Abstract

We propose a novel risk measure that is built on comparing high-frequency time-varying volatility and low-frequency return spillover estimates. This measure permits to identify the markets that are epidemic in their complex interdependence. We conjecture that initially a highly volatile market experiences episodes of risk transmission, but only later absorbs risk and becomes an epidemic market. Moreover, we can detect newly emerging ‘contagion’ in the system. We examine the behaviour of 30 global equity markets and compare spillover measures, which encapsulate many large and small crises episodes. Instead of relying on ex post crisis information, our model identifies crises periods. An important implication of the proposed approach is that highly interrelated markets, such as China, are less likely to transmit a global economic crisis under the current interdependence setting.

Similar content being viewed by others

1 Introduction

The multiple crises of the last two decades provide an ideal testing ground to identify systemic risks facing global equity markets. Understanding systemic risks using empirical tests on contagion, spillovers and financial networks has been a long standing research question. While the literature stretches back as early as King et al. (1994) on spillovers and Allen and Gale (1998) on contagion, the empirical literature on networks and financial spillovers is more recent. Allen and Gale (2000) and Gai and Kapadia (2010) evaluated network effects within the financial sector, while Acemoglu et al. (2015) showed how real economy shocks can become the source of crises that spread dramatically via financial interconnectedness as ‘fragility’, affecting otherwise ‘robust’ networks. Empirical representations show how the networks themselves change over time, between calm and crisis periods, and with the development and growth of emerging financial markets (Billio et al. 2012; Khandani et al. 2013; Demirer et al. 2018a). The changing nature of the links between those institutions can be considered a measure of contagion (Dungey and Gajurel 2015), while the links between spillovers and networks are highlighted in Diebold and Yılmaz (2014) via forecast error variance decompositions providing a single index of system’s vulnerability. This paper overcomes the limitations of the DY vulnerability index by highlighting vulnerability via newly proposed identification approaches using the signed return spillover index (Dungey et al. 2017b) complemented with a novel signed volatility spillover index.

We investigate risk transmissions in the global equity market using the Diebold and Yilmaz (DY) connectedness index,Footnote 1 the multivariate historical decomposition (MHD) index (Dungey et al. 2017b) and we propose a novel signed volatility decomposition (SVD) that helps extracting ‘contagion’ by identifying ‘excess volatility’ spillover matrices.

This paper makes several contributions into the literature. First, we propose a risk matrix that identifies sources of ‘contagion’. Then, we provide a rationale regarding the recent surge in speculation around crisis sources, and explore whether there is enough evidence aligning with these postulations. We examine if China is a potential source of crisis as suggested in Engle (2018), Akhtaruzzaman et al. (2021).Footnote 2 We produce evidence that it is unlikely that China is a source of financial contagion. Finally, we address some key questions that have long puzzled researchers. Can we identify excessively contagious markets out of sample taking into consideration their degree and dynamics of systemic connections? How different are contagion patterns in more recent times compared to earlier periods? Can we disentangle large contagion waves driving global economies towards a potential crisis? Identifying potential sources of ‘contagion’ and patterns underpinning contagious markets will allow regulators to take timely action attenuating the exposure of domestic markets to a large-scale crisis.

We also investigate changing dynamics in the risk transmission and in the resilience matrices, especially during the global economic slowdown as a direct result of Covid-19 pandemic.

A primary objective of this paper is to show that signed risk measures are better suited to model crises then popular DY risk measures. It examines market dynamics across all episodes of crisis and compare the derived signals with actual events juxtaposed against popular DY risk measures. Such comparison concentrates out the degree of misidentification if crisis modelling is reliant on a single framework, and more than one framework may not only complement each other’s findings but also reduce the gaps in the outcome. Hence, this objective addresses that running multiple important risk analysis frameworks simultaneously may have important implications in understanding both the degree and direction of crisis and in better modelling of crisis episodes. This is even more interesting as the global economies have significantly slowed down facing the Covid-19 pandemic. It warrants investigation if a Covid-19 pandemic and the economic downturn emerging in response have significant impact on systemic connections and how the popular DY model responses differently to the signed risk model.

A secondary objective of this paper is to detect excessively contagious markets in the past and newly emerging contagious markets using a single framework. A major gap in the extant literature is the effects of ‘interdependence’ are often enveloped within the potential effects coming from ‘contagion’ and as such are not well studied. This gives rise to a bias resulting from heteroscedasticity and often leading to failure in adopting a proper policy response to an imminent crisis. Interdependence bears less negative connotation compared to contagion, and the voluminous literature simply fails to incorporate major perspectives in crisis studies. This has resulted in an abundance of incomplete crisis examinations. Among the 124 papers reviewed in the taxonomy of Seth and Panda (2018), only 4 mention contagion, interdependence and integration.

