Abstract

In this article, we provide empirical evidence of an important economic consequence after major changes in accounting standards. More precisely, we document that several companies have switched their pension scheme from a traditional defined benefit (db) scheme to a defined contribution (dc) scheme. In many cases, the annual reports of the pension funds and their sponsoring companies state that the introduction of IFRS is the main reason for switching from a db to dc scheme. We also analyse which company or pension fund characteristics might be related to the decision to switch. Even though many companies seem to consider switching to dc schemes, already 12 out of the 44 largest company pension schemes have converted their pension scheme. This is an important economic consequence attributed to the introduction of new accounting standards. Our results do not indicate a clear pattern of company characteristics that predict which companies are more likely to switch, although the relative size of the pension plan assets compared with the company's equity seems weakly positively related to switching.

Similar content being viewed by others

INTRODUCTION

With Regulation EC 1606/2002, the European Union has decided that all listed companies in Europe should apply the International Financial Reporting Standards (IFRS) for annual accounts starting on or after 1 January 2005. The introduction of new accounting standards may lead to economic consequences for the companies that are now forced to adopt the new standards. In this article, we investigate whether the introduction of these new financial reporting standards influences the choice of pension schemes that Dutch companies offer their employees. In order to do so, we investigate the statements of several companies that changed their pension scheme recently from defined benefit (db) to defined contribution (dc). Moreover, we empirically analyse which characteristics determine the change in pension scheme by investigating a sample of large Dutch pension schemes. Using a sample of Dutch pension schemes has a clear advantage when analysing the economic consequences on pension schemes following the introduction of IFRS. The Netherlands has one of the most developed db second-pillar pension systems that was confronted with the new accounting treatment of pensions after the introduction of IFRS. Hence, the economic consequences can be expected to be largest in the Netherlands.

Traditionally, most Dutch companies have pension schemes with db characteristics. The company has promised to make additional contributions (one-off or smoothed through increased contributions over a number of years) to the pension fund if it becomes insolvent. With an ageing employee population and a growing number of pensioners, the mechanism of increasing contributions has become less effective these days and the company should decide whether it can and wants to guarantee pension scheme solvency in the future. In the Netherlands, the steering mechanism of conditional inflation compensation has been strengthened over the past years by moving from final-pay to average-pay pension schemes. In final-pay schemes, only the retired lose out on inflation compensation, but in average-pay schemes both active and inactive participants share this negative outcome. The number of pension funds that offer average-pay instead of final-pay has more than doubled from 16 per cent to 54 per cent over the period 1998–2010. The number of active participants in average-pay schemes has increased in the same period from 1.2 million (25 per cent) to 5.2 million (91 per cent). The number of active participants in full dc schemes has increased from less than 0.1 million (0.5 per cent) to 0.3 million (4.5 per cent) in the same period.1 In this article, we analyse whether the introduction of IFRS leads companies to shift more pension risks to their employees.

The contribution of this article is twofold. First, we establish that corporate and pension fund communication point towards economic consequences of the introduction of IFRS. For the majority of the pension funds analysed in more detail, we find an explicit mention of IFRS as the driver for shifting more pension risk towards the employees. Second, we analyse the characteristics of the companies and their pension schemes to see which companies are most likely to shift risks to their employees. We find weak evidence that pension schemes from larger pension funds relative to their sponsor's equity capital are more likely to be converted from db to dc schemes. Although it seems that larger pension scheme assets relative to its sponsor's equity increase the probability of a switch, our results indicate that there are no clear characteristics associated with scheme switching. This article contributes to our understanding of accounting in the sense that changes in local accounting standards have more economic impact than foreign standards, although the standard by itself does not contain new information.

The set-up of this article is as follows. In the next section, we describe the IFRS pension accounting and the changes with the previous Dutch accounting principles on pensions. In the subsequent section, we discuss several Dutch companies that have already switched from db schemes to collective dc schemes. In the penultimate section, we analyse the changes in pension schemes for large Dutch pension plans. We conclude with our main findings and projections for the future in the final section.

