Abstract

This study aims to demonstrate the impact of renewable energy consumption (REC) on environmental degradation using the EKC hypothesis testing for the BRIC and G-7 countries. Two EKC models were created and tested, with Model 2 including REC and other independent variables such as economic freedom (EF) and economic policy uncertainty (EPU), which affect the level of renewable energy consumption and CO2 emissions. Empirical findings indicate that the EKC hypothesis is verified faster in the REC-EF-EPU-based EKC model (Model 2) than in the EF-EPU-based EKC model (Model 1) for G-7 countries since the turning point takes place earlier in Model 2 than in Model 1 with REC. This suggests that renewable energy consumption accelerates the reduction of CO2 emissions. Moreover, this earlier turning point results in lower environmental cleaning costs, less time vesting, and saving resources and money for G-7 countries. However, the study found no evidence supporting the EKC hypothesis for the BRIC countries.

Similar content being viewed by others

1 Introduction

The relationship between economic growth and the environment is a critical issue for achieving sustainable development goals since high levels of economic activity can lead to significant environmental problems that negatively impact sustainable development (Bongers 2020). To combat environmental issues without compromising economic prosperity and well-being, it is essential to analyze and understand the impact of economic growth on environmental degradation. Grossman and Krueger (1991) proposed a non-linear relationship between economic growth and environmental degradation, illustrated by the inverted U-shaped curve of the Environmental Kuznets Curve (EKC) in Fig. 1.

Environmental Kuznets Curve (EKC)

According to the EKC hypothesis, a rise in real GDP per capita initially leads to an increase in CO2 emissions in the first stages of economic growth due to the consumption of fossil fuels. Eventually, this leads to a decrease in CO2 emissions after a certain turning point due to the adoption of eco-friendly technologies, policies, and cleaner energy demand (Dinda 2004; Soytas and Sari 2009; Aslan et al. 2018; Destek and Sarkodie, 2019a; Dogru et al. 2019; Erdogan and Acaravci 2019; Kisswani et al. 2019; Isik et al. 2019a, b; Destek et al., 2020a; Destek and Sinha, 2020b; Ongan et al. 2020; Ongan et al. 2022, 2023; Ahmad et al., 2023, 2022, 2021a, b, c; Alvarado et al. 2021a, b, c, 2022a; Işık et al. 2020a, 2021a, b, 2022; Çetin et al., 2023; Jabeen et el., 2023). Therefore, the critical question is how countries can reach this turning point with a lower real GDP per capita and earlier. Delaying the turning point will increase the cost of environmental cleaning and time investments for countries. On the other hand, an earlier turning point means that economic growth policies based on real GDP per capita and energy policies based on environmental degradation (i.e., CO2 emissions) converge quickly and sustainably at a lower cost. Therefore, increasing renewable energy consumption is one of the factors that can accelerate the reduction of CO2 emissions. As studies have provided solid evidence for the positive relationship between fossil energy consumption and environmental degradation, the focus has shifted toward renewable energy consumption. Therefore, recent studies have examined the nexus between renewable energy consumption, economic growth, and CO2 emissions (Amoah et al. 2020; Ali et al. 2021; Alsanusi et al. 2022; Alvarado et al. 2022a, 2022b, c; Assi et al. 2021; Avci and Sarigul 2022; Baig et al., 2022; Deng et al. 2022; Fatima et al. 2022; Hussain et al. 2022; Jiang et al. 2022; Irfan et al. 2021; Pata and Işık, 2021; Kartal 2022; Rehman et al. 2022a, b, c; 2021a, 2021b, 2021c; Serttas et al., 2022; Yasir et al. 2022; Shahzad et al. 2021; Dogan et al. 2020; Dogru et al. 2020; Işık 2013; Işık et al. 2020a; Ongan et al. 2017, 2018a, b; Işık and Radulescu, 2017; Işık 2010; Bölük and Mert 2015; López-Menéndez et al. 2014).

Through EKC hypothesis testing, this study focuses on the importance of renewable energy consumption (REC) on environmental degradation. The study aims to determine if the EKC model with REC reaches the turning point earlier than the EKC model without this variable for the BRIC and G-7 countries. The study assumes that more economic freedom (EF) enables innovation and adopting eco-friendly technologies for more renewable energy consumption, but there is little research and mixed results on the EF-environmental degradation link. The study also considers changing economic policy uncertainty, measured by Baker et al. (2016) with the EPU index, which is significant for the renewable energy consumption- CO2 emissions link and influences investments in renewable energy (Romano and Fumagalli (2018); Jiang et al. (2019); Adedoyin and Zakari, (2020); Işık et al. 2020b, Wang et al. (2020); Adams et al. (2020); Aimer, (2021). However, investments in renewable energy have decreased globally in recent years, and the International Energy Agency (IEA) is concerned that this development may negatively impact on achieving established climate objectives (IEA., 2018).

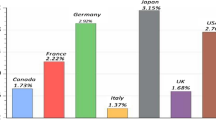

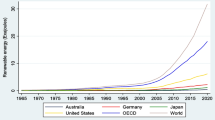

In this context, for testing the EKC hypothesis in the presence of independent variable renewable energy consumption (REC), we have built a REC-EF-EPU-based EKC model (Model 2). This model will be compared to Model 1 without REC as an EF-EPU-based EKC model. Furthermore, when we do this, we will examine all these relationships comparatively for the BRICS and G-7 countries, which have different EF, EPU, GDP, and CO2 emissions levels. Our sample countries groups are the BRIC (Brazil, Russia, India, and China) and G7 (Germany, France, the UK, Italy, Canada, the USA, and Japan) (see averages of the CO2 and GDP in Figs. 2, 3). In this context, this investigation will be between developed and developing economies.

Average CO2 in G7 and BRIC countries

Average GDP in G7 and BRIC countries

Given these observations, the novelty of this research lies in the comparative analysis between the G7 and BRIC countries and the gaps in the literature. Firstly, G7 countries were selected for investigation because their leaders significantly increased funding for nature by 2025 and mobilized substantial private finance to ensure faster net-zero emissions. On the other hand, BRIC states are among the world’s largest polluters, with an aggregated population of over 3 billion people, significantly contributing to global emissions. Recent studies have also indicated that energy consumption has the most significant long-term effect on the environment, making it the primary cause of pollution for BRIC states (Yilanci et al., 2020). The comparative analysis focuses on these two groups of countries since they share the long-term target of reducing pollution, despite having different patterns regarding pollution levels (BRIC countries contribute more to global pollution than G7 countries). Thus, the novelty of this research lies in demonstrating how renewable energy consumption can be a solution to decreasing pollution for both groups of countries. While many studies confirm the role of renewable energy in reducing environmental degradation (Khattak et al. 2020), none of them analyze this topic comparatively for G7 and BRIC states, clustering of countries with different pollution trends but with the same objective of mitigating climate change.