Simultaneous increase in volatility facing a crisis is often wrongly attributed as resulting from contagion. It is because such amplifications in risks pertain to interdependence and overcast the effect of contagion for a particular market. An important significance of the current paper is that we propose a tractable novel approach that separates contagion effects out of effects due to interdependence, yet offers better crisis demarcation without prior knowledge on crisis.

More recently, Dungey and Renault (2018) relying on Forbes and Rigobon’s (2002) findings showed how to distinguish contagion from interdependence. Dungey and Renault (2018) suggested that swings in the volatility of common factors may transpire from reasons pertaining to ‘source’ or ‘target’ markets and may induce simultaneous volatility jumps. The evolution of innovations in one entity that is immediately reflected in another when a crisis does not precede and as such may not pertain to contagion. However, a crisis period co-movement in volatility requires careful exploration, as volatility in the common factor of a ‘target’ itself may overcast the effects coming from the ‘source’. In our work, we adopt a combined yet simpler approach considering the nexus between two issues and distinguishing markets with different levels of contagion.

In the current paper, we define ‘contagion’ as the difference between return spillover and realised volatility spillover. This allows us to identify if risks emanating from a market are purely due to a swing in the local volatility factor or if it is a response to a shock in the network. Moreover, ‘contagion’ identified in this approach allows us to separate out a long term ‘contagion’, and the dynamics for the ‘more contagious’ markets do not shift with every past, current and future crisis episode. Hence, allowing us a ‘contagion’ identification that does not require re-estimation with every crisis periods.

A novelty in our method is that crisis demarcation is not a necessary condition for contagion identification, unlike earlier methods. We do not need to concur with Forbes and Rigobon (2002) in knowing the crisis and calm periods to separate contagion from interdependence. We support the work of Dungey and Renault (2018) while progressing the current tenet by identifying the more contagious markets from the less contagious or not contagious markets with a single approach. This is a key contribution to the current literature investigating the real time evolution of contagion and, by extension, the early warning literature.

Our results also allow us to focus on the potential risks of crisis and the emergence of China as an important conduit market as outlined in a number of studies.Footnote 3

We identify the most crisis-prone markets and explain how the effect of innovations in these markets is different from the less crisis-prone markets. We examine the shock transmission dynamics in the global markets facing the Covid-19 pandemic.

Finally, five key arguments concerning the time-varying nature of systemic risk estimates leading to the detection of crisis transmission patterns are addressed. First, we examine whether policy interventions that restrict significant transmission paths help interconnected financial markets to deal with shocks. Second, we find that the changing interactions between markets result in changing patterns of shock spillovers. Third, we examine whether it is possible to detect which markets are more shock resistant in the sample period from 1998 to 2020. Fourth, we determine if a parametric signed identification approach can be used as an extension to the DY identification approach of return spillovers. Fifth, we examine if signed realised volatility identification approach can better identify ‘excess volatility’ in an interconnected system and help separating out excessively contagious markets.

The remainder of the paper proceeds as follows. Section 2 discusses a history of crisis episodes across the global equity market. Section 3 presents the empirical framework concerning GVD, static and dynamic networks, MHD and SVD. Section 4 outlines the dataset, consisting of 30 equity markets. This section also presents the filtering method and descriptive statistics on filtered data. Section 5 discusses the empirical results based on ‘system-wide connectedness’, before following on to the dynamic analysis and MHD measures explaining the effect of positive and negative shocks in the sample markets. We compare the results of MHD with SVD in this section. We discuss identifying ‘contagion’ and a subsection dedicated to ‘risk dynamics during Covid-19 pandemic’. Section 6 presents the conclusion to this paper.

2 Literature review

A key statement in the voluminous literature, which has generated several avenues of discussion regarding crisis control, is the heightening of integration resulting from modern globalisation, which is what causes contagion and systemic failures; see, for example, Atsalakis and Valavanis (2009), Bisias et al. (2012), Chinazzi and Fagiolo (2015), Benoit et al. (2017), Silva et al. (2017), Seth and Panda (2018).

