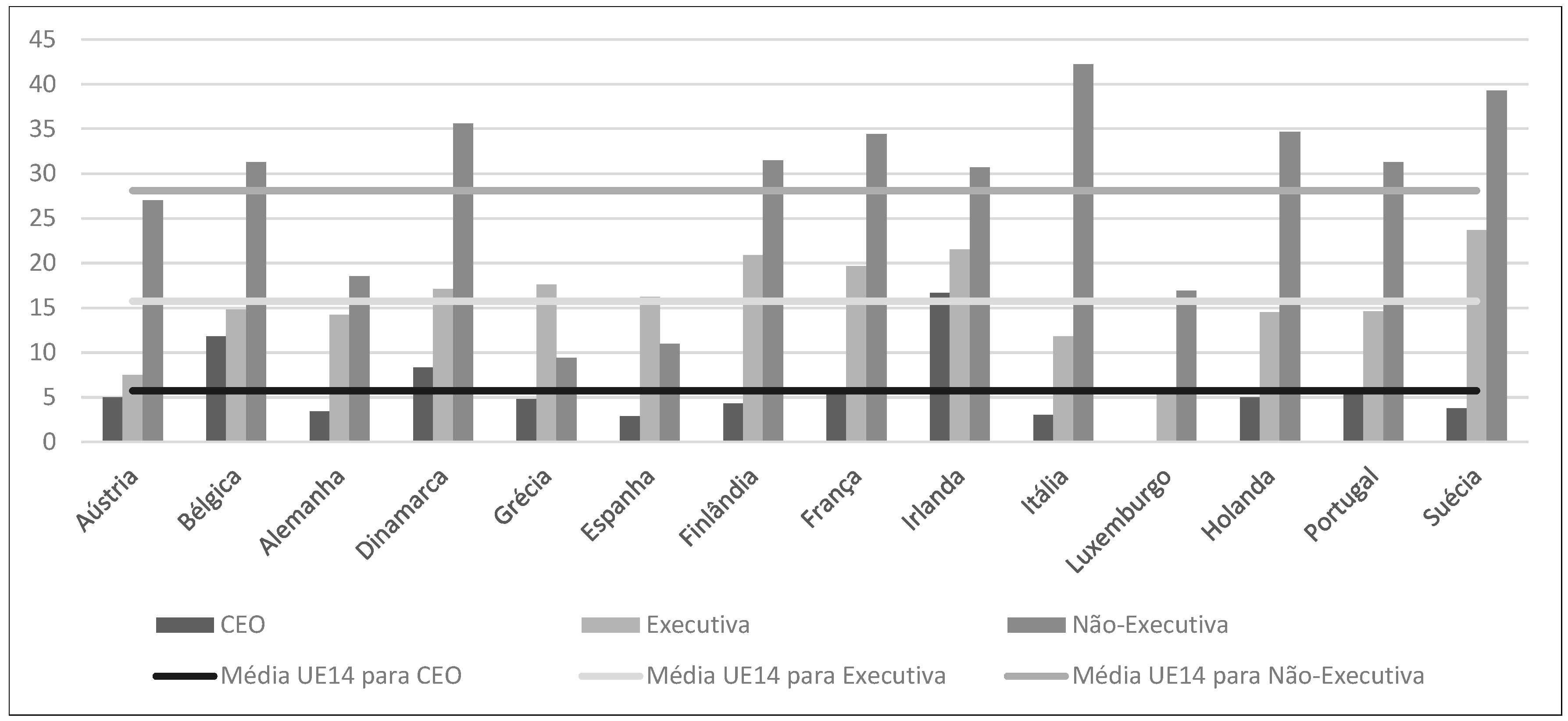

Considering the EU14 group (Germany, Austria, Belgium, Denmark, Spain, Finland, France, Greece, Holland, Ireland, Italy, Luxembourg, Portugal, and Sweden), we can analyze the women representation in companies in these countries. Figure 1 shows that, in 2019, women were still a minority on the boards of the largest listed companies in the EU14, with no country having a higher presence of women than men on the boards.

The percentage of women’s presence is closer to that of men in non-executive positions. In executive positions, the percentages are more disparate, and, with regard to CEO positions, the differences are quite accentuated. In non-executive positions, the mean values are 28.1% for women and 71.9% for men. The countries with the lowest percentages of women in non-executive positions are Spain and Greece, with 11.0% and 9.4%, respectively. In contrast, the countries that present the highest percentages of women in non-executive positions are Sweden and Italy, with 39.3% and 42.2%, respectively.

As for executive positions, the mean value for women is only 15.7%. The countries that show the lowest percentages of women in executive positions are Luxembourg with 6% and Austria with 7.5%. In contrast to this, Sweden and Ireland present the highest values, at 23.7% and 21.5%, respectively.

In terms of CEO positions, the mean value for women is even lower, at only 5.8%. The countries with the highest representation of women in CEO positions are Ireland with 16.7% and Belgium with 11.8%, and the countries with the lowest representation are Italy with 3% and Luxemburg with none.

Due to these discrepancies, the European Council has regulated the introduction of quotas for the inclusion of women in management positions. The implementation of these regulations is intended to put an end to the imbalance, which is considered unjustified and harmful, and to break the glass ceiling concept, which symbolizes the invisible barrier that continues to bar women talent from top positions in Europe’s largest companies.

2.2. Gender Differences and Similarities

Carter et al. (2010) argue that there is no single theory predicting the association between women on board and firm financial performance. Indeed, research on board gender diversity has used different theoretical frameworks.

The effects of gender differences on the business world have been studied in the literature over the years. Terjesen et al. (2009) refer to the gender self-schema as a theory that is reflected in the behavior of each individual. Gender self-schema is an individual psychological construct that is based on certain aspects and is developed during childhood. Konrad et al. (2000), in their study of gender differences and similarities, as well as preferred attributes for a particular job, argue that the male self-schema is defined by norms, rules and beliefs that are considered appropriate, such as performance creation, dominance, aggressiveness, goals, autonomy, exhibitionism and toughness. In contrast, the female gender presents itself as the support of the home, commitment, care and respect for others, as well as submission to others.