The rest of this study is structured as follows: Sect. 2 summarizes the literature review. Section 3 explains the empirical model, while Sect. 4 presents the estimation methodology. In Sect. 5, the findings are discussed, and finally, Sect. 6 presents the conclusion with the study’s policy implications.

2 Literature review

Many studies focused on the EKC hypothesis, including the independent variables of renewable energy consumption, economic policy uncertainty, and economic freedom, with very mixed results regarding the shape of EKC. For instance, Jebli et al. (2013) applied the Fully Modified Ordinary Least Squares (FMOLS) and Dynamic Ordinary Least Squares (DOLS) models. They found evidence for the EKC hypothesis in the presence of renewable energy consumption. Bölük and Mert (2015) applied the autoregressive distributed lag (ARDL) approach and found no evidence for the EKC hypothesis, but found an association between REC and CO2 emissions in Turkey. Bento and Moutinho (2016) applied the ARDL bounds testing approach to cointegration and verified the EKC hypothesis with the contribution of REC in CO2 emissions for Italy. Bilgili et al. (2016) applied the FMOLS and DOLS models and verified the EKC hypothesis with the support of REC in reducing CO2 emissions for the OECD countries. Jebli et al. (2016) applied the same methodology supporting the EKC hypothesis and found the same contribution of REC in reducing CO2 emissions for the OECD countries. Dong et al. (2017) used the panel unit root, cointegration, and causality tests, and validated EKC hypothesis for the BRICSFootnote 1 countries. They also found a significant negative relation between REC and CO2 emissions. López-Menéndez et al. (2014) examined 27 EU countries using panel data and proved the existence of the EKC hypothesis in the presence of REC. Danish et al. (2019) applied panel data estimation techniques to verify this hypothesis and found the REC’s contribution to the BRIC countries’ ecological footprint. Destek (2019b) applied the second-generation panel data methodologies and verified the EKC and REC’s contribution to CO2 emissions in Central and Eastern European countries. Işık et al. (2019a, b) used the common correlated effects estimator and validated the EKC hypothesis for 5 out of 10 US states. They also found a significant contribution of REC to CO2 emissions. Sharif et al. (2019) applied the heterogeneous panel estimations and verified the EKC. They also revealed the contribution of REC in 74 countries. Zhang et al. (2020) used the ARDL model and supported this hypothesis for developing Asian economies. They also found that renewable energy enhanced the trajectory rate of EKC. Erdogan et al. (2020) used the FMOLS and DOLS models and found evidence supporting the EKC hypothesis with REC for the OECD countries. Sun et al. (2020) used the Malmquist-Luenberger productivity index and verified the EKC with REC. Khattak et al. (2020) applied the common correlated effect mean group (CCEMG) technique. They found evidence supporting the EKC hypothesis in all BRICS countries and found the contribution of REC in CO2 emissions only in Russia, India, and China. The following papers found mixed results regarding the relationship between economic freedom and environmental degradation. Carlsson and Lundström (2001) used the pooled estimation method and found that increases in economic freedom led to decreases in CO2 emissions in low-income and high-income countries. Dasgupta et. al. (2006) applied the Hausman test for low-middle-upper-middle income countries. They found mixed results on the impact of economic freedom on CO2 emissions Wood and Herzog (2014) applied the two-staged model and found that increased economic freedom led to decreasing CO2 emissions. Hartwell and Coursey (2015) used a pooled OLS and a fixed-effects specification and found that economic freedom supports CO2 emissions in 292 countries. Bae et. al. (2016) used the GMM approach for 15 post-Soviet Union independent (PSI) countries and found that high economic freedom increases CO2 emissions. Joshi and Beck (2018) applied the Arellano-Bover/Blundell-Bond Generalized Method of Moments (GMM) estimator for 22 OECD countries. They could not find evidence supporting the positive contribution of economic freedom to environment. Adesina and Mwamba (2019) applied the GMM estimator for 24 African countries. They found that high economic freedom (proxied by the trade freedom index, business freedom index, freedom from corruption, and fiscal freedom index) increases environmental quality. Adesina and Mwamba (2019) applied the two-step system GMM methodology for 12 African countries. They found that increases in economic freedom improve environmental quality lowering CO2 emissions. Shahnazi and Shabani (2021) applied cross-sectional dependence and found evidence supporting the positive contribution of economic freedom to CO2 emissions in the EU area. The following papers found mixed results regarding the relationships between environmental degradation and the economic policy uncertainty (EPU) index. Jiang et al. (2019) applied a novel parametric test of Granger causality in quantiles for the USA. They found that CO2 emissions would rise, if EPU index increases. Ulucak and Khan (2020) applied the dynamic ARDL estimation and found that EPU determines the increase of CO2 emissions through the energy intensity effect in the USA. Abbasi and Adedoyin (2021) used the novel dynamic ARDL simulation model and could not find a significant relationship between CO2 emissions and EPU index in China. Adams et al. (2020) applied the Panel Pooled Mean Group Autoregressive Distributed lag model (PMG-ARDL) and found that policy uncertainty degrades the environment. Wang et al. (2020) applied the ARDL model and found that high economic policy uncertainty (measured by the World Uncertainty Index—WUI) leads to high CO2 emissions. Adedoyin and Zakari (2020) applied ARDL-bound testing and found no relationship between CO2 emissions and economic policy uncertainty for the UK. Ulucak and Khan (2020) used the dynamic ARDL approach and found that rises in the EPU index policy uncertainty adversely affect environmental quality. Anser et al. (2021), using a PMG (pooled mean group)-ARDL approach, found that EPU increases the world’s CO2 emission. Considering the relationship between population and CO2 emission, many scholars found that population growth increases CO2 emission. For instance, Zhang and Lin (2012) applied the STIRPAT model and found that population growth leads to high CO2 emission in China. Wang et al. (2013) used the STIRPAT (stochastic impacts by regression on population, affluence, and technology) for Guangdong Province, China, and found that population negatively impacts on CO2 emission. Wang and Zhao (2015) applied the same methodology and found the same results for China. Dong et al. (2018) applied the cross-sectional dependence and slope homogeneity tests for 128 countries and found that population negatively impacts on CO2 emission. Kim et al. (2020) applied the FMOLS model for South Korea, and proved that population aging reduces CO2 emissions. Regarding verification of the EKC hypothesis for the BRIC and G-7 countries, the following scholars found mixed results. For instance, Mohsen and Ali Rezaei (2013) applied the unit root tests and Kao panel cointegration test and found evidence supporting the EKC hypothesis for the BRICS countries. Chang (2015) applied the non-oriented DDF model and found that the EKC hypothesis is not verified for the BRICS and G-7 countries. Sinha and Sen (2016) used GMM methodology for BRICS and verified the EKC hypothesis only for Brazil and India. Zhou et al. (2019) applied the panel quantile regression model and studied the EKC hypothesis in G7 and BRICS countries. They found that the EKC hypothesis is validated only for G-7 countries. Sinha et al. (2019) used the unit root and cointegrations tests and could not find evidence supporting this hypothesis for the BRICS countries.