It is important to understand that connectedness measures at large do not indicate risk transmission, but identifies the degree of systemic connections, in our case, across borders. Systemic risk transfer within borders may not lead to a full scale crisis, but risk transfer across borders, as Brunnermeier et al. (2016) suggested, may indicate a diabolic loop, or as highlighted in Farhi and Tirole (2017) a deadly doom loop creating a large scale crisis. While contagion measures may capture only the volatility spillovers as suggested in Masson (1998), Khan and Park (2009), Bekaert et al. (2013) that may emerge with large shocks spilling over onto the neighbours corresponding to an event, that is not likely be a systemic event (Dungey and Renault 2018). Hence, it is crucial to discuss the connection between systemic risk and financial contagion networks.

A second issue that has emerged from the extant literature is the imprecise identification of the constituents of a crisis (Romer and Romer 2015). What constitutes a crisis may range from asset price decline, bank run-on or, even institutional bankruptcies. In Silva et al.’s (2017) analysis of the systemic financial risk literature, a major issue found was the tendency to identify this phenomenon with banking crises (Silva et al. 2017). Further, Field (2003) found that this tendency was an underlying cause of many previously ineffective macroprudential responses, suggesting that macroprudential monitoring based on SIFI-centred risk identification only aggravated a systemic crisis. This concern is further reflected in the limited definition of systemic risk that the ECB (2009) produced as ‘one perspective is to describe it as the risk of experiencing a strong systemic event. Such an event adversely affects a number of systematically important intermediaries or markets’(p.134). It is important to detect the connections SIFIs and capital markets’ role in crisis generation.

We believe the issue of financial crisis require a balanced combination of arguments across streams of studies concerning financial crisis, financial contagion, systemic risk, equity and banking risk argument.

2.1 Contagion and systemic risk

Common shocks spilling out of origin and spanning across multiple sectors may build into a crisis. Systemic risks endowed within multiple sectors do not lead to cascade if there is no contagion and liquidity is well diversified. A pronounced rise in systemic risk may lead to credit risk transfer between sectors forming contagion. Contagion further exacerbates risk transmission as a conduit and a large-scale crisis may unearth. Systemic risk and contagion may go hand in hand in forming a crisis. A key issue in the current context is concentrating out the tipping point in shocks manifesting into crisis.

To understand this better, let us consider Allen and Carletti (2006) explaining risk transfer between banking and insurance sector that may or may not lead to crisis generation. Credit risk transfer between these two sectors is beneficial to welfare if there is uniform demand for liquidity, but is detrimental facing idiosyncratic risk. For crisis to manifest in terms of interdependence, the precept for both banking and insurance sector is to manage long- and short-term assets across different contingencies, despite operating differently. Also, let us consider two contingencies, when both sectors have common demand for liquidity against when the sectors do not have common demand for liquidity. In autarky, the sectors having no interplay subjects the insurance sector to systemic risk, but banking sector less so. For the case of banks having common demand for liquidity facing no idiosyncratic risk, credit risk transfer is beneficial for welfare. For the case of banks having common demand for liquidity, but apart from facing idiosyncratic liquidity risks, credit risk transfer may not remain beneficial. In both the cases, a crisis is not manifest despite the sectors reaching crisis points. Contagion acts as conduit for systemic crises across insurance and banking sector and back to insurance sector leading to Pareto reduction in welfare. In the context of incomplete markets and plunging asset prices, contagion across many illiquid markets leads to a worsening spiral, involving many financial institutions. However, market exposure to each other depends more on the strength of their own institutional and economic fundamentals. ‘Spillover’ and ‘contagion’ are coined to address excessive co-movements of asset returns preceding a crisis due to unidentifiable sources of shocks.

There is a significant increase in the number of studies centred around contagion.Footnote 4 However, only a fraction defines contagion and interdependence separately, and less so attempts to distinguish the terms empirically. This is partly due to a lack of tractable framework that does not require nesting of multiple methods. The hypothesis underpinning ‘Interdependence’ having a lesser negative connotation then ‘contagion’ or ‘systemic risk’, and as such are less conspicuous in empirical techniques. To postulate that we can gauge one without considering the other simply draws us further away from the objective of finding ways to fend off a crisis. Seminal work from Forbes and Rigobon (2002) distinguishes ‘interdependence’ and ‘contagion’, and proposes a widely accepted definition. Forbes and Rigobon (2002) suggests that in the case of two markets, countries or entities explicitly showing co-movements during calm periods will not be considered contagious despite amplifying co-movements and crisis engulfing both indices. It is contagion, when such co-movements are triggered facing a widespread crisis only. Key to this insight is the simultaneous volatility increases underpinning the increases in cross-correlation between factors. The bias is a result of heteroscedasticity and if untreated gives spurious identification. Hence, in all turbulence the gyrations in cross correlation index are erroneously dubbed as contagion. In similar spirit, albeit in a different framework Duffie et al. (2009) and Darolles and Gourieroux (2015) distinguishes frailty from contagion. This, in fact, explains why contagion identification is abound in the current tenet of studies. Earlier, the implications of such spurious identification of contagion are highlighted in Billio and Pelizzon (2003).