Becker (2009) advocates the theory of human capital, in which an individual’s experience, education and skills can be used to benefit a company. In this sense, directors should be able to employ all their human capital. Thus, people who put themselves forward for these positions should acquire as many skills as they need in order to be employed (Kesner 1988). However, it is argued that those responsible for selecting these professionals tend to believe that women do not meet the required requirements, which is considered one of the factors that have contributed to the low number of women on boards (Burke 2000). On the contrary, Ryan and Haslam (2007) argue that there are companies that, in a situation of change, have a greater tendency to choose women for their boards, but in more precarious conditions than men. In fact, Oakley (2000) continues to point out that women are not offered the same type of opportunities, such as training, development, promotions, and pay.

In the past, women, compared to men, tended to receive less education and professional advancement, triggering lower pay levels and consequences in their career progression (Tharenou et al. 1994); however, today, women are increasingly more likely than men to acquire a more advanced education (Hillman et al. 2002). However, despite higher academic qualifications, as Singh et al. (2008) point out, women still have less experience in senior positions.

Besides individualist theories, organization theories can also explain the presence and the attitudes of women on boards. Gendered organizational theory advocates that we cannot analyze issues related to gender inequality without considering, among other factors, the organizational culture (ideas, attitudes, and values) and the interactions on the workplace (with colleagues across different positions and power) (Acker 2012).

Indeed, previous studies show that when there is a woman in a team dominated by men, she does not feel comfortable expressing her opinions, however, if there are at least three women the gender barrier falls and they already feel free to express their ideas (Konrad et al. 2008). Moreover, although women may have skills and qualifications needed to be appointed to the board, the board intentionally discriminates against them based on stereotypes which are unrelated to their qualifications (Cotter et al. 2001), and this discrimination or stereotypes inhibits their abilities to fully contribute to business strategy (Galbreath 2011). Therefore, organizational cultural values and the socialization process can constrain women’s attitudes and behaviors in the workplace.

2.3. Gender Diversity and Firm Value

Firm value can be influenced by several factors that are intrinsic or extrinsic to a company, with the composition of the board of directors being among them. Board diversity is defined by the variety of people that make it up and the combination of the different qualities, characteristics and experiences of each individual, which influences the decision making and other processes of the board’s competence (Van der Walt and Ingley 2003). Thus, several types of diversity may impact a board’s competence, such as gender, cultural diversity, ethics, education, experience, skills, and independence.

In general, the presence of women on boards is seen positively by capital markets since there has been a positive short-term market reaction to the announcement of women nominations to sit on boards (Campbell and Mínguez Vera 2010). Economically, it is claimed that women increase shareholder value. Indeed, women are more predisposed than men to identify ethical judgmental issues (Smith et al. 2001), and certain shareholders believe that boards with a greater number of women hinder earnings management (Gonçalves et al. 2019), provide greater security to their investments, avoid legal nonconformities and prevent corporate corruption and fraud (Flynn and Adams 2004). Boards with more women directors are characterized by a greater potential in decision making, more rigorous monitoring and greater alignment with shareholder interests (Adams and Ferreira 2009). Finally, from a moral perspective, the presence of women on boards is seen as a matter of social justice (Habib and Hossain 2013).

However, there is no consensus on the impact of the presence of women on boards and firm value. Carter et al. (2010) argue that the effect of gender diversity may be distinct in different circumstances and at different periods and that the effects of diversity are endogenous to each company. The literature also suggests that there are sectors and business areas that have a better reaction to gender diversity on the board compared to others (Hillman et al. 2007).

In fact, some studies suggest that the presence of women on boards is positively related to firm values measured using Tobin’s Q (Carter et al. 2003; Abdelzaher and Abdelzaher 2019; Campbell and Mínguez Vera 2010; Reguera-Alvarado et al. 2017), whereas other studies have found no relationship (Singh et al. 2019; Marinova et al. 2016) or even a negative one (Adams and Ferreira 2009; Shehata et al. 2017). Shehata et al. (2017) argue that the inclusion of women should be carried out cautiously and adjusted to each company based on qualifications and experience in order to avoid a negative impact on company performance.

Given its crucial role, the leadership style and skills of the Board Chair are critical for Board effectiveness (Gabrielsson et al. 2007). There is evidence that women Chairs are more likely to be democratic and interactive leaders in contrast to men, who tend to be authoritative leaders (Eagly and Carli 2003). In this sense, having a woman as Chair may enhance the quality of the board’s decision-making and consequently increase firms’ performance (Peni 2014).

Indeed, Peni (2014) finds a positive relationship between the presence of women CEOs or Chairs and firm value and argue that gender-based differences may affect the CEO and Chair’s success. In contrary, Bennouri et al. (2018) find that women Chairs negatively impacts firm value but positively impact firm performance. They argue that although the results obtained underline the effectiveness of women Chairs in improving the board’s decision-making process, the leadership position of women is negatively perceived by investors.

With the increasing literature pointing to the advantages of having women on boards and the growing social movement for gender equality, several European countries have moved toward implementing quota laws to regulate the presence of women on the boards of listed and/or public-interest companies. However, there is no consensus in the literature on the introduction of women on boards through quota laws. Adams and Ferreira (2009) state that, in cases where the imposition of women on boards occurs through quotas, this integration may harm companies that are already well managed, since the reasons for integration may not be due to interests in improving governance and company performance. Moreover, Kakabadse et al. (2015) argue that the introduction of quotas does not allow for the determination of the true impact of the presence of women on a company’s performance.