IFRS AND DUTCH PENSION ACCOUNTING

The pension accounting standard for IFRS is a leftover from the time that the standards were known as International Accounting Standards (IAS). According to IAS 19 ‘Employee benefits’, the company has to classify its pension scheme as dc or db. A dc pension plan is a scheme in which the company only pays a fixed pension premium and is not required to make any other pension contributions. As companies with dc schemes face no liabilities except for the fixed pension contribution, it suffices to account for these contributions as the pension expense. All other schemes are considered to be db schemes.2 Funding shortages of a db scheme will be visible on the company's balance sheet and earnings statement. The reason for this is that the company (partially) guarantees the benefits, and hence funding shortages have to be paid for.

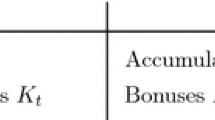

An overview of the relationship between the company and the pension fund is given in Figure 1, taken from Swinkels.3 It shows the three main participants in the pension deal: the company, the pension fund and the employee or pensioner. The company and employee both contribute to the pension fund. The pension fund in turn supplies the pensioners with nominal pensions and, if the financial situation allows, inflation compensation. One of the two regulators, De Nederlandsche Bank (DNB), is involved with the financial solvency of the pension fund and the other Autoriteit Financiële Markten (AFM) supervises the way in which the pension fund communicates with its participants about the pension scheme. In principle, IAS 19 only affects listed companies sponsoring a pension scheme and not the pension funds themselves. Pension funds would have to report according to IAS 26 ‘Accounting and Reporting by Retirement Benefit Plans’, but as pension funds are not listed companies they are required to use Dutch pension fund accounting standard RJ 610 ‘Pension funds’.4 Note that the requirements of Dutch pension fund accounting are typically higher than the standards set out in IAS 26.

An overview of the Dutch pension fund landscape.Note: The figure shows the three main participants: the company, the pension fund and the employee or retiree. The two pension fund regulators are also depicted. This figure also shows that companies have a financing agreement with the pension fund, in which they state the pension contributions (premiums). When there is a big surplus, funds could run from the pension fund to the company. Employees may have to pay part of the total premium themselves. The benefit for the employee and retiree is the nominal pension claim and annual inflation compensation (indexation).

Non-listed Dutch companies should in principle apply the Dutch accounting standards as published by the Raad voor de Jaarverslaggeving (RJ). The pension standard is known as RJ 271 and used to be a translation of IAS 19 with the exception of multi-employer schemes that could be accounted for as if it were dc schemes. Recently, the RJ introduced a completely new set of financial reporting standards for Dutch pension schemes. Starting from 2008, pension schemes only have to account for the pension premiums in the income statement, and only have to record a liability if the scheme has a funding shortage in nominal terms.5, 6 This change is the result of a long and heated lobby on the risk sharing elements between employer and employee in Dutch pension arrangements (see Ponds and Van Riel7 and the effect this has on the discount rate for pension liabilities; see Swinkels8). Such lobbying phenomena have been described before in the pension accounting literature. For example, Francis9 finds that companies that experience negative consequences from changes in the US pension accounting standards are the ones that exert the largest pressure against these changes (and not without success).