Piccotti (2017) argued that there exists a symbiotic relationship between contagion and systemic risk (financial contagion defines the spread of market disturbances and poses a potential threat for economies by attempting to integrate with international financial system. This also explains the extent to which a local crisis may propagate across neighbours and warrants investigation beyond real economic factors. Conversely, systemic risk suggests the risks that exist within a system of nodes comes from the strength of these nodes). Endogenous credit and capital constraints turn non-systemic risks into systemic risk as crisis propels through different markets followed by a reinforcing cycle. Additionally, crisis propagation brings about temporal changes to aggregate elasticity of temporal substitution affecting asset prices in different markets (Holmstrom and Tirole 1996, 1997; Kiyotaki and Moore 1997; Longstaff and Wang 2012; Elliott et al. 2014; Shenoy and Williams 2017). Hence, financial contagion increases all costs, as the marginal utility of consumption is negatively affected in the short term for long-term investors. Consequently, investors short-term holding time preference attributes a higher price to contagion (Van Binsbergen et al. 2012, 2013; Belo et al. 2015). Drawing a distinction, Piccotti (2017) suggested that financial contagion may positively affect the marginal utility of consumption corresponding to assets with a longer holding period, subsequently decreasing contagion costs while generating higher returns for risk-takers. Fernández-Rodríguez et al. (2016) define interconnectedness as a bridge between two crucial visions, ‘pure contagion’ and ‘shock spillover’. We are provided with an ideal natural experiment to investigate the degree to which existing systemic risk makes a given market more contagious. In other words, we aim to identify if high-risk spillovers are positively associated with spikes in contagion.

2.2 Banks or equity markets?

Notably, since the 2008 credit crisis several restrictions were imposed on banking securitisation, especially in advanced economies. The Association of Financial Markets in Europe reported significant reduction in the securitisation activities, especially for the USA and European banks (AFMEA 2017). Evidently, this has impaired the capital and profitability of these banks as indicated by for International Settlements (2018). Mersch (2017) presented an account of attempts to revive risk transfer in capital markets, especially in USA and European economies, by providing a natural experiment to recover the changes in the risk transfer dynamics for these economies.

The 2008 crisis has also driven the central banks to enforce both measures to enhance liquidity provisions and interbank loan freezes for commercial banks against the fear of an untenable build up and unwinding of systemic risk within the interbank loan networks (Georg 2013). Banks face a stochastic supply of deposits and interbank loans that link the banks, ensuring there is a continuing buffer of credit among them: this is the key to banking operations. While such static interbank loan networks form the money market, Haldane (2013) defined these interbank networks as robust, yet fragile, suggesting that interbank networks work on a knife’s edge. Moreover, static networks work well for maintaining liquidity provisions by enhancing liquidity allocation and risk share between depository institutions, and they are an intrinsic part in the globalisation of banks (Battiston et al. 2012; Ladley 2013; Gai and Kapadia 2010). Conversely, interbank networks amplify shocks for all participants and face the insolvency of a strongly connected participant. Acharya and Bisin (2014) defined such externality as a counterparty risk externality that fuels cascading defaults in banks, otherwise known as interbank contagion. Acharya and Bisin (2014) further suggests that a similar effect arises from one bank’s holding numerous other banks’ assets. A correlation externality arises when common shocks rip through all parties in an interbank loan market due to the common holding of sub-prime assets sourced from defaulting banks. Therefore, the fundamental banking activities are the source of untenable cycles of shock transmission, coupled with securitisation or shadow banking which provides a potential means for a downward spiral. However, the contribution of each participant disproportionately contributes to each trigger event and crisis propagation, and trying to gauge a generalised index of risk from these banks often leads to aberrations in outcomes. For more recent and important studies in this domain, we refer to Fry-McKibbin et al. (2021) and Bratis et al. (2020).