Moreover, Isidro and Sobral (2015) studied the effects of the presence of women on the board of European companies that would be subject to the introduction of the quota law. They did not find a direct relationship between the presence of women and firm value but rather an indirect one through the effects on financial performance measures, such as Return on Assets and Return on Sales.

Additionally, some European countries, including Germany, Croatia, and Denmark, are (or have been) governed by women. Seierstad et al. (2017) argue that, among the several external factors that can drive changes in women’s representation on boards, political actors can play an important role. Thus, it is of interest to study whether the association between the presence of women, firm value, and financial performance is different in countries governed by women, because there may be a greater tendency to increase the presence and the role of women in the business world and in society in general.

Therefore, this study aims to answer the following research questions in the context of European 14 group (EU14)-listed companies:

- Q1: Is the presence of women on boards positively associated with firm value?

- Q2: When countries are governed by women, does the positive association between the presence of women on boards and firm value hold?

3. Methodology

3.1. Data and Sample

Financial data, as well as data concerning the constitution of the boards of the companies, are from the Orbis database. Orbis database (Bureau Van Dijk) contains financial and non-financial information, including information on boards of directors, about private and public firms across the world.

The initial sample consists of 3368 listed companies, belonging to the EU14, covering the period between 2011 and 2018. From the initial sample, companies belonging to the financial, real estate and public sectors were excluded, as they have specific business and regulatory characteristics.

Additionally, companies with null or negative book equity values are removed in order to avoid financial bias from bankrupt firms (Lins 2003; Reguera-Alvarado et al. 2017). The final sample consists of a total of 13,980 observations, related to firms from 14 European countries and 15 industries. Table 1 presents the composition of the sample by country. The country with the highest representation is France, with 22.0% of the sample, followed by Germany (18.1%) and Sweden (14.8%).

Regarding the composition of the sample by industry (Table 2), the Manufacturing sector represents 49.6% of the total firm-year observations, followed by the Information and Communication sector (15.5%).

3.2. Models

Based on previous studies (Jedi and Nayan 2018; Campbell and Mínguez-Vera 2008; Carter et al. 2010; Isidro and Sobral 2015; Gonçalves et al. 2019), we developed the following models in order to answer Q1 and Q2, respectively:

Firm valueit = β0 + β1Financial performanceit + β2Chair_Wit+ β3CEO_Wit + β4CFO_Wit + β5Sizeit + β6Levit + β7Growthit + β8Ageit + β9Countryi + β10Indi + β11Yeari + μit

Firm value is measured using Tobin’s Q, computed as the sum of the market value of equity (share price multiplied by the number of ordinary shares in issue at the fiscal year-end) and the book value of debt divided by the book value of total assets. Tobin’s Q is often used in many studies, as it is considered the closest representation of firm value (Adams and Ferreira 2009; Carter et al. 2010; Isidro and Sobral 2015). When Tobin’s Q is greater than 1, investors have the expectation that the resources available to the organization will be applied efficiently; conversely, investors have the expectation that the resources available to the organization will be applied inefficiently when this ratio is less than 1 (Campbell and Mínguez-Vera 2008).

Following previous research, financial performance is proxied by two accounting indicators: ROA, measured as net income divided by total assets, and Operating Margin, measured as operating income divided by total sales (Jedi and Nayan 2018; Carter et al. 2010; Isidro and Sobral 2015).

The presence of women on boards is measured using three dummy variables, namely, Chair_W, CEO_W, and CFO_W, which take the value of 1 if the position is occupied by a woman and 0, otherwise (Gonçalves et al. 2019).

Firm size (Size) is defined as the natural logarithm of the total assets of a firm. This variable is a key determinant of firm value and financial performance, and it is associated with greater cost control, as larger firms have larger and more complex market transactions. According to previous studies, a negative association between firm size and firm value/performance is expected (Gonçalves et al. 2018; Carter et al. 2010; Adams and Ferreira 2009; Campbell and Mínguez-Vera 2008). Financial leverage (Lev) is computed as the ratio of total liabilities to total assets. Debt is a mechanism that forces managers to generate cash flows in order to pay interest, and it promotes managers’ abilities to manage problems (Gonçalves et al. 2020; Shleifer and Vishny 1997). A negative relationship is expected between leverage, firm value and financial performance.

The variable Growth represents the annual growth rate of a company’s sales. Thus, sales growth is considered a relevant determinant of performance and is expected to be positively related to firm value and financial performance (Isidro and Sobral 2015). The age of a company (Age) is measured using the natural logarithm of the years of the company. Companies can lose their ability to compete and innovate over time. In general, many years in business can be associated with greater organizational rigidity. However, it may represent greater knowledge, skills, and specialization.

Given the possible differences between countries and industries that may influence the dependent variables under study, the variables Country and Ind are included in the models as dummy variables. Because firm value and financial performance may differ over time, the variable Year is also included to control for possible temporal effects. In order to control for heteroscedasticity and autocorrelation, the models were estimated using pooled regression with robust standard errors clustered at the firm level, accounting for potential fixed effects.

Subsequently, in conjunction with the presence of women on the board, the company’s financial performance and the impact of being in a country governed by women on the value of each company, we included Gov_W in model (2) as follows:

Firm valueit = ρ0 + ρ1Financial performanceit + ρ2Chair_Wit + ρ3CEO_Wit + ρ4CFO_Wit + ρ5Gov_Wit ρ6Sizeit + ρ7Levit + ρ8Growthit + ρ9Ageit + ρ10Countryi + ρ11Indi + β11Yeari + φit

The variable Gov_W is a dummy variable, and it takes the value of 1 when the country has a woman as a political or monarchical representative of the country and 0, otherwise. More detailed information about variables definition is provided in Appendix A.

4. Results and Discussion

4.1. Descriptive Statistics

Table 3 presents the descriptive statistics of the sample, showing that the average Tobin’s Q value is 1.068, which suggests that, on average, companies create expectations in investors that their resources will be well applied so that they will generate value in the future. Return on Assets and Operating Margin present average values of 2.1% and 6.4%, respectively.