Previous changes in accounting principles in the United States and the United Kingdom indicate that companies prefer to have a stable income statement and therefore tend to favour a fixed contribution rate.10, 11, 12 This means that many db schemes have been closed and are replaced by dc schemes. Klumpes et al13 find that UK companies that run larger pension risks are more likely to close their db scheme for new entrants. Ali and Kumar14 find that the impact of the new standards on the magnitude of the pension expense is important for an early adoption of new accounting principles in the United States. Klumpes and Wittington15 find that the use of a high discount rate is the most important characteristic for early adoption of new accounting rules in the United Kingdom. Mittelstaedt16 indicates that weakening corporate earnings figures may result in less pension contributions made by the company, reversion of previously paid contributions, or in extreme cases closure of the pension scheme. Munnell et al17 mention costs reductions caused by intensive global competition as a possible cause of the termination of db schemes of healthy companies. Munnell et al17 also put forward that accounting gains may cause healthy firms to terminate their pension scheme in a low interest rate environment. In the United States, the so-called cash balance schemes have become very popular to limit the risk for the employer. Cash balance schemes are in principle db schemes, but with several dc characteristics (see Cahill and Soto18 or Johnston et al19 for a detailed description of cash balance schemes). D’Souza et al20 find that companies with high pension expenses and a higher average workforce age are more likely to switch their traditional db scheme to a cash balance scheme. Kapinos21 adds that the number of people enrolled in the pension scheme has a positive influence, and union status, funding status and the total number of db pension plans with one employer have a negative influence on the probability of plan conversion. This suggests that cost and/or risk reduction are driving factors affecting the decision to switch from traditional to cash-balance schemes.

Many Dutch companies have listings abroad that require them to apply US or UK pension accounting standards that had fair value elements before the introduction of IFRS. This makes it less plausible that the adoption of IFRS should cause pension surprises at all. Perhaps the performance of the management team is measured against local earnings measures, which would justify their sudden interest in reducing the company's pension risk.

In the Netherlands, a new concept that tries to keep many of the existing pension elements without interfering with the sponsoring company's balance sheet has gained popularity: collective defined contribution (cdc).22 This concept means that the company still offers a db scheme to its employees, in most cases an inflation-indexed average-pay scheme. The financing agreement between the company and the pension fund states that the pension premium is fixed (for at least 5 years) and there will be no other contributions from or to the company. The pension premium has to cover the costs of the pension scheme and usually contains an additional component to compensate employees because they now bear the investment risk (see Hoevenaars et al23). In the event of insolvency, a funding ratio below 105 per cent, the company makes no additional contributions, but the board of the pension fund decides whether the shortage will be reduced by leaving out compensation or cutting pension rights.24 A crucial element of this pension scheme is that companies no longer take responsibility for the pensions of their (past) employees when the solvency of the pension fund is weak.25, 26 This lack of solidarity between employer and employee is a radical change in the Dutch labour markets. In this study, we try to link the introduction of new financial reporting standards with changing risk sharing contracts within the Netherlands (see Ponds and Van Riel7 and Dixon and Monk27). Hence, we establish that there are real economic consequences following changes in accounting standards.

PUBLIC STATEMENTS OF SWITCHING COMPANIES

Several companies have been in the news because of the explicit breach of the solidarity between employer and employee in the pension contract. These companies have tried to change their db scheme into a cdc scheme that has been discussed in the previous section. In this section, we would like to list several of the public statements of companies that recently have switched from db schemes to cdc schemes, in more detail. It seems that (managers of) these companies dislike the influence that db schemes might have on the balance sheet and income statement, and that they are even willing to pay a higher average contribution rate to pay for the reduction of this volatility.

Akzo Nobel is a Dutch chemical company represented in the AEX stock market index. In addition to its stock market listing at Euronext, it is also listed in the United States on NASDAQ. This means that Akzo Nobel is also required to use US pension accounting standards for the forms it is required to hand in to the Securities and Exchange Commission. In a press release on 1 July 2005, the chief financial officer (CFO) of Akzo Nobel states: ‘Fluctuations in the pension fund due to market circumstances have had too much influence on the Company's balance sheet and results. By moving to a defined contribution scheme – which starts on 1 July 2005 – we will pay a fixed annual premium’. With this statement, the CFO points to the possible pension accounting effects of the current pension scheme and the need to change the scheme. When we examine the new finance arrangement, we observe that selling the pension guarantee comes at a price for the company. The fixed contribution amounts to 20 per cent of the pensionable wage.28 The company further contributes a one-off payment of €150 million and a subordinated loan of €100 million. These payments should prevent wealth (that is, the value of the guarantee) transfers from the employees to the company, which, according to Reiter and Omer,29 was the case when many US companies closed their db schemes in the late 1980s.