Allen and Gale (1998) presented an interesting perspective to explain the crucial link between banks and equity markets, and policy direction geared towards impeding the growth of crisis in both sectors. A classical view sources crisis from ‘mass hysteria’, in which investors’ panic due to an impending crisis is analogous to sunspots (Kindleberger 1978). These extraneous ‘sunspot’ panics emit from speculations and lead to self-fulfilling scenarios. Fearing a bank’s failure to fulfil its commitment leads to a synchronised withdrawal that drains the bank of liquidity, leading to bank failure and crisis precipitation. Alternatively, policies blunting the initial panic ensures there are few full withdrawals, resumes confidence in the bank’s commitment and dampens any further panic. Allen and Gale (1998) suggested that an ‘optimal allocation’ of risks is obtainable if bank runs are allowed within a controlled scenario. Banks shed risks into asset markets to stimulate cash flow. Facing a downturn, banks liquidate capital market assets that, in turn, forces asset prices down. Hence, if intervention strategies are simply geared towards preventing a capital market collapse, a Pareto improvement is observed in the banking sector, which satisfies the self-fulfilling prophecy. In this way, banking interventions can be a tool used to protect a few large banks from a cascade, and capital market interventions may protect the economy. In this regard, examining banking sectors for systemic risk-led crisis generation is investigating the wrong facet of the problematic.

This dichotomy is reflected in the tenet of studies identifying sources of crisis. The ubiquity of systemic stress across multiple sectors in the unfolding of a crisis makes it arduous to look for a unique sector reflecting the dynamics of crisis. Intuitively analysing the systemic banking connections identified by earlier studies has led to discourse in capturing the dynamics of boom-bust cycles. Evidently, there is strong interconnection between systemic risk propagation in banking and in stock markets. Myers (1977) asserted that fearing run-ons, banks naturally siphon off large, collateralised debts, which effectively devalues all common equities built into similarly constructed debt portfolios. A systemic decline in equity indices indicates widespread systemic banking declines. While investigating unprecedented losses in the long/short equity hedge funds during the USA quantitative meltdown of 2007 followed by coordinated deleveraging of equity market-neutral portfolios, Khandani and Andrew (2011) surprisingly found indications of macrostress building and shifting patterns in equity price expectations. Apparently, signs of distress across many sectors are more effectively gauged using equity market systemic risk analyses.

An increasing number of commentators give credence to this notion. Hanson et al. (2011) evinced that declines in equity indices are directly connected to forced liquidation of similarly constructed debt portfolios in the banking sectors. A resulting fire sale triggers a twin crisis, which then merges micro-level downturns into a complete economic downturn. Diamond and Rajan (2011), Shleifer and Vishny (2010) and Stein (2010) found unerringly positive similarities between equity market fire sales and bank credit crunches. In effect, classic bank run-on is indistinguishable from a stock market crash (Gorton and Metrick 2012; Covitz et al. 2009). Further, the rapid accumulation of credit bubbles spurs macroeconomic vulnerabilities and systemic connections in equity markets, which provides a perfect platform for modelling crisis (Dungey et al. 2020; Krishnamurthy and Muir 2017; Alan and Alexi 2014; Adrian and Shin 2009; Reinhart and Rogoff 2009).

Most recently, Syllignakis and Kouretas (2011) asserted that institutional investors shifting investment preferences from stocks and bonds to treasury bills, with the preceding investment withdrawal from institutional to investor-managed, emerging market hedge funds and private equity by investors as the USA subprime crisis unfolded exacerbated crisis transmission and contagion in the emerging Eastern European markets. Evidently, connectivity between emerging and European export dominant countries had resurfaced, especially with Germany, Russia, the UK and the USA (Syriopoulos 2007; Lucey and Voronkova 2008; Syllignakis and Kouretas 2010). This warrants a complete investigation into the shift of contagion preferably in equity markets.

3 Empirical framework

We apply DY, MHD and signed volatility decomposition (SVD) approaches to a large panel of international equity markets. The DY provides a profile of increasing spillover effects between the markets across the sample period, highlighting periods of change in the intensity for these effects. However, the DY is limited in identifying the direction of contemporaneous risk measures. MHD analysis enhances the DY by identifying linkages between markets that amplify or dampen shocks and, further, how the system of markets fluctuates around the average relationship by accumulating shocks over time. MHD helps discerning negative in-shocks from positive out-shocks with signs. SVD analysis complements MHD by calibrating the model with innovations from realised variance estimates put into an impulse response framework. For the DY analysis, we use a rolling window of 100 days. The results are robust to different rolling sample sizes and data frequencies.