Regarding the presence of women on the board, only 3.3% of observations have women as Chairs, 4.2% as CEOs and 5.6% as CFOs. Additionally, 22.3% of observations represent countries governed by women (Germany and Denmark).

Pearson’s correlation matrix (Table 4) shows a positive and statistically significant correlation between Tobin’s Q and the following variables: ROA, Chair_W, CEO_W, CFO_W, and Gov_W. Conversely, the variables Size, Lev, and Age are negative and significantly related to Tobin’s Q. Chair_W, CEO_W, and CFO_W present positive and significant correlations among themselves at the 1% significance level. Contrary to expectations, these variables are negatively correlated with the variable Gov_W.

In order to additionally test for the possible existence of the multicollinearity of the variables, the Variance Inflation Factor (VIF) is used. The values obtained (not tabulated) are lower than 10 for all variables; thus, all the same variables are included in the regressions, rejecting the hypothesis of multicollinearity.

4.2. The Association between Women on Boards and Firm Value

Table 5 presents the empirical results of the estimations of models (1) and (2). In terms of firm value (columns 1 and 2), both financial performance measures present a positive coefficient, suggesting that greater financial performance is associated with a greater firm value. All the gender variables present a positive coefficient, but only CFO_W shows a statistically significant one. Thus, it is possible to conclude that firms with a woman CFO have a higher firm value. Similar to Isidro and Sobral (2015), we do not find a direct effect of women Chairs on firm value. These results also point to potential organizational cultural values and the socialization process that can constrain women’s attitudes and behaviors in the workplace (Acker 2012; Galbreath 2011; Cotter et al. 2001).

In terms of control variables, smaller, less leverage, and younger firms have a higher firm value, suggesting that larger companies have to manage more complex activities and that mature firms are more rigid and less efficient at creating value. This also suggests that investors’ perceptions of their ability to innovate, introduce improvements and apply their assets are high.

Columns (3) and (4) in Table 5 present the results obtained from model 2. The variable Gov_W has a positive, statistically significant coefficient at the 1% level, suggesting that companies in countries governed by women tend to have higher firm values. It may be concluded that the presence of women in high political positions positively influences firm value. This influence may be associated with different forms of management practiced by women compared to men, demonstrating that the inclusion of women in important political positions may drive greater success for a country’s companies and may also favor the introduction of women onto company boards. As Seierstad et al. (2017) argue, political actors can play an important role on driving changes in women’s representation on the Board.

The introduction of this variable does not alter the previous results on financial performance and gender variables. ROA and Operating Margin are positively related to firm value, as expected, and all the gender variables present positive coefficients, but only CFO_W is statistically significant. In terms of control variables, the results are somewhat similar, with Size, Lev, and Age remaining negatively associated with firm value.

4.3. Additional Analysis

To further analyze the association between firm value and the presence of women on boards, three dummy variables, namely, Shareholder_Chair_W, Shareholder_CEO_W, and Shareholder_CFO_W, are included in model 1. These variables take the value 1 when the position is occupied by a woman and 0, otherwise. The objective is to test whether the relationship between the presence of women on boards and firm value remains the same when the women are also shareholders. Columns (1) and (2) in Table 6 present the results. The results suggest that companies with women Chairs or CEOs that are also shareholders have lower firm values. The results for the remaining variables are consistent with those of the main analysis.

Additionally, in order to determine whether gender changes in executive and non-executive positions influence firm value, we introduce three dummy variables in model 1: Change_Chair_W, Change_CEO_W, and Change_CFO_W. These variables assume the value 1 if the change is from a man to a woman and 0, otherwise. Columns (3) and (4) in Table 6 report the results.

Change_Chair_W presents a positive, statistically significant coefficient at the 10% level when financial performance is measured using ROA, suggesting that changing the gender of the Chair from a man to a woman brings economic benefits to firms, which is consistent with prior evidence that there is a positive short-term market reaction to the announcement of women nominations to sit on boards (Campbell and Mínguez Vera 2010).

However, there is no evidence that gender changes in CEO and CFO are positively associated with firm value. These results may suggest that the implementation of quota laws should be carefully thought out. Although gender diversity may provide greater potential in decision making and greater alignment with shareholders, the introduction of women must take into account several factors, such as the sector of the company and even the characteristics of the company’s employees (in line with Isidro and Sobral 2015).

Again, the results for the remaining variables, financial performance, gender and control variables, are similar to previous results, providing robustness to our main results and conclusions.

5. Conclusions

In recent decades, the issue of gender diversity on boards and top management has received increasing attention in the academic literature and popular press. The main objective of this study was to analyze the association between the presence of women as Chairs, CEOs and CFOs and firm value in the context of listed companies belonging to the EU14.

Our main results suggest a strong positive relationship between financial performance and firm value. Firms with women CFOs have higher firm values, measured using Tobin’s Q, suggesting the market expectations of firm future earnings is higher when the CFO position is occupied by a woman. However, similar to previous studies, we did not find evidence of an association between the presence of women as Chairs or CEOs and firm value.

The results also suggest that firms located in countries governed by women have higher firm values, corroborating the hypothesis that there are other external factors capable of influencing the perception of women’s acceptance, namely political factors.

Additional analyses showed that when a woman has a CFO position and is also a shareholder, firm values are lower. Finally, when there is a Chair change from man to woman, firm value increases.

The present study has some limitations. One limitation is related to missing data ab-out the number of women on the boards, which is relevant information for a better understanding of the relationship between women representativeness on boards and firm values. Nevertheless, our results contribute to the scarce literature that studies whether the presence of women on boards, namely in Chair positions and executive CEO and CFO positions, brings economic benefits to a firm, as well as to the ongoing debate among academics, press, governments and regulators on whether appointing women to board positions has positive valuation effects.