DSM is like Akzo Nobel, a Dutch company from the chemical sector represented in the AEX stock market index. DSM does not have any listings abroad and hence has not been forced to use foreign pension accounting standards in the past. A press release states: ‘The collective labour agreement states that DSM does not need to back the pension fund in case of shortages. […] The shift of investment risks has to do with the new accounting system, IFRS’.30 Here also explicitly the introduction of the new accounting standards is used to motivate the switch in pension scheme. The price for conversion of the plan is a contribution rate increasing from 12 per cent to 21 per cent of the pensionable wage. In April 2006, it became clear that DSM still has to account for the new pension scheme as a db scheme, as in advantageous future scenarios the company is still entitled to receive part of the surplus. According to IFRS, such pension scheme does not qualify as a dc scheme, although the accountant has approved that the company bears no downside risk anymore.

SNS Reaal Group is a bank and insurance company that was only recently listed on Euronext. Nevertheless, it reported according to IFRS before its listing. From the 2005 semi-annual report of SNS Reaal Group, it seems that the pension scheme has been changed retrospectively from db to dc: ‘The valuation principles for pensions have been changed according to IFRS. IAS 19 is used in IFRS, whereas SNS Reaal Group GAAP applied RJ 271. Also, the pension scheme has been changed on 1 January 2004 from a defined benefit scheme to a defined contribution scheme’.31 The company does not mention IFRS explicitly as the culprit for the change in pension scheme, but mentions it in the same paragraph as implementing IAS 19. A union report states that IFRS is the most important reason: ‘The most important reason for this is the introduction of a fixed contribution pension scheme under IFRS regulation. […] SNS Reaal Group pays this fix contribution and cannot be held responsible for any possible shortages and does not have a right to claim possible surpluses’.32 The price for switching to this scheme follows from the same union report, stating a fixed contribution of 21.5 per cent of the pensionable wage and a one-off contribution of €105 million.

ARCADIS is a Dutch engineering and consulting firm with a listing on Euronext. The company has been listed on NASDAQ since the merger with Geraghty & Miller in 1993. Thus, ARCADIS has ample experience with accounting for its db scheme according to the US accounting standards. The 2003 annual report mentions a discussion in the audit committee about the Dutch pension scheme: ‘This discussion focused on the influence of the Dutch Pension Plan on the result as reported under US Generally Accepted Accounting Principles and the consequences thereof given the new regulations in The Netherlands’. A little further in the report, the company mentions that it will start investigating possibilities to move from a db scheme to a dc scheme: ‘The current pension scheme in The Netherlands is based on the defined benefit system; therefore, financial developments in the pension fund can, depending on the accounting rules that apply, have a great effect on the Company's results. ARCADIS’ policy is, therefore, aimed at converting the pension scheme into the defined contribution system’. This could imply that some Dutch companies that are currently still following a db scheme might need more time to switch from a db to a dc scheme. The 2004 annual report indicates that the switch to a dc scheme has been accomplished. ‘In 2004, the pension plan for the majority of employees in the Netherlands was modified. This was necessary to keep the plan affordable and to warrant ARCADIS against the considerable consequences resulting from the 2005 introduction of the International Financial Reporting Standards. In the new pension plan, ARCADIS has changed from a defined benefit to a defined contribution plan’. Once more, the introduction of IFRS is used to motivate the pension change. Lately, there have been numerous companies (both listed and non-listed) that announced an intended change in the type of pension scheme because of new accounting rules. For many companies, this is merely an accounting issue, as they already had a financing agreement with the pension fund that contains explicit limits on the liability of the sponsoring company. Under Dutch accounting standards, they were not required to disclose information about the pension liabilities and were always assumed to have db schemes.