3 Empirical model

This study’s empirical approach is based on the following models (Models 1 and 2) without and with the independent variable REC. Model variables are in natural logarithmic forms:

where \(\alpha_{2}\) < 0,maximum (optimal) real GDP per capita level for Model 1 is calculated by GDP1 = exp (-\({\alpha }_{1}\)/2 \({\alpha }_{2}\)). In Model 1, \({CO}_{2}\) represents carbon emissions (metric million tons); \(GDP\) and \({GDP}^{2}\) are real GDP per capita and the squared of real GDP per capita, respectively (in USD); X is control variables: economic freedom (EF) index, economic policy uncertainty (EPU) index, and population (POP); \(e\) represents white noise error terms. The expected signs for \({\alpha }_{1}\) and \({\alpha }_{2}\) are to be positive and negative, respectively since rises in real GDP per capita will initially increase CO2 emissions and, eventually, decrease them after a certain (maximum) point implying the EKC hypothesis verification. Data were obtained from the World Development Indicators (2021), the World Bank Database, World Energy Agency, EPUFootnote 2 index, and EFFootnote 3 index. The empirical models are estimated with STATA 16. The sample period is 1996–2019 (See notations of relevant variables and their definitions in Table 1).

Following Eq. 1, we re-write our second model (Model 2) with the independent variable renewable energy consumption (REC) in the following form:

where \(\beta_{2}\) < 0,

The maximum (optimal) real GDP per capita level for Model 2 is calculated by GDP2 = exp (-\({\beta }_{1}\)/2 \({\beta }_{2}\)). The expected signs for \({\beta }_{1}\), \({\beta }_{2}\) and \({\beta }_{4}\) are the same as in Eq. 1, and for \({\beta }_{3}\), it is expected to be negative since an increase in renewable energy consumption (REC) leads to a decrease in CO2 emissions. When comparing both models, it is expected that renewable energy consumption will accelerate the reduction of CO2 emissions, resulting in an earlier turning point in Model 2 compared to Model 1. This implies that it will take less time to reach this point in Model 2 than in Model 1, assuming that real GDP per capita increases over time since the turning point occurs at a lower real GDP per capita level. Furthermore, the EKC trajectory of Model 2 is expected to be shorter than that of Model 1. It is also expected that the maximum real GDP per capita level (in dollars) for Model 2 (GDP2) to be lower than its level achieved for Model 1 (GDP1).

4 Estimation methodology

In the estimation methodology of the study, we will proceed with the analyses under the following sub-titles.

4.1 Preliminary tests for cross-section dependence, unit root and cointegration

Cross-sectional dependence is checked because the CO2 emissions in one country might be correlated with those in another. CD Pesaran’s (2004) test is used in this case because it is not affected by the small size of the sample, null hypothesis stating cross-sectional independence:

\(\rho_{ij}\)- pair-wise correlation coefficient of the errors

In the case of balanced panels, the statistic of CD Pesaran’s (2004) test is determined as:

\(T_{ij}\)- number of common observations for countries i and j

Under the hypothesis of cross-section dependence, the Breitung test is used to check for unit roots. For non-stationary data, the cointegration is tested based on Kao, Pedroni, and Westerlund tests.

4.2 Panel autoregressive distributed lag

The panel Autoregressive Distributed Lag model (panel ARDL) might also be used in case of no clear cointegration relationship. For Model 1 and Model 2, the ARDL model is represented as:

After parameterization, the previous equations are represented as:

where λ, λ′, λ′′, λ′′′ are short-run coefficients associated to lagged endogenous variable and explanatory variables. θ type coefficients refer to long-run coefficients for explanatory variables. The speeds of adjustment are given by \({\Phi }_{1i}\) and \({\Phi }_{2i}\). The pool mean group (PMG) estimator supposes homogenous long-run equilibrium across countries and heterogeneous short-run relationships. Countries’ gaps explain the heterogeneous short-run behaviour.

5 Empirical findings

5.1 Pesaran’s CD test

According to CD Pesaran’s test, the cross-section dependence is checked for almost all the variables in the BRIC and G-7 countries, excepting population growth and economic freedom index at a 5% level of significance (see Table 2).

5.2 Unit root and cointegration tests and coefficients of cointegration

According to the Breitung test that allows for cross-dependence, the panel data for all variables are stationary in the first differences in the BRIC and G-7 countries, which implies that the data in level are integrated of order 1(I(1)) (see Table 3).

Given the fact that the data for all variables are integrated in the same order, the cointegration relationship is checked using Kao, Pedroni, and Westerlund tests. According to Table 4, there is no cointegration relationship between variables at a 5% level of significance.

According to Table 4, there is mixed evidence related to the cointegration relationship in G-7 countries. The Westerlund test indicated no cointegration, while Kao and Pedroni’s tests suggest a possible cointegration. Hence, we can estimate the coefficients of the models (see also Table 5).