As future research, it would be interesting to expand the analysis by including other countries outside Europe as well as study the role women’s networks on the association between the presence of women on Board and firm value.

Author Contributions

Conceptualization, T.C.G., C.G. and M.R.; methodology, T.C.G. and M.R.; software, M.R. and T.C.G.; validation, T.C.G., C.G. and M.R.; formal analysis, M.R. ,T.C.G. and C.G.; investigation, T.C.G., C.G. and M.R.; resources, T.C.G. and M.R.; data curation, M.R.; writing—original draft preparation, M.R., T.C.G. and C.G.; writing—review and editing, T.C.G. and C.G.; visualization, T.C.G. and C.G.; supervision, T.C.G.; project administration, T.C.G.; funding acquisition, T.C.G. and C.G. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by Fundação para a Ciência e Tecnologia, Portugal, grant number UID/SOC/04521/2020.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The data was retrieved from Amadeus, under license to ISEG Lisbon School of Economics & Management.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

{kind=link}

Table A1.

Variable Definition.

| Variable | Definition | |

|---|---|---|

| Tobin’s Q | Firm value | Sum of the market value of equity (share price multiplied by the number of ordinary shares in issue at fiscal year-end) and the book value of debt divided by the book value of total assets. |

| ROA | Return on assets | Net income divided by total assets. |

| Operating Margin | Operating Margin | Operating income divided by the total sales. |

| Chair_W | Chairperson | Dummy variable that takes the value of 1 if the position is occupied by a woman and 0, otherwise. |

| CEO_W | Chief Executive Officer | Dummy variable that takes the value of 1 if the position is occupied by a woman and 0, otherwise. |

| CFO_W | Chief Financial Officer | Dummy variable that takes the value of 1 if the position is occupied by a woman and 0, otherwise. |

| Size | Firm size | Natural logarithm of total assets. |

| Lev | Financial leverage | Total liabilities divided by total assets. |

| Growth | Sales growth | Annual variation of sales (%) |

| Age | Firm age | Natural logarithm of the number of years of the firm |

| Gov_W | Political or monarchical representative of the country | Dummy variable that takes the value of to 1 if the position is occupied by a woman and 0, otherwise. |

| Ind | Industry | Binary variable that takes the value of 1 if the company belongs to the sector in question and 0, otherwise. |

| Country | Country | Binary variable that takes the value of 1 if the company belongs to the country in question and 0 otherwise. |

| Year | Year | Binary variable that takes the value of 1 if the observation belongs to the year in question and 0, otherwise. |

References

- Abdelzaher, Angie, and Dina Abdelzaher. 2019. Women on Boards and Firm Performance in Egypt: Post the Arab Spring. The Journal of Developing Areas 53: 225–41. [Google Scholar] [CrossRef]

- Acker, Joan. 2012. Gendered organizations and intersectionality: Problems and possibilities. Equality, Diversity and Inclusion: An International Journal 31: 212–24. [Google Scholar] [CrossRef]

- Adams, Renée B., and Daniel Ferreira. 2009. Women in the boardroom and their impact on governance and performance. Journal of Financial Economics 94: 291–309. [Google Scholar] [CrossRef] [Green Version]

- Adams, Renée B., Jakob de Haan, Siri Terjesen, and Hans van Ees. 2015. Board diversity: Moving the field forward. Corporate Governance: An International Review 23: 77–82. [Google Scholar] [CrossRef]

- Becker, Gary S. 2009. Human Capital: A Theoretical and Empirical Analysis, with Special Reference to Education. Chicago: University of Chicago Press. [Google Scholar]

- Bennouri, Moez, Tawhid Chtioui, Haithem Nagati, and Mehdi Nekhili. 2018. Female board directorship and firm performance: What really matters? Journal of Banking & Finance 88: 267–91. [Google Scholar]

- Burke, Ronald J. 2000. Company size, board size and numbers of women corporate directors. In Women on Corporate Boards of Directors. Dordrecht: Springer, pp. 157–67. [Google Scholar]

- Campbell, Kevin, and Antonio Mínguez-Vera. 2008. Gender diversity in the boardroom and firm financial performance. Journal of Business Ethics 83: 435–51. [Google Scholar] [CrossRef]

- Campbell, Kevin, and Antonio Mínguez Vera. 2010. Female board appointments and firm valuation: Short and long-term effects. Journal of Management & Governance 14: 37–59. [Google Scholar]

- Carter, David A., Betty J. Simkins, and W. Gary Simpson. 2003. Corporate governance, board diversity, and firm value. Financial Review 38: 33–53. [Google Scholar] [CrossRef]

- Carter, David A., Frank D’Souza, Betty J. Simkins, and W. Gary Simpson. 2010. The gender and ethnic diversity of US boards and board committees and firm financial performance. Corporate Governance: An International Review 18: 396–414. [Google Scholar] [CrossRef]

- Cotter, David A., Joan M. Hermsen, Seth Ovadia, and Reeve Vanneman. 2001. The glass ceiling effect. Social Forces 80: 655–81. [Google Scholar] [CrossRef]

- Eagly, Alice H., and Linda L. Carli. 2003. The female leadership advantage: An evaluation of the evidence. The Leadership Quarterly 14: 807–34. [Google Scholar] [CrossRef]

- Flynn, Patricia M., and Susan M. Adams. 2004. Changes will bring woman oards: Research shows that geography and industry account for considerable discrepancies in the prevalence of women directors, as does company size. But trends are favorable for more women joining corporate boards. Financial Executive 20: 32–35. [Google Scholar]

- Gabrielsson, Jonas, Morten Huse, and Alessandro Minichilli. 2007. Understanding the leadership role of the board chairperson through a team production approach. International Journal of Leadership Studies 3: 21–39. [Google Scholar]

- Gaio, Cristina, and Tiago Cruz Gonçalves. 2022. Gender diversity on the board and firms’ corporate social responsibility. International Journal of Financial Studies 10: 15. [Google Scholar] [CrossRef]