Some other notable quotes are those of the Pension Fund VWS (annual report 2005): ‘The pension scheme has been substantially changed starting 31 December 2005. Background for this change were the new accounting regulations for companies …’ and of the Telegraaf Media Groep (annual report 2005): ‘Partly this is the consequence of the new pension arrangement with Telegraaf 1959 Pension Fund, in which (under IFRS) a shift from a defined-benefits to a collective defined-contribution scheme has taken place’.

It seems remarkable that Dutch companies listed on a US or UK stock exchange are using IFRS as a motivation for transforming their pension scheme. These companies have been required to estimate the consequences of db scheme accounting and the influence this has had on their earnings following foreign standards for many years, but only now are they reconsidering their promised pension liabilities in more detail. One explanation is that companies with foreign listings are aware of the possible impact on accounting figures, but had no incentive to change the schemes because of the dominant importance of local accounting standards. As they have already done the calculations, one could hypothesize that companies with a foreign listing are quicker in changing their pension schemes.

Thomas33 suggests that US companies that need cash for their operating business had the possibility to terminate their over-funded pension plan to get hold of the excess assets present in the scheme. Such asset reversions are virtually impossible in the Netherlands as employees make up at least 50 per cent of the boards of pension funds. Many Dutch pension funds had large solvency surpluses at the end of the 1990s, and thus the option-value of the guarantee was worth only a little and possible money flows from the pension fund to the sponsor company were reality in some case (possibly to circumvent planned taxation for pension fund surpluses). In such case of high funding ratios, it is relatively easy for a company to switch form db to dc. However, after the stock market downturn in the period 2000–2003, the solvency was substantially less and hence the guarantee of the company worth more and switches were much more difficult. Hoevenaars et al23 demonstrate how to calculate the fair value of the guarantee of the sponsor company.34, 35, 36

Disclosures in the press about the nature of the financing agreements between the pension fund and the sponsoring company in collective dc schemes indicate that the fixed premium level is fixed for a period of 5 years. It is likely that after this period the contribution rate can be changed depending on the return on plan assets. When pension rights must be reduced, there will be a high pressure from the employees on the sponsor to increase contributions. On the other hand, when solvency is sufficient, the company will put pressure on the employees to accept lower contribution rates as part of the labour agreement. The accountant perhaps should judge whether these residual risks are acceptable under dc scheme pension accounting. At this stage, it seems that accountants are willing to qualify such pension agreement as dc. Communication with the participants is of utmost importance – if the participants are not aware of the risks due to a lack of communication, the db plan becomes a so-called constructive obligation and hence qualifies as db instead of dc.

EMPIRICAL ANALYSIS

The previous section contained evidence on IFRS being the motivation of companies to switch their pension scheme from db to dc. This section contains a sample of 44 Dutch company pension funds.37 Data from these pension funds are obtained from annual reports of the pension funds. The sample is limited to corporate pension schemes and limited to the largest pension funds measured by total assets. The data are hand collected from the annual reports for the study period 2001–2006. We also hand collected data from the annual reports of the companies sponsoring these corporate pension funds.38

In Table 1, we present the data used in our empirical analysis. We observe that 27 per cent (12 out of 44) of the pension schemes have announced to change from a db to a dc scheme. This change is indicated with a ‘1’ in the column SWITCH. The column with RETIR contains the percentage of participants who are currently not employed by the company (the sum of retirees and employees who have left the company without taking their pension entitlement to their new employer). This variable measures the maturity of the pension scheme.39 The column with PREM has the pension premiums as a fraction of the total assets. The lower this figure, the more difficult it is for the company to recover from solvency problems by increasing the premiums. LN ASS is the natural logarithm of the fair value of plan assets. Table 1 is sorted on the size of the pension fund, which is this variable. Column FI ALLO contains the fraction of the investment portfolio invested in fixed income (or cash) assets. Funds with a riskier investment profile might be more willing to limit company risk by shifting investment risks to participants.40, 41 The next column VOL FR is the volatility of the funding ratio, calculated as the volatility of the funding ratio over the 5-year period from 2002 to 2006. This variable is also an indication of the risk embedded in the pension scheme. The last two columns, REL BAL and REL EQ, denote the relative importance of the pension plan relative to the sponsor company. The former is the difference in the natural logarithm of the total balance of the sponsor company minus the LN ASS, and the latter the natural logarithm of the total book equity of the sponsor company minus LN ASS. The larger the pension fund relative to the sponsor company, the more likely it is that risks will be explicitly shifted towards scheme participants by a switch to dc. Klumpes et al13 indicate that the choice to curtail pension schemes is mainly driven by the potential impact on the balance sheet and income statement.42, 43