The DY provides information on the direction and size of spillovers, while the MHD provides the direction, size and sign, that is, whether the linkages dampen or amplify shock transmission. We calibrate the MHD further by the estimating signed index with realised variances, and separate out the self-exciting transitory signed volatility evolution from the signed return spillovers with our proposed signed volatility decomposition (SVD). This approach can be considered as an extension of vulnerability and transmission representations with MHD.

3.1 Diebold and Yilmaz spillover index (DY)

Diebold and Yilmaz (2012) proposed a VAR forecast error variance decompositions (FEVD) to compute DY spillover indices. The FEVD matrix is termed as the adjacency matrix (or ‘connectedness matrix’). Across the rows and down the columns all possible connections between the VAR variables are represented by in-shocks to the targets and effects of out-shocks to potential recipients.

Consider a VAR(p) of the formFootnote 5

where \(x_{t}\) is the return vector \(x_{t}=\left( x_{1.t,\ldots .}x_{N.t}\right) ^{\prime }\), \(\varphi \) is a \(N\times N\) parameter matrix and \(\varepsilon _{t}\) represent residuals. The moving average representation of VAR(p) from (1) is

where,

Diebold and Yilmaz (2009) propose using the H-step-ahead forecast error variance decomposition (GVD) that is constructed from VAR (see Koop et al. 1996) to circumvent the order dependence issue. Following the work of Pesaran and Shin (1998), we denote this GVD by \(\theta _{ij}^{g}\left( H\right) \) and that gives

where the co-variance matrix is \(\sum \) and \(a_{jj}\) is square root of error variance of jth equation and in the ith element, \(A_{h}\) is the moving average coefficient from VAR and \(e_{j}\) is a selection vector of ones.

Now \(\sum _{j=1}^{N}\theta _{ij}^{g}\left( H\right) \ne 1\). However, after normalising, the rows in the FEVD matrix are defined as

in which we get \(\sum _{j=1}^{N}\tilde{\theta _{ij}^{g}}\left( H\right) =1\) and \(\sum _{i,j=1}^{N}\tilde{\theta _{ij}^{g}}\left( H\right) =N\).

The static spillover are computed by taking the sum of off-diagonal elements as proportion of sum of all elements, representing system wide connectedness. Notably, the directional spillover index identifies the return spillover of all other markets to market i

The return spillover from market i to the other markets is given by

Pairwise directional connectedness identifies gross shock transmission to and from the markets as

3.2 Multivariate historical decomposition (MHD)

MHD, pioneered by Dungey et al. (2017a), provides a signed contribution of shocks from one to another market that captures the dampening effects. Here, the connectedness elements measured with \(B_{ij}\) explain the fraction of variation of i due to shocks in j at time t (excluding self-loops in a network).

Building on the VAR defined in equation (1) the generalised historical decomposition of j at time t can be used to estimate a signed spillover index. This is presented as follows:

where \({\mathcal {E}}_{t+j-i}= \left[ \varepsilon _{t+j-i},...\varepsilon _{t+j-i} \right] \) is an \(N\times N\) residual matrix. IRFs’ are one unit impulse responses (non-orthogonalised) and \(\odot \) is the Hadamard product. The estimated MHD provides an \(N\times N\) matrix providing signed in-shocks across the rows and signed out-shocks down the columns of the matrix. This approach accommodates the nonlinear dynamics of the data.

MHD permits to estimate signed weights of shocks throughout the channels, as a function of impulse responses weighted by residuals \(\varepsilon _{t}\). The system uses unconditional variance estimates as innovations for the impulse response estimates and, as such, is considered to represent signed spillovers in the returns.

3.3 Signed volatility decomposition (SVD)

Now the SVD is proposed by extracting spillover information drawn from realised variances associated with volatility transmissions within a network. We take the difference between return and volatility spillovers to identify whether a particular market is driven more by intrinsic volatility than by risks emerging from the network.

Moreover, we consider a nonparametric approach to estimate SVD, which follows the same algorithm as MHD. Unlike MHD computed from daily returns, we compute MHD from realised variance drawing from 5-min intervals in prices and, as such, the historic decomposition is depicted as SVD.