- Galbreath, Jeremy. 2011. Are there gender-related influences on corporate sustainability? A study of women on boards of directors. Journal of Management and Organization 17: 17–38. [Google Scholar] [CrossRef]

- Gonçalves, Tiago, Cristina Gaio, and Frederico Robles. 2018. The impact of Working Capital Management on firm profitability in different economic cycles: Evidence from the United Kingdom. Economics and Business Letters 7: 70–75. [Google Scholar] [CrossRef] [Green Version]

- Gonçalves, Tiago, Cristina Gaio, and Tatiana Santos. 2019. Women on the board: Do they manage earnings? empirical evidence from european listed firms. Revista Brasileira de Gestao de Negocios 21: 582–97. [Google Scholar] [CrossRef]

- Gonçalves, Tiago, Cristina Gaio, and Carlos Lélis. 2020. Accrual mispricing: Evidence from European sovereign debt crisis. Research in International Business and Finance 52: 101111. [Google Scholar] [CrossRef]

- Gonçalves, Tiago, Diego Pimentel, and Cristina Gaio. 2021. Risk and performance of European green and conventional funds. Sustainability 13: 4226. [Google Scholar] [CrossRef]

- Habib, Ahsan, and Mahmud Hossain. 2013. CEO/CFO characteristics and financial reporting quality: A review. Research in Accounting Regulation 25: 88–100. [Google Scholar] [CrossRef]

- Hillman, Amy J., Albert A. Cannella Jr., and Ira C. Harris. 2002. Women and Racial Minorities in the Boardroom: How Do Directors Differ? Journal of Management 28: 747–63. [Google Scholar] [CrossRef]

- Hillman, Amy J., Christine Shropshire, and Albert A. Cannella Jr. 2007. Organizational Predictors of Women on Corporate Boards. Academy of Management Journal 50: 941–52. [Google Scholar] [CrossRef] [Green Version]

- Isidro, Helena, and Márcia Sobral. 2015. The Effects of Women on Corporate Boards on Firm Value, Financial Performance, and Ethical and Social Compliance. Journal of Business Ethics 132: 1–19. [Google Scholar] [CrossRef]

- Jedi, Firas Farhan, and Sabri Nayan. 2018. An empirical evidence on the effect of women board representation on firm performance of companies listed in Iraq stock exchange. Business and Economic Horizons 14: 117–31. [Google Scholar] [CrossRef] [Green Version]

- Kakabadse, Nada K., Catarina Figueira, Katerina Nicolopoulou, Jessica Hong Yang, Andrew P. Kakabadse, and Mustafa F. Özbilgin. 2015. Gender Diversity and Board Performance: Women’s Experiences and Perspectives. Human Resource Management 54: 265–81. [Google Scholar] [CrossRef] [Green Version]

- Kesner, Idalene F. 1988. Directors’ Characteristics and Committee Membership: An Investigation of Type, Occupation, Tenure, and Gender. Academy of Management Journal 31: 66–84. [Google Scholar]

- Konrad, Alison M., J. Edgar Ritchie Jr., Pamela Lieb, and Elizabeth Corrigall. 2000. Sex Differences and Similarities in Job Attribute Preferences: A Meta-Analysis. Psychological Bulletin 126: 593–641. [Google Scholar] [CrossRef] [PubMed]

- Konrad, Alison M., Vicki Kramer, and Sumru Erkut. 2008. The impact of three or more women on corporate boards. Organizational Dynamics 37: 145–64. [Google Scholar] [CrossRef]

- Lins, Karl V. 2003. Equity ownership and firm value in emerging markets. Journal of Financial and Quantitative Analysis 38: 159–84. [Google Scholar] [CrossRef] [Green Version]

- Marinova, Joana, Janneke Plantenga, and Chantal Remery. 2016. Gender diversity and firm performance: Evidence from Dutch and Danish boardrooms. The International Journal of Human Resource Management 27: 1777–90. [Google Scholar] [CrossRef]

- Oakley, Judith G. 2000. Gender-based Barriers to Senior Management Positions: Understanding the Scarcity of Female CEOs. Journal of Business Ethics 27: 321–34. [Google Scholar] [CrossRef]

- Peni, Emilia. 2014. CEO and Chairperson characteristics and firm performance. Journal of Management & Governance 18: 185–205. [Google Scholar]

- Reguera-Alvarado, Nuria, Pilar de Fuentes, and Joaquina Laffarga. 2017. Does board gender diversity influence financial performance? Evidence from Spain. Journal of Business Ethics 141: 337–50. [Google Scholar] [CrossRef]

- Ryan, Michelle K., and S. Alexander Haslam. 2007. The glass cliff: Exploring the dynamics surrounding the appointment of women to precarious leadership positions. Academy of Management Review 32: 549–72. [Google Scholar] [CrossRef]

- Seierstad, Cathrine, Gillian Warner-Søderholm, Mariateresa Torchia, and Morten Huse. 2017. Increasing the Number of Women on Boards: The Role of Actors and Processes. Journal of Business Ethics 141: 289–315. [Google Scholar] [CrossRef]

- Shehata, Nermeen, Ahmed Salhin, and Moataz El-Helaly. 2017. Board diversity and firm performance: Evidence from the U.K. SMEs. Applied Economics 49: 4817–32. [Google Scholar] [CrossRef]

- Shleifer, Andrei, and Robert W. Vishny. 1997. A Survey of Corporate Governance. The Journal of Finance 52: 737–83. [Google Scholar] [CrossRef]

- Singh, Val, Siri Terjesen, and Susan Vinnicombe. 2008. Newly appointed directors in the boardroom: How do women and men differ? European Management Journal 26: 48–58. [Google Scholar] [CrossRef] [Green Version]