A preliminary analysis to gauge the importance of each of the variables is to investigate the characteristics of both the sample of firms that switch and the sample that does not switch. Table 2 shows the results from this split. At first glance, it seems that the differences between the two subsamples are limited. It seems that the schemes that switch are smaller than the firms that do not switch. This could be due to larger costs for large schemes to switch, possibly for reputation or publicity or the larger influence of unions on the pension arrangements for these companies. It also seems that the switching schemes are large relative to their pension plan sponsors. For example, the average (log) difference of the fair value of pension assets relative to company book equity is −1.30 for switching firms, and −0.05 for non-switching firms. Moreover, for 10 out of 12 switching firms, this variable is negative, while this is only in 16 out of 32 non-switching firms.

We investigate which of the characteristics mentioned above influence the decision to change the company pension scheme from db to dc in a multivariate context. As the dependent variable is a binary variable, with ‘0’ indicating ‘no switch’ and ‘1’ indicating ‘switch’, we make use of a probit model to determine the influence of each variable.

with Pr{…} the conditional probability that a pension plans switches from db to (c)dc and X the matrix of conditioning variables. We estimate the parameters β to empirically analyse the importance of each of the variables. Positive (negative) estimates increase (decrease) the probability of a switch from db to dc.

Table 3 shows the estimation results. The left part of Table 3 shows the estimation results from the univariate model, which means that each explanatory variable is analysed in isolation. The results indicate that the RELEQ variable is statistically significant at the 95 per cent confidence level. Its negative coefficient implies that the pension schemes from larger pension funds relative to their sponsor's equity capital are more likely to be converted from db to (c)dc schemes. The other variables have the expected signs, but the relatively low number of observations makes it difficult to find statistical significance. The right side of Table 3 shows the estimation results for the multivariate model. Although the parameter estimates remain qualitatively similar to the univariate case, again the low number of observations reduces the statistical significance of the relationships found. Our results are in line with Klumpes et al13 and Ali and Kumar,14 indicating that the firms to take action first are the ones that expect the highest impact from the accounting changes.

CONCLUSION

The Dutch pension system that traditionally has been dominated by schemes with db characteristics is under heavy pressure. New minimum funding requirements introduced by the parliament and accounting standards with fair value add to the discussion on the viability of the system.

In this article, we investigate four Dutch companies that explicitly mention the introduction of IFRS as the main cause for their switch from db schemes to dc schemes. In contrast to the United States or the United Kingdom, the recent movements in the Netherlands seem to point towards collective instead of individual dc schemes. For the participants in the fund, a conditional indexed average-pay scheme remains the basis, but the company has no responsibility to make additional contributions in bad times (or receive contribution discounts in good times). These developments officially eliminate the pension solidarity between employer and employee that traditionally could be seen in the Netherlands. This also means that the pension fund gets more responsibilities towards participants, and that pension fund governance becomes more important in the future.

Given the developments in the United States and the United Kingdom in the past, we expect that companies in the Netherlands also would like to reduce pension risks. It seems that pension schemes with many assets compared to the sponsor company equity are the most likely to have switched. Reduced pension fund solvency and tough international competition might lead more companies to replace their db scheme to a dc scheme in the future. Further research in this area is needed before stronger conclusions can be drawn.