5.3 The pool mean group (PMG) and common correlated effects (CCE) estimator

To estimate the coefficients of Model 1 without REC and Model 2 with REC, we apply the pooled mean group (PMG) and common correlated effects (CCE) estimators developed by Pesaran et al. (1999) and Pesaran (2006), respectively. The PMG and CCE estimation results are reported in Table 6 and Tables 7 and 8, respectively.

Test results of Models 1 and 2 presented in Tables 6, 7 and 8, based on both the PMG and CCE estimators, indicate that the EKC hypothesis is verified only for G-7 countries since the BRIC countries’ coefficients are insignificant. Furthermore, we confirm that renewable energy consumption (REC) in Model 2 accelerates the reduction of CO2 emissions in the long run. This means the EKC hypothesis is verified faster in Model 2 (with a shorter EKC trajectory) than in Model 1, which didn’t include REC. It can be quickly reached to the maximum (optimal) real GDP per capita level with a lower real GDP per capita level since GDP in Model 1 is higher than GDP in Model 2. Additionally, while a rise in economic freedom (EF) mitigates CO2 emissions, a fall in EPU increases carbon emissions for both BRIC and G-7 countries in the long run. Higher policy uncertainty (EPU) reduces economic activity, which implies less pollution, but only in the long-run, not in the short-run. The population growth (POP) increases CO2 emissions in all countries. It should also be noted that the positive impacts of economic freedom (EF) on the environment in stronger for the BRIC countries than in G-7 countries, according to the PGM model. This can be interpreted that the G-7 countries already have more freedom than the BRIC countries (see rest of the analysis in Appendix).

6 Conclusion with policy implications

This study aimed to empirically prove the accelerating impact of renewable energy consumption (REC) on environmental degradation. In this regard, the EKC hypothesis testing was used for the BRIC and G-7 countries. It was expected that the EKC model with REC would accelerate the reduction of CO2 emissions. Therefore, two different EKC models were created and tested separately: Model 1 without REC and Model 2 with REC. Empirical findings of both the PMG and CCE estimators revealed that reaching the maximum (optimal) real GDP per capita level, took a shorter time (with lower real GDP per capita level) in Model 2 than in Model 1 for G-7 countries. This means that the EKC trajectory of Model 2 is shorter than in Model 1’s. The economic inferences of this shorter period (early turning point) for the governments mean lower environmental cleaning costs, less time vesting, and saving the resources and money. This also means that the economic growth policies based on real GDP per capita and energy policies based on environmental degradation (i.e., CO2 emissions) converge with each other quickly and sustainably at a lower cost. At this point, we should remind something one more time. To be able to use the terms “early or quick turning point” in the EKC models, we assumed that real GDP per capita rises over time. This must be a mathematically necessary assumption in the EKC models since it brings a time dimension to the EKC models.

Overall, the study found that renewable energy consumption plays an essential role in accelerating the reduction of CO2 emissions and it positively contributes to the environment. However, the EKC hypothesis could not be verified for the BRIC countries, indicating that their economic and energy policies may not be sustainable. This could be due to various reasons, such as the incorrect implementation of economic and energy policies and the low share of renewable energy consumption in their total energy consumption.

The study found that GDP growth, renewable energy consumption, and population significantly impact CO2 emissions in the long run in G7 countries, especially when renewable energy consumption is included in the model. On the other hand, the impacts of economic policy uncertainty (EPU) and economic freedom (EF) on CO2 emissions are weaker in G7 countries than in BRIC countries when renewable energy consumption is considered. However, when renewable energy consumption is excluded, all exogenous factors substantially impact BRIC countries more than G7 countries. Thus, it can be concluded that renewable energy consumption plays a crucial role in reducing CO2 emissions, particularly in G7 countries, and can contribute to improving economic freedom.

The main policy implication of this research is to show policymakers the importance and the accelerating impact of the renewable energy consumption for a cleaner environment. Moreover, the COVID-19 pandemic may force governments to invest more in renewable energy since it may strengthen resilience to protect people’s health Dogru et al. (2023), Karagöz et al. (2021, 2023). Promoting renewable energy sources should be done by supporting public–private partnerships in the RE area for investing in these RE sources and acknowledging the benefits of RE use for the population (Işık et al. 2017, 2018). In this regard, G7 countries, as developed economies, can allocate significant financial funds and design adequate regulations for supporting these public–private partnerships and research in the RE area. All the regulations elaborated by the authorities should promote economic freedom by not deterring investments in the RE area or not generating large disinvestments in the RE consumption area because of the worsening of the macroeconomic and regulatory context. This is especially true for BRICS countries that are developing economies. They don’t benefit from significant financial funds such as G7 countries, and the investments are more sensitive to the macroeconomic framework in the developing countries than in the developed economies. However, BRICS represent top emerging economies, and they made significant progress and strengthened their cooperation for joint projects in the renewable energy area. Russia and China have access to wind energy. South Africa, India, and Brazil use solar energy primarily, and Brazil also uses biomass, so all BRICS have significant resource advantages in the RE sector. Economic freedom should improve in BRICS countries to support economic progress and investments in the RE area. Environmental policy should consider policy uncertainty and economic freedom to achieve the CO2 reduction target. Our results suggested that a rise of policy uncertainty determines a decrease in CO2 emissions, causing the economic activity to shrink so that the pollution can decrease, but will not attract investors in the RE area either, which is detrimental to the environment in the long run.

This study can be followed by future empirical works that will use different methodologies for different countries. However, we believe that the further studies will support the motto of this current study “more renewable energy consumption, a cleaner environment, lower cost, and more time-saving.” From the empirical and methodological perspective, this will represent an “earlier turning point on the EKC or a faster EKC hypothesis verification.”

Data availability

The datasets generated and analyzed during the current study are available in the World Bank Indicator, Materialflows.net, World Intellectual Property Organization repository, http://data.worldbank.org and World energy Agency, Economic Policy Index and Economic Freedom Index.

Notes

BRICS countries are Brazil, Russia, India, China, and South Africa.