- Singh, Amit Kumar, Shubham Singhania, and Varda Sardana. 2019. Do Women on Boards affect Firm’s Financial Performance? Evidence from Indian IPO Firms. Australasian Accounting, Business and Finance Journal 13: 53–68. [Google Scholar] [CrossRef]

- Smith, Wanda J., Richard E. Wokutch, K. Vernard Harrington, and Bryan S. Dennis. 2001. An examination of the influence of diversity and stakeholder role on corporate social orientation. Business and Society 40: 266–94. [Google Scholar] [CrossRef]

- Terjesen, Siri, Ruth Sealy, and Val Singh. 2009. Women directors on corporate boards: A review and research agenda. Corporate Governance: An International Review 17: 320–37. [Google Scholar] [CrossRef] [Green Version]

- Tharenou, Phyllis, Shane Latimer, and Denise Conroy. 1994. How do you Make it to the Top? An Examination of Influences on Women’s and Men’s Managerial Advancement. Academy of Management Journal 37: 899–931. [Google Scholar]

- Van der Walt, Nicholas, and Coral Ingley. 2003. Board Dynamics and the Influence of Professional Background, Gender and Ethnic Diversity of Directors. Corporate Governance 11: 218–34. [Google Scholar] [CrossRef]

Figure 1.

Percentage of women in CEO, executive and non-executive positions in the largest listed companies in EU14 in 2019. Source: data from European Institute for Gender Equality.

Figure 1.

Percentage of women in CEO, executive and non-executive positions in the largest listed companies in EU14 in 2019. Source: data from European Institute for Gender Equality.

Table 1.

Sample composition by country.

| Country | Observations | % |

|---|---|---|

| Austria | 310 | 2.2 |

| Belgium | 554 | 4.0 |

| Denmark | 606 | 4.3 |

| Finland | 721 | 5.2 |

| France | 3.069 | 22.0 |

| Germany | 2.530 | 18.1 |

| Greece | 937 | 6.7 |

| Ireland | 262 | 1.9 |

| Italy | 1.183 | 8.5 |

| Luxembourg | 215 | 1.5 |

| Netherlands | 567 | 4.1 |

| Portugal | 265 | 1.9 |

| Spain | 695 | 5.0 |

| Sweden | 2.066 | 14.8 |

| Total | 13.980 | 100 |

Table 2.

Sample composition by industry.

| Sector of Activity | Observations | % |

|---|---|---|

| Agriculture, forestry and fishing | 168 | 1.2 |

| Mining and quarrying | 270 | 1.9 |

| Manufacturing | 6.933 | 49.6 |

| Electricity, gas, steam, and air conditioning supply | 399 | 2.9 |

| Water supply; sewerage, waste management, and remediation activities | 103 | 0.7 |

| Construction | 446 | 3.2 |

| Wholesale and retail trade; repair of motor vehicles and motorcycles | 1.181 | 8.4 |

| Transportation and storage | 464 | 3.3 |

| Accommodation and food service activities | 202 | 1.4 |

| Information and Communication | 2.169 | 15.5 |

| Professional, scientific, and technical activities | 638 | 4.6 |

| Administrative and support service activities | 356 | 2.5 |

| Human health and social work activities | 207 | 1.5 |

| Arts, entertainment and recreation | 273 | 2.0 |

| Other service activities | 171 | 1.2 |

| Total | 13.980 | 100 |

Table 3.

Descriptive statistics.

| Mean | Standard Deviation | Median | Minimum | Maximum | |

|---|---|---|---|---|---|

| Tobin’s Q | 1.068 | 1.978 | 0.643 | 0.002 | 145.923 |

| ROA | 0.021 | 0.112 | 0.031 | −1.045 | 2.501 |

| Operating Margin | 0.064 | 1.05 | 0.060 | −37.380 | 101.388 |

| Chair_W | 0.033 | 0.178 | 0 | 0 | 1 |

| CEO_W | 0.042 | 0.200 | 0 | 0 | 1 |

| CFO_W | 0.056 | 0.230 | 0 | 0 | 1 |

| Gov_W | 0.223 | 0.416 | 0 | 0 | 1 |

| Size | 19.437 | 2.391 | 19.247 | 11.928 | 26.850 |

| Lev | 0.551 | 0.191 | 0.563 | 0.003 | 0.999 |

| Growth | 0.250 | 9.668 | 0.041 | −92.943 | 986.455 |

| Age | 3.510 | 0.924 | 3.401 | 0 | 6.482 |

Table 4.

Pearson’s correlation matrix.

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | (11) | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| (1) Tobin’s Q | 1.000 | ||||||||||

| (2) ROA | 0.137 *** | 1.000 | |||||||||

| (3) Operating Margin | 0.010 | 0.126 *** | 1.000 | ||||||||

| (4) Char_W | 0.035 *** | −0.013 | −0.008 | 1.000 | |||||||

| (5) CEO_W | 0.030 *** | −0.016 * | −0.005 | 0.226 *** | 1.000 | ||||||

| (6) CFO_W | 0.047 *** | 0.017 ** | −0.023 *** | 0.060 *** | 0.104 *** | 1.000 | |||||

| (7) GOV_W | 0.040 *** | 0.046 *** | 0.018 ** | -0.068 *** | −0.050 *** | −0.070 *** | 1.000 | ||||

| (8) Size | −0.145 *** | 0.220 *** | 0.049 *** | 0.007 | −0.019 ** | 0.010 | 0.006 | 1.000 | |||

| (9) Lev | −0.241 *** | −0.192 *** | 0.000 | 0.006 | −0.033 *** | −0.017 ** | −0.052 *** | 0.260 *** | 1.000 | ||

| (10) Growth | 0.013 | 0.004 | 0.006 | −0.003 | −0.002 | −0.005 | −0.008 | −0.014 * | −0.028 ** | 1.000 | |

| (11) Age | −0.110 *** | 0.126 *** | 0.017 ** | 0.017 * | −0.021 ** | −0.016 * | 0.110 ** | 0.280 *** | 0.072 *** | −0.014 * | 1.000 |

Note: ***, ** and * denote statistical significance at 1%, 5%, and 10% levels, respectively.