References and Notes

Source: De Nederlandsche Bank, http://www.dnb.nl.

Under US GAAP, only individual dc pension plans qualify as dc, whereas collective dc pension plans are still treated as if they are db pension plans. Multi-employer plans are considered dc under US GAAP, as in the Dutch RJ 271.

Swinkels, L. (2006) Zijn pensioenregelingen gewijzigd als gevolg van de introductie van IFRS? Maandblad voor Accountancy en Bedrijfseconomie 80 (11): 562–570.

The Dutch Minister of Justice has informed the Dutch parliament that pension funds should follow the Dutch accounting regulations instead of IFRS (reference letter: 5274274/04/06, March 2004).

Napier, C.J. (2009) The logic of pension accounting. Accounting and Business Research 39 (3): 231–249.

See Napier5 for a discussion on the choices with respect to pension accounting.

Ponds, E.H.M. and Van Riel, B. (2009) Sharing risk: The Netherlands’ new approach to pensions. Journal of Pension Economics and Finance 8 (1): 91–105.

Swinkels, L. (2011) The case for local fair value discount rates under IFRS. Pensions 16 (2): 107–114.

Francis, J.R. (1987) Lobbying against proposed accounting standards: the case of employers’ pension accounting. Journal of Accounting and Public Policy 6 (1): 35–57.

For a more extensive review on pension accounting research, we refer the reader to Glaum.11 Recent trends in international pension provision are described in Barr.12.

Glaum, M. (2009) Pension accounting and research: A review. Accounting and Business Research 39 (3): 273–311.

Barr, N. (2009) International trends in pension provision. Accounting and Business Research 39 (3): 211–225.

Klumpes, P., Whittington, M. and Li, Y. (2009) Determinants of the pension curtailment decisions of UK firms. Journal of Business, Finance and Accounting 36 (7/8): 899–924.

Ali, A. and Kumar, K.R. (1994) The magnitudes of financial statement effects and accounting choice: The case of the adoption of SFAS 87. Journal of Accounting and Economics 18 (1): 89–114.

Klumpes, P.J.M. and Whittington, M. (2003) Determinants of actuarial valuation method changes for pension funding and reporting: Evidence from the UK. Journal of Business, Finance and Accounting 30 (1/2): 175–204.

Mittelstaedt, H.F. (1989) An empirical analysis of factors underlying the decision to remove excess assets from overfunded pension plans. Journal of Accounting and Economics 11 (4): 399–418.

Munnell, A.H., Golub-Sass, F., Soto, M. and Vitagliano, F. (2006) Why are Healthy Employers Freezing Their Pensions? Boston College Center for Retirement Research Issues in Brief 44.

Cahill, K.E. and Soto, M. (2003) How Do Cash Balance Plans Affect the Pension Landscape? Boston College Center for Retirement Research Issues in Brief 14.

Johnston, K., Hatem, J. and Scott, E. (2011) The cash balance plan as a real option: Financial innovation and implicit contacts. Pensions 16 (1): 39–50.

D'Souza, J., Jacob, J. and Lougee, B.A. (2004) Why Do Firms Convert to Cash Balance Pension Plans? An Empirical Investigation. Cornell University Working Paper.

Kapinos, K.A. (2009) On the determinants of defined benefit pension plan conversions. Journal of Labor Research 30 (2): 149–167.

In a publication of KPMG (‘De pensioenwereld in 2006’, October 2005) about 36 per cent of respondents mention to consider moving from a db to a cdc scheme within the next 5 years.

Hoevenaars, R., Kocken, T. and Ponds, E. (2009) Pricing risk in corporate pension plans: Understanding the real pension deal. Rotman International Journal of Pension Management 2 (1): 56–64.

Pension funds that make more prudent actuarial assumptions are allowed to use a lower solvency rate, but never below 100 per cent. Note that this solvency level is comparable to an accrued benefit obligation that the pension fund reports to the Dutch pension regulator and not the projected benefit obligation that is used in pension accounting for the sponsoring company. This 105 per cent is a minimum funding level and the Dutch regulator requires a risk-based target funding ratio that depends on the probability of underfunding within 1 year.