References

Abbasi KR, Adedoyin FF (2021) Do energy use and economic policy uncertainty affect CO2 emissions in China? Empirical evidence from the dynamic ARDL simulation approach. Environ Sci Pollut Res 28:23323–23335

Adams S, Adedoyin F, Olaniran E, Bekun FV (2020) Energy consumption, economic policy uncertainty and carbon emissions; causality evidence from resource rich economies. Econ Anal Policy 68:179–190

Adedoyin FF, Zakari A (2020) Energy consumption, economic expansion, and CO2 emission in the UK: the role of economic policy uncertainty. Sci Total Environ 738:140014

Adesina KS, Mwamba JVM (2019) Does economic freedom matter for CO2 emissions? Lessons from Africa. J Develop Areas 53(3):155–167

Ahmad M et al (2021a) Intention-based critical factors affecting willingness to adopt Novel Coronavirus prevention in Pakistan: implications for future pandemics. Int J Environ Res Public Health 18(11):6167

Ahmad M et al (2021b) Do inward foreign direct investment and economic development improve local environmental quality: aggregation bias puzzle. Environ Sci Pollut Res 28(26):34676–34696

Ahmad M et al (2021c) Heterogeneous links among urban concentration, non-renewable energy use intensity, economic development, and environmental emissions across regional development levels. Sci Total Environ 765:144527

Ahmad M et al (2022) Assessing long-and short-run dynamic interplay among balance of trade, aggregate economic output, real exchange rate, and CO2 emissions in Pakistan. Environ Dev Sustain 24(5):7283–7323

Ahmad M et al (2023) Households’ perception-based factors influencing biogas adoption: innovation diffusion framework. Energy 263:126155. https://doi.org/10.1016/j.energy.2022.126155

Aimer N (2021) Economic policy uncertainty and exchange rates before and during the COVID-19 pandemic. J Ekonomi 3(2):119–127

Ali S et al (2021) Evaluating green technology strategies for the sustainable development of solar power projects: evidence from Pakistan. Sustainability 13(23):12997

Alsanusi M, Altintaş H, Alnour M (2022) The role of real exchange rate in the trade balance between Turkey and Libya: evidence from nonlinear and wavelet-based approaches. J Ekonomi 4(2):46–56. https://doi.org/10.58251/ekonomi.1173205

Alvarado R et al (2021a) Ecological footprint, economic complexity and natural resources rents in Latin America: empirical evidence using quantile regressions. J Clean Prod 318:128585

Alvarado R et al (2021b) Heterogeneous impact of natural resources on income inequality: the role of the shadow economy and human capital index. Econ Anal Policy 69:690–704

Alvarado R et al (2022a) Biocapacity convergence clubs in Latin America: an analysis of their determining factors using quantile regressions. Environ Sci Pollut Res 29(44):66605–66621. https://doi.org/10.1007/s11356-022-20567-6

Alvarado R et al (2022b) Impact of natural resources on economic progress: evidence for trading blocs in Latin America using non-linear econometric methods. Resour Policy 79:102908

Alvarado R et al (2022c) Impact of the informal economy on the ecological footprint: the role of urban concentration and globalization. Econ Anal Policy 75:750–767

Amoah A, Kwablah E, Korle K, Offei D (2020) Renewable energy consumption in Africa: the role of economic well-being and economic freedom. Energy, Sustain Soci 10(1):1–17

Anser MK, Apergis N, Syed QR (2021) Impact of economic policy uncertainty on CO2 emissions: evidence from top ten carbon emitter countries. Environ Sci Pollut Res. https://doi.org/10.1007/s11356-021-12782-4

Aslan A, Destek MA, Okumus I (2018) Bootstrap rolling window estimation approach to analysis of the Environment Kuznets Curve hypothesis: evidence from the USA. Environ Sci Pollut Res 25(3):2402–2408

Assi AF, Isiksal AZ, Tursoy T (2021) Renewable energy consumption, financial development, environmental pollution, and innovations in the ASEAN+ 3 group: evidence from (P-ARDL) model. Renew Energy 165:689–700

Avci P, Sarigül SS (2022) Is the performance of the companies operating in the participation index in the Turkish economy affected by the macroeconomic perspective? J Ekonomi 4(2):3–3. https://doi.org/10.58251/ekonomi.1182456

Bae JH, Li DD, Meenakshi R (2016) Determinants of CO2 emission for post-Soviet Union independent countries. Climate Policy 17(5):591–615

Baig IA et al (2022) Addressing the effect of meteorological factors and agricultural subsidy on agricultural productivity in India: a roadmap toward environmental sustainability. Environ Sci Pollut Res 30(6):1–18

Baker SR, Bloom N, Davis SJ (2016) Measuring economic policy uncertainty. Quarter J Econ 131(4):1593–1636

Bento JPC, Moutinho V (2016) CO2 emissions, non-renewable and renewable electricity production, economic growth, and international trade in Italy. Renew Sustain Energy Rev 55:142–155

Bilgili F, Koçak E, Bulut Ü (2016) The dynamic impact of renewable energy consumption on CO2 emissions: a revisited Environmental Kuznets Curve approach. Renew Sustain Energy Rev 54:838–845

Bölük G, Mert M (2015) The renewable energy, growth and environmental Kuznets curve in Turkey: an ARDL approach. Renew Sustain Energy Rev 52:587–595

Bongers A (2020) The environmental Kuznets curve and the energy mix: a structural estimation. Energies 13(10):2641

Carlsson F, Lundström S (2001) Political and Economic Freedom and the Environment: the Case of CO2 Emissions Department of Economics. Goteborg University, UK

Çetin M et al (2023) The impact of natural resources, economic growth, savings, and current account balance on financial sector development: theory and empirical evidence. Resourc Policy 81:103300. https://doi.org/10.1016/j.resourpol.2023.103300

Chang MC (2015) Room for improvement in low carbon economies of G7 and BRICS countries based on the analysis of energy efficiency and environmental Kuznets curves. J Clean Prod 99:140–151

Danish MAB, Mahmood N, Zhang JW (2019) Effect of natural resources, renewable energy and economic development on CO2 emissions in BRICS countries. Sci Total Environ 678:632–638. https://doi.org/10.1016/j.scitotenv.2019.05.028

Dasgupta K, Hamilton K, Pandey D (2006) Wheeler, Environment during growth:accounting for governance and vulnerability. World Dev 34(9):1597–2161

Deng QS et al (2022) Asymmetric impacts of foreign direct investment inflows, financial development, and social globalization on environmental pollution. Econ Anal Policy 76:236–251

Destek MA (2019) Investigation on the role of economic, social, and political globalization on environment: evidence from CEECs. Environ Sci Pollut Res 27:33601–33614