We begin by calculating intraday log returns with \(r_{t,i}= \log (P_{t,i})-\log (P_{t,i-1}) \). Next, we compute squared returns for each 5-min interval and sum them up to find daily realised variances as

SVD is computed from using the estimates of \(\mathrm{RV}_{t}\) in Eq. (8). To identify contagion in the associated network from volatility of common factors localised to a given market we simply take the spread between SVD and MHD:

which is used in the empirical analysis section.

4 Data

The data are daily dollar denominated stock returns from 30 developed and developing countries’ markets across Asia–Pacific, Europe, the Americas and the Middle East.Footnote 6 The beginning of the sample corresponds to the Asian financial crisis period. Daily returns are generated from price indices for 1 January, 1998, to 15 June, 2020. Global economies endure 15 major crisis periods and several minor turmoils within the sample periods as outlined in Table 1.

Taking natural logarithms of the data, we transform price to returns data. We further use a two-day moving average filter, removing time zone effects as in Forbes and Rigobon (2002).

We use a balanced sample of 30 financial markets in this paper.Footnote 7 We classify the markets into export crisis (EC) markets (i.e. leaders in commodity export), oil exporters into both emerging (OEE) and developed (OED) markets, European markets that have been directly affected by the Greek crisis (GIIPS) of 2010 onwards and high-yield Asia–Pacific markets directly affected by the Asian crisis (AC) of 1997–1998. We also include in the OED group the so-called conduit markets of the USA and Japan (BIS 1998; Baur and Schulze 2005). Table 1 provides the classification of the markets into five clusters, which is a common presentation in the literature.

Table 2 provides a brief description of each of these events along with the broad dating conventions.

Discussions concerning properties of asset returns dominate in both the current and early literature. Among early studies, Fama (1976) suggested that daily asset returns series are more non-Gaussian than are shorter frequency return series. Additionally, Cont (2001) emphasised persistence and nonlinearity, while Stărică and Granger (2005) focused more on non-stationarity inherent within stock returns data.

Recently, Joseph et al. (2017) classified stock returns as non-Gaussian and time varying, with smooth compact support over low-frequency spectral content. Others suggested that the daily stock returns data are negatively skewed, nonlinear, noisy and volatile (Joseph and Larrain 2008; Atsalakis and Valavanis 2009; Joseph et al. 2011; Kremer and Schäfer 2016; Zhong and Enke 2017). It is crucial to use appropriate filtering and transforming techniques for better detection and decoding of cycles in source data.

Of the relevant studies examining prediction, Zhou et al. (2012) supported on the dissent in theory and practice regarding asset returns. Only the pre-possessing of returns circumvents such misalignment, as suggested by Joseph et al. (2016, 2017), Atsalakis and Valavanis (2009) and Zhong and Enke (2017). A central context of data pre-processing with filtering is there is no discord in its importance in the relevant studies investigating returns (Joseph et al. 2017).

Finally, Smith et al. (1997) suggested that despite its simplicity as a method, moving average filters do much better compared to other digital signal processing techniques, such as single pole. Precisely, moving average handles discrete time series in a subtle manner (Smith et al. 1997).

Within the context of considering raw returns as non-Gaussian, nonlinear, time-variant random data, the importance of spectrum density/frequency domain analysis for pre-processing is undeniable. Hence, moving average is the chosen signal processing technique here. On another note, ‘spectral windowing’ is important to extract detectable edges and avoid aberrations caused from discontinuity in the raw data. Naturally, the chosen window size is 2 in our paper, which is consistent with Oppenheim and Schafer (2014) and Forbes and Rigobon (2002).

The transform function

handles both infinite and finite impulse responses. The moving average filter derived from the rational transfer function allows input of different window size (ws)

Indeed, our pre-processed data characterised by the frequency contents of the signals better detect the periodicity than do the raw unprocessed returns data. Table 3 presents a selection of statistics for the 30 return indices; including average, minimum, maximum, standard deviation and Jarque–Bera test results for normality in distribution. The greatest spread between minimum and maximum is found for Venezuela, Kuwait and Iraq, all of which have high standard deviations. As is usual for returns normality is rejected at the 5% significance level. Rather, these indices have more leptokurtic and skewed distributions, consistent with the crisis effects throughout the sample period (Brown and Warner 1985; Fama and French 1988; Kim et al. 1991; Corhay and Rad 1994; Longin 1996). In addition to robustness tests with different rolling windows, we have examined the possibility of multicollinearity in residuals. We found correlation coefficients to be null and insignificant in the residuals, ruling out the possibility of loss of consistency in our estimation outputs.