Table 5.

Women on boards and firm value.

| Tobin’s Q (1) | Tobin’s Q (2) | Tobin’s Q (3) | Tobin’s Q (4) | |

|---|---|---|---|---|

| ROA | 2.405 *** | - | 2.386 *** | |

| (0.290) | (0.289) | |||

| Operating margin | - | 0.030 *** | 0.028 *** | |

| (0.008) | (0.008) | |||

| Chair_W | 0.397 | 0.380 | 0.424 | 0.409 |

| (0.347) | (0.346) | (0.346) | (0.346) | |

| CEO_W | 0.106 | 0.082 | 0.118 | 0.095 |

| (0.107) | (0.108) | (0.107) | (0.108) | |

| CFO_W | 0.328 *** | 0.347 *** | 0.351 *** | 0.371 *** |

| (0.062) | (0.063) | (0.062) | (0.063) | |

| Gov_W | - | - | 0.198 *** | 0.212 *** |

| (0.032) | (0.033) | |||

| Size | −0.087 *** | −0.056 *** | −0.086 *** | −0.056 *** |

| (0.009) | (0.009) | (0.009) | (0.009) | |

| Lev | −1.864 *** | −2.240 *** | −1.841 *** | −2.213 *** |

| (0.111) | (0.109) | (0.112) | (0.110) | |

| Growth | 0.001 | 0.001 | 0.001 | 0.001 |

| (0.001) | (0.001) | (0.001) | (0.001) | |

| Age | −0.182 *** | −0.162 *** | −0.192 *** | −0.173 *** |

| (0.025) | (0.024) | (0.024) | (0.024) | |

| Constant | 4.327 *** | 3.929 *** | 4.292 *** | 3.894 *** |

| (0.295) | (0.291) | (0.296) | (0.291) | |

| Observations | 13.980 | 13.980 | 13.980 | 13.980 |

| Adjusted R2 | 0.090 | 0.074 | 0.092 | 0.076 |

| F-statistic | 104.882 | 98.899 | 100.519 | 95.954 |

| P-value | 0.000 | 0.000 | 0.000 | 0.000 |

Note: *** denotes statistical significance at 1%. Standard errors are in parentheses.

Table 6.

Role of being a shareholder and gender change in Chair, CEO, and CFO positions.

| Tobin’s Q (1) | Tobin’s Q (2) | Tobin’s Q (3) | Tobin’s Q (4) | |

|---|---|---|---|---|

| ROA | 2.399 *** | - | 2.420 *** | - |

| (0.290) | (0.289) | |||

| Operating Margin | - | 0.029 *** | - | 0.030 *** |

| (0.008) | (0.009) | |||

| Chair_W | 0.576 | 0.565 | 0.207 | 0.198 |

| (0.429) | (0.429) | (0.266) | (0.265) | |

| CEO_W | 0.154 | 0.132 | 0.129 | 0.103 |

| (0.123) | (0.124) | (0.096) | (0.099) | |

| CFO_W | 0.307 *** | 0.324 *** | 0.495 *** | 0.502 *** |

| (0.063) | (0.065) | (0.096) | (0.096) | |

| Shareholder_Chair_W | −0.881 ** | −0.907 ** | - | - |

| (0.426) | (0.425) | |||

| Shareholder_CEO_W | −0.338 ** | −0.346 ** | - | - |

| (0.153) | (0.157) | |||

| Shareholder_CFO_W | 0.343 | 0.363 | - | - |

| (0.335) | (0.374) | |||

| Change_Chair_W | - | - | 0.635 * | 0.603 |

| (0.381) | (0.381) | |||

| Change_CEO_W | - | - | −0.062 | −0.055 |

| (0.104) | (0.107) | |||

| Change_CFO_W | - | - | −0.217 | −0.201 |

| (0.206) | (0.205) | |||

| Size | −0.088 *** | −0.058 *** | −0.086 *** | −0.056 *** |

| (0.010) | (0.009) | (0.009) | (0.009) | |

| Lev | −1.858 *** | −2.233 *** | −1.857 *** | −2.236 *** |

| (0.110) | (0.108) | (0.108) | (0.107) | |

| Growth | 0.001 | 0.001 | 0.001 | 0.001 |

| (0.001) | (0.001) | (0.001) | (0.001) | |

| Age | −0.179 *** | −0.159 *** | −0.180 *** | −0.160 *** |

| (0.024) | (0.024) | (0.023) | (0.023) | |

| Constant | 4.352 *** | 3.955 *** | 4.311 *** | 3.911 *** |

| (0.299) | (0.294) | (0.285) | (0.279) | |

| Observations | 13.980 | 13.980 | 13.980 | 13.980 |

| Adjusted R2 | 0.092 | 0.075 | 0.092 | 0.076 |

| F-statistic | 77.114 | 72.930 | 77.683 | 73.237 |

| P-value | 0.000 | 0.000 | 0.000 | 0.000 |

Note: ***, ** and * denote statistical significance at 1%, 5% and 10% levels, respectively. Standard errors are in parentheses.

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Gonçalves, T.C.; Gaio, C.; Rodrigues, M. The Impact of Women Power on Firm Value. Adm. Sci. 2022, 12, 93. https://doi.org/10.3390/admsci12030093

AMA Style

Gonçalves TC, Gaio C, Rodrigues M. The Impact of Women Power on Firm Value. Administrative Sciences. 2022; 12(3):93. https://doi.org/10.3390/admsci12030093

Chicago/Turabian StyleGonçalves, Tiago Cruz, Cristina Gaio, and Micaela Rodrigues. 2022. "The Impact of Women Power on Firm Value" Administrative Sciences 12, no. 3: 93. https://doi.org/10.3390/admsci12030093

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.