Destek MA, Sarkodie SA (2019) Investigation of environmental Kuznets curve for ecological footprint: the role of energy and financial development. Sci Total Environ 650:2483–2489

Destek MA, Sinha A (2020) Renewable, non-renewable energy consumption, economic growth, trade openness and ecological footprint: evidence from organisation for economic Co-operation and development countries. J Clean Prod 242:118537

Destek MA, Shahbaz M, Okumus I, Hammoudeh S, Sinha A (2020) The relationship between economic growth and carbon emissions in G-7 countries: evidence from time-varying parameters with a long history. Environ Sci Pollut Res 27(23):29100–29117

Dinda S (2004) Environmental Kuznets curve hypothesis: a survey. Ecology Economics 49:431–455

Dogan E et al (2020) The use of ecological footprint in estimating the environmental Kuznets curve hypothesis for BRICST by considering cross-section dependence and heterogeneity. Sci Total Environ 723:138063

Dogru T et al (2019) The balance of trade and exchange rates: theory and contemporary evidence from tourism. Tour Manage 74:12–23

Dogru T et al (2020) The nexus between tourism, economic growth, renewable energy consumption, and carbon dioxide emissions: contemporary evidence from OECD countries. Environ Sci Pollut Res 27(32):40930–40948

Dogru T et al (2023) Employee turnover dynamics in the hospitality industry vs. the overall economy. Tour Manag 99:104783. https://doi.org/10.1016/j.tourman.2023.104783

Dong K, Sun R, Hochman G (2017) Do natural gas and renewable energy consumption lead to less CO2 emission? Empirical evidence from a panel of BRICS countries. Energy 141:1466–1478

Dong K, Gal H, Yaqing Z, Renjin S, Hui L, Hua L (2018) CO2 emissions, economic and population growth, and renewable energy: empirical evidence across regions. Energy Economics 75:180–192

Erdogan S, Acaravci A (2019) Revisiting the convergence of carbon emission phenomenon in OECD countries: new evidence from Fourier panel KPSS test. Environ Sci Pollut Res 26:24758–24771

Erdogan S, Okumus I, Guzel AE (2020) Revisiting the Environmental Kuznets Curve hypothesis in OECD countries: the role of renewable, non-renewable energy, and oil prices. Environ Sci Pollut Res 27(19):23655–23663

Fatima N et al (2022) Households’ perception and environmentally friendly technology adoption: implications for energy efficiency. Front Energy Res 10:830286

Grossman GM, Krueger A, (1991) Environmental impacts of a North American Free trade agreement. National Bureau of Economic Research Working Paper 3914, NBER. Cambridge MA

Hartwell CA, Coursey D (2015) Revisiting the environmental rewards of economic freedom. Econ Business Lett 4(1):36–50

Hussain I et al (2022) Using an asymmetrical technique to assess the impacts of CO2 emissions on agricultural fruits in Pakistan. Environ Sci Pollut Res 29(13):19378–19389

International Energy Agency, 2018. Global energy investment in 2017 fails to keep up with energy security and sustainability goals, July 17, 2018. Available at: https://www.iea.org/newsroom/news/2018/july/global-energy-investment-in-2017-.html

Irfan M et al (2021) Interventions for the current COVID-19 pandemic: frontline workers’ intention to use personal protective equipment. Front Public Health. https://doi.org/10.3389/fpubh.2021.793642

Işik C (2010) Natural gas consumption and economic growth in Turkey: a bound test approach. Energy Syst 1(4):441–456

Işık C (2013) The importance of creating a competitive advantage and investing in information technology for modern economies: an ARDL test approach from Turkey. J Knowl Econ 4:387–405. https://doi.org/10.1007/s13132-011-0075-2

Işık C, Kasımatı E, Ongan S (2017) Analyzing the causalities between economic growth, financial development, international trade, tourism expenditure and/on the CO2 emissions in Greece. Energy Sources Part B 12(7):665–673

Işık C, Dogru T, Turk ES (2018) A nexus of linear and non-linear relationships between tourism demand, renewable energy consumption, and economic growth: theory and evidence. Int J Tour Res 20(1):38–49

Işık C, Ongan S, Özdemir D (2019a) The economic growth/development and environmental degradation: evidence from the US state-level EKC hypothesis. Environ Sci Pollut Res 26(30):30772–30781

Işık C, Ongan S, Ozdemir D (2019b) Testing the EKC hypothesis for 10 US States: an application of heterogeneous panel estimation method. Environ Sci Pollut Res 26(1):10846–10853

Işık C, Ahmad M, Pata UK, Ongan S, Radulescu M, Adedoyin FF, Ongan A (2020a) An evaluation of the tourism-induced environmental Kuznets curve (T-EKC) hypothesis: evidence from G7 Countries. Sustainability 12(21):9150

Işık C, Sirakaya-Turk E, Ongan S (2020b) Testing the efficacy of the economic policy uncertainty index on tourism demand in USMCA: theory and evidence. Tour Econ 26(8):1344–1357

Işık C, Ongan S, Ozdemir D, Ahmad M, Irfan M, Alvarado R, Ongan A (2021a) The increases and decreases of the environment Kuznets curve (EKC) for 8 OECD countries. Environ Sci Pollut Res 28(22):28535–28543

Işık C, Ahmad M, Ongan S, Ozdemir D, Irfan M, Alvarado R (2021b) Convergence analysis of the ecological footprint: theory and empirical evidence from the USMCA countries. Environ Sci Pollut Res 28(25):32648–32659

Işık C, Ongan S, Bulut U, Karakaya S, Irfan M, Alvarado R, Rehman A (2022) Reinvestigating the Environmental Kuznets Curve (EKC) hypothesis by a composite model constructed on the Armey curve hypothesis with government spending for the US States. Environ Sci Pollut Res 29(11):16472–16483

Isik C, Radulescu M (2017) Investigation of the relationship between renewable energy, tourism receipts and economic growth in Europe. Statistika-Statistics Econ J 97(2):85–94

Jabeen G et al (2023) Role of energy utilization intensity, technical development, economic openness, and foreign tourism in environmental sustainability. Gondwana Res. https://doi.org/10.1016/j.gr.2023.03.001

Jebli MB, Youssef SB, Ozturk I (2016) Testing environmental Kuznets curve hypothesis: the role of renewable and non-renewable energy consumption and trade in OECD countries. Ecol Ind 60:824–831