Tinker, T. and Ghicas, D. (1993) Dishonored contracts: Accounting and the expropriation of employee pension wealth. Accounting, Organisations, and Society 18 (4): 361–380.

Tinker and Ghicas25 describe the contracting costs that might be involved when companies breach implicit pension contracts with their employees (when mergers seem to be motivated to capture the pension accounting surplus).

Dixon, A.D. and Monk, A.H.B. (2009) The power of finance: accounting harmonization's effect on pension provision. Journal of Economic Geography 9 (5): 619–639.

The pensionable wage is defined as the actual wage minus a threshold that proxies for the level of state benefits. This threshold is bound by fiscal policy. As an example, consider a person earning €30 000 per year with a €15 000 proxy threshold; a contribution rate of 20 per cent would be €3000 or 10 per cent of the person's wage.

Reiter, S.A. and Omer, T. (1992) A critical perspective on pension accounting, pension research, and pension terminations. Critical Perspectives on Accounting 3 (1): 61–85.

Author's translation of a press release in Dutch by the ANP on 27 June 2005.

Author's translation from the semi-annual report (only available in Dutch).

Author's translation of a concept in Dutch for a collective labour agreement by labour union FNV Bondgenoten.

Thomas, J.K. (1989) Why do firms terminate their overfunded pension plans? Journal of Accounting and Economics 11 (4): 361–398.

Several studies indicate that the stock market has problem valuing pension agreements appropriately; Franzoni and Marin35 and Coronado et al.36

Franzoni, F. and Marin, J. (2006) Portable alphas from pension mispricing. Journal of Portfolio Management 32 (4): 44–56.

Coronado, J., Mitchell, O.S., Sharpe, S.A. and Nesbitt, S.B. (2008) Footnotes aren’t enough: The impact of pension accounting on stock values. Journal of Pension Economics and Finance 7 (3): 257–276.

Note that Swinkels3 describes the switch to defined contribution from 2 out of the 24 most liquid Dutch companies listed on Euronext. The two switching companies are Akzo Nobel and DSM.

We access annual reports from companies and pension funds through http://annualreports.info and http://pensionfund.info.

The maturity is measured by the number of participants and not the size of their pension claim. It is hard to say how the ratio would be influenced if we would take the size of the pension claim into account. Retired employees usually have substantial pension claims, but employees that left the company and did not convert their pension to their new employer might have only a small pension claim with the company.

Amir, E., Guan, Y. and Oswald, D. (2010) The effect of pension accounting on corporate pension asset allocation. Review of Accounting Studies 15 (2): 345–366.

Amir et al40 investigate the reverse causality. They indicate that pension funds increase their allocation to fixed income securities when pension accounting standards move towards fair valuation, both in the United States and the United Kingdom.

Haw, I.-U., Jung, K. and Lilien, S.B. (1991) Overfunded defined benefit pension plan settlements without asset reversions. Journal of Accounting and Economics 14 (3): 295–320.

Haw et al42 indicate that overfunded pension schemes may be settled because of accounting gains and that firms with declining earnings and restricted debt covenants are most likely to do so.

Acknowledgements

I thank the Network for Pensions, Aging and Retirement (Netspar) for financial support and Marleen Dijkstra for excellent research assistance. Parts of this article were written during a research visit to the Center for Retirement Research at Boston College. I also thank the participants of the 1st Accounting and Finance Conference in Thessaloniki and the 30th Annual Conference of the European Accounting Association in Lisbon for helpful comments.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Swinkels, L. Have pension plans changed after the introduction of IFRS?. Pensions Int J 16, 244–255 (2011). https://doi.org/10.1057/pm.2011.20

Received:

Revised:

Published:

Issue Date:

DOI: https://doi.org/10.1057/pm.2011.20