In the following section, we present a comparison in the estimates gauged from DY, MHD and SVD. Note that, while DY and MHD estimates are computed drawing on data from the complete sample size from January 1998- June 2020, the MHD–SVD spread draws on from 5 min interval prices for September 2009 until September 2017.Footnote 8

5 Empirical results

In this section, we discuss the empirical results obtained from the DY, MHD and SVD methods (see Figs. 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13, 14, 15, 16, 17, 18, 19, 20 and 21). A detailed explanation of the amplifying and dampening transmissions and vulnerability is also presented in Tables 4 and 5. The empirics of the study covers multiple methodologies across multiple sample classifications. While a concise description of the observations from analysis is discussed, a more detailed comparative description for each methodologies across each sample classification is discussed in detail in Table 4 for risk transmissions and in Table 5 for risk receivings.

The analysis holds for two fundamental principles.

-

1.

First, a common phenomenon that largely holds is that big transmitters are generally more susceptible to global contagion shocks and that propagation of crisis with contagion is one-directional.

-

2.

Second, in identifying ‘contagion’ from an aggregate risk assessment, our economic prior is that for the markets in which locally induced volatility swings together with spillover, the increases coming from interconnection amplify the aggregate risk estimates, which reverts the market to a steady state by releasing excess risks onto others. Hence, in times of excess volatility, markets are more epidemic in nature.

Next, we discuss comparisons by market blocks (see Table 4): Asian crisis (AC), Export crisis (EC), Greek crisis (GIIPS), Oil exporting developed (OED) and Oil exporting emerging (OEE) countries’ markets.

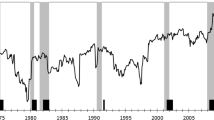

India, Singapore and Thailand in the AC cluster are highly susceptible to their own market shocks, but this holds less so for Malaysia, South Korea and the Philippines. While many past studies have contended (including our DY estimates) that Malaysia and the Philippines are more resilient for not being deeply connected to global networks as others (Raghavan and Dungey 2015), our MHD estimates further suggest the latter set of markets receive strong shocks in major events. As given in Figs. 1, 6, 11, 16 and 21, we suggest that the Indian, Malaysian and South Korean markets are more vulnerable to globally induced contagion than are the rest. The transmission estimates uphold this phenomenon by depicting these markets as low transmitters that are highly vulnerable to an epidemic in the holistic network. As Thailand, Singapore and the Philippines remain more susceptible to local volatility, unsurprisingly they emerge as strong transmitters as they release ‘excess volatility’ to other peripheries (see Tables 4 and 5). This ‘excess volatility’ refers to the accumulation of instantaneous self-exciting stochastic volatility in excess of volatility spillovers coming from the network itself.

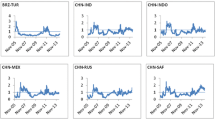

Simultaneous volatility changes in common factors with large-scale events often pollute the degree of actual spillovers as suggested in Dungey and Renault (2018). In Figs. 2, 7, 12, 17 and 21 we identify risks generated out of interconnections in the network from localised volatility changes for the EC (i.e. Germany, Chile, France, China, the UK and Australia) market cluster with MHD–SVD spread. We identify that Germany, Chile and the UK are predominantly more vulnerable to instantaneous transitory spikes in volatility, polluting the actual degree of shocks received from interconnections within the network. Consistent with the principle of high spreaders being less susceptible to vulnerability coming from a global contagion, the UK and France turn out to be high transmitters of crisis, especially during the GFC and eurozone crisis. For Australia, transmissions are triggered strongly with ‘excess volatility’ and, as such, it is highly vulnerable to epidemic shocks in the network. As opposed to Dungey and Renault (2018), who suggested Germany does not suffer from the same market reassessment risk as major markets and is distanced from other connections, we find Germany and China are highly susceptible to crisis received from other markets with ‘excess volatility’ most recently. Consequently, this indicates the degree of systemic risk found within these markets is due to contagion. At the onset of the Chinese and export crises, the heightened volatility in the German and Chinese market starts spilling excessive risks onto others, resulting in amplified transmission in the network as laid out in the second principle.

In comparing DY and MHD, we find MHD rejects DY’s depictions of Germany and France as the highest spreaders of crisis. Despite occasional spikes in resilience responding to major global events spanning our sampling periods, Germany remains more vulnerable to crisis coming from contagion than does France or the UK. While we may attribute the degree of transmissions coming from France as neutral to dampening, the UK