Jebli MB, Youseff SB, Ozturk I, (2013) The environmental kuznets curve: the role of renewable and non-renewable energy consumption and trade openness, MPRA Working paper no: 51672

Jiang Y, Zhou Z, Liu C (2019) Does economic policy uncertainty matter for carbon emission? Evidence from US sector level data. Environ Sci Pollut Res 26–24:24380–24394

Jiang G et al (2022) Effect of agricultural employment and export diversification index on environmental pollution: building the agenda towards sustainability. Sustainability 14(2):677

Joshi P, Beck K (2018) Democracy and carbon dioxide emissions: assessing the interactions of political and economic freedom and the environmental Kuznets curve. Energy Res Soc Sci 39:46–54

Karagöz D et al (2021) Solo female travel risks, anxiety and travel intentions: examining the moderating role of online psychological-social support. Current Issues Tour 24(11):1595–1612. https://doi.org/10.1080/13683500.2020.1816929

Karagöz D et al (2023) Event motivation, subjective well-being, and revisit intentions during the second wave of the pandemic: moderating effect of affective risk about COVID-19 and perceived trust. Current Issues Tour. https://doi.org/10.1080/13683500.2022.2158787

Kartal MT (2022) The role of consumption of energy, fossil sources, nuclear energy, and renewable energy on environmental degradation in top-five carbon producing countries. Renew Energy 184:871–880

Khattak SI, Ahmad M, Khan ZU, Khan A (2020) Exploring the impact of innovation, renewable energy consumption, and income on CO2 emissions: new evidence from the BRICS economies. Environ Sci Pollut Res 27(12):13866–13881. https://doi.org/10.1007/s11356-020-07876-4

Kim J, Lim H, Jo H (2020) Do aging and low fertility reduce carbon emissions in Korea? evidence from IPAT augmented EKC analysis. Int J Environ Res Public Health 17(8):2972

Kisswani KM, Harraf A, Kisswani AM (2019) Revisiting the environmental Kuznets curve hypothesis: evidence from the ASEAN-5 countries with structural breaks. Appl Econ 51–17:1955–1868

López-Menéndez AJ, Moreno B, Pérez R (2014) Environmental costs and renewable energy: re-visiting the environmental Kuznets curve. J Environ Manage 145:368–373

MohsenAli Rezaei MA (2013) A panel estimation of the relationship between trade liberalization, economic growth and CO2 emissions in BRICS countries. Hyperion Econ J 1(4):3–27

Ongan S et al (2017) The effects of real exchange rates and income on international tourism demand for the USA from some European Union countries. Economies 5(4):51

Ongan S et al (2018) The asymmetric effects of exchange rates on the US tourism balances in the NAFTA countries: an application of the nonlinear ARDL approach. J Appl Econ Business Res 8(3):162–174

Ongan S et al (2020) Economic growth and environmental degradation: evidence from the US case environmental Kuznets curve hypothesis with application of decomposition. J Environ Econ Policy 2160–6544:1–8

Ongan S et al (2022) Retesting the EKC hypothesis through transmission of the ARMEY curve model: an alternative composite model approach with theory and policy implications for NAFTA countries. Environ Sci Pollut Res 29(31):46587–46599. https://doi.org/10.1007/s11356-022-19106-0

Ongan S et al (2023) Are economic growth and environmental pollution dilemma? Environ Sci Pollut Res. https://doi.org/10.1007/s11356-023-25698-y

Ongan S et al., 2018a. Testing the J-curve hypothesis for the USA: applications of the nonlinear and linear ARDL models. South-Eastern Eur J Econ, 16(1).

Pata UK, Isik C (2021) Determinants of the load capacity factor in China: a novel dynamic ARDL approach for ecological footprint accounting. Resour Policy 74:102313

Pesaran MH (2004) General diagonist tests for cross section dependence in panels. Mimeo, University of Cambridge

Pesaran MH (2006) Estimation and inference in large heterogeneous panels with a multifactor error structure. Econometrica 74(4):967–1012

Pesaran MH, Shin Y, Smith RP (1999) Pooled mean group estimation of dynamic heterogeneous panels. J Am Stat Assoc 94–446:621–634

Rehman A et al (2021a) An asymmetrical analysis to explore the dynamic impacts of CO2 emission to renewable energy, expenditures, foreign direct investment, and trade in Pakistan. Environ Sci Pollut Res 28(38):53520–53532

Rehman A et al (2021b) Carbonization and atmospheric pollution in China: the asymmetric impacts of forests, livestock production, and economic progress on CO2 emissions. J Environ Manage 294:113059

Rehman A et al (2021c) Estimating the connection of information technology, foreign direct investment, trade, renewable energy and economic progress in Pakistan: evidence from ARDL approach and cointegrating regression analysis. Environ Sci Pollut Res 28(36):50623–50635

Rehman A et al (2022a) Carbonization and agricultural productivity in Bhutan: investigating the impact of crops production, fertilizer usage, and employment on CO2 emissions. J Clean Prod 375:134178

Rehman A et al (2022b) Globalization and renewable energy use: how are they contributing to upsurge the CO2 emissions? A global perspective. Environ Sci Pollut Res 30(4):9699–9712. https://doi.org/10.1007/s11356-022-22775-6

Rehman A et al (2022c) Estimating interlinks of carbon emissions from transportation, industrialization, and solid/liquid fuels with economic progress: evidence from Pakistan. Int J Environ Sci Technol 20(2):1981–1996. https://doi.org/10.1007/s13762-022-04111-0

Romano T, Fumagalli E (2018) Greening the power generation sector: understanding the role of uncertainty. Renew Sustain Energy Rev 91:272–286

Serttaş A, Sarıkaya T, Ünğan E (2022) Sustainability as a communication policy created by the economic system. J Ekonomi 4(2):74–81. https://doi.org/10.58251/ekonomi.1167505

Shahnazi R, Shabani ZD (2021) The effects of renewable energy, spatial spillover of CO2 emissions and economic freedom on CO2 emissions in the EU. Renew Energy 169:293–307

Shahzad U et al (2021) Do environment-related policy instruments and technologies facilitate renewable energy generation? Exploring the contextual evidence from developed economies. Energies 14(3):690

Sharif A, Raza SA, Ozturk I, Afshan S (2019) The dynamic relationship of renewable and non-renewable energy consumption with carbon emission: a global study with the application of heterogeneous panel estimations. Renew Energy 133:685–691

Sinha A, Sen S (2016) Atmospheric consequences of trade and human development: a case of BRIC countries. Atmos Pollut Res 7(6):980–989

Sinha A, Gupta M, Shahbaz M, Tuhin S (2019) Impact of corruption in public sector on environmental quality: implications for sustainability in BRICS and next 11 countries. J Clean Prod 232:1379–1393

Soytas U, Sari R (2009) Energy consumption, economic growth, and carbon emissions: challenges faced by an EU candidate member. Ecol Econ 68(6):1667–1675

Sun H, Kporsu AK, Taghizadeh-Hesary F, Edziah BK (2020) Estimating environmental efficiency and convergence: 1980 to 2016. Energy 208:118224

Ulucak R, Khan SUD (2020) Relationship between energy intensity and CO2 emissions: does economic policy matter? Sustain Dev 28:1457–1464

Wang Y, Zhao T (2015) Impacts of energy-related CO2 emissions: evidence from underdeveloped, developing and highly developed regions in China. Ecol Ind 50:186–195

Wang P, Wu W, Zhu B, Wei Y (2013) Examining the impact factors of energy-related CO2 emissions using the STIRPAT model in Guangdong Province, China. Appl Energ 106:65–71

Wang Q, Xiao K, Lu Z (2020) Does economic policy uncertainty affect CO2 emissions? empirical evidence from the United States. Sustainability 12–21:9108

Wood J, Herzog I (2014) Economic Freedom and Air Quality. Fraser Institute, Canada

Yao S, Zhang S, Zhang X (2019) Renewable energy, carbon emission and economic growth: a revised environmental Kuznets Curve perspective. J Clean Prod 235:1338–1352

Yasir A et al (2022) Factors affecting electric bike adoption: seeking an energy-efficient solution for the post-COVID era. Front Energy Res 9:817107

Yilanci V, Bozoklu S, Gorus MS (2020) Are BRICS countries pollution havens? Evidence from a bootstrap ARDL bounds testing approach with a Fourier function. Sustain Cities Soc 55:102035

Zhang GG, Lin Y (2012) Panel estimation for urbanization, energy consumption and CO2 emissions: a regional analysis in China. Energy Policy 49:488–498

Zhang J, Alharthi M, Abbas Q, Li W, Mohsin M, Jamal K, Taghizadeh-Hesary F (2020) Reassessing the environmental kuznets curve in relation to energy efficiency and economic growth. Sustainability 12:8346

Zhou Y, Sirisrisakulchai J, Liu J, Sriboonchitta S (2019) Factors affecting carbon emissons in the G7 and BRICS countries: evidence from quantile regression. In: Integrated uncertainty in knowledge modelling and decision making: 7th international symposium, IUKM 2019, Nara, Japan, 27–29 Mar 2019, Proceedings 7. Springer International Publishing, pp 406–417

Acknowledgements

This study was supported by Anadolu University Scientific Research Projects Commission (BAP), under the grant no: 2206E062

Funding

Not applicable.

Author information

Authors and Affiliations

Contributions

Conceptualization: CI methodology: CI, MS Software: MS investigation, writing—original draft preparation: CI, MS, SO, MR, and ZY, writing—review and editing, CI, MS, SO, MR, ZY, AR, RA, and MA, supervision, SO all authors have read and agreed to the published version of the manuscript.

Corresponding author

Ethics declarations

Conflicts of Interest

The authors declare no conflict of interest. The authors declare that they have no known competing financial interests or personal relationships that could have appeared to influence the work reported in this paper.

Ethical approval and consent to participate

Not applicable.

Consent for publication

Not applicable.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix 1

Appendix 1

See Table 9.

All the GDP terms in polynomial specifications are significant, and output growth strongly impacts CO2 emissions in G7 and BRIC countries, as we can see in Table 6, too. However, there are different patterns in the case of RKC. A U-shaped relationship was obtained for BRIC countries. This result is similar to the finding of Yao et al. (2020) for six large regions and for 17 developed and developing countries from 1990 to 2014. On the other hand, an inverse U relationship was observed in the case of G7 countries.

See Table 10.

GDP terms are not significant for the quadratic model. There are two different patterns in the two groups of countries, confirmed by Table 7, too. The positive sign for the linear and cubic specification and the negative one for squared GDP indicate an N-shaped relationship between CO2 emissions and GDP in the case of G7 countries. On the other hand, BRIC countries present an inversely-N-shaped relationship. Since the GDP values for which the first derivative is null are not local extrema, there is an increasing relationship between GDP and pollution.

See Table 11.

In all the models for EKC, population growth has a positive but low impact on CO2 emissions. The same positive influence of population on pollution was observed by Liddle (2015) in the case of 80 countries in the period 1971–2011.

Robusness: other control variables

The robustness of the results is checked by adding other control variables. For example, in the case of EKC, we added economic freedom and economic policy uncertainty in logarithms.

Table 8 shows similar results regarding the relationship between GDP and CO2 emissions. The speed of adjustment is more than double compared to the basic models. In G7 speed of adjustment is 55.6% in the case of G7 countries for RKC and 43.8% for the same group in the case of EKC.

According to Tables 8 and 9 in the RKC, economic freedom has a negative impact on CO2 emissions for BRIC countries and a positive one for G7 countries. On the other hand, a higher economic policy uncertainty reduced pollution in both groups of countries.

See Table 13.

Table 10 confirms the N-shaped relationship for BRIC and the inversely N-shaped one for G7 countries. These results show that in BRIC countries, economic growth is associated with an increase in pollution, while in G7 countries, it is possible to have economic growth with fewer CO2 emissions.

See Table 14.

The negative impact of economic freedom on pollution might be explained by the progress in the transition to environmental-friendly industries in BRIC. However, more efforts are required to ensure sustainable growth. Moreover, higher policy uncertainty reduces economic activity, which implies less pollution.

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Işık, C., Simionescu, M., Ongan, S. et al. Renewable energy, economic freedom and economic policy uncertainty: New evidence from a dynamic panel threshold analysis for the G-7 and BRIC countries. Stoch Environ Res Risk Assess 37, 3367–3382 (2023). https://doi.org/10.1007/s00477-023-02452-x

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00477-023-02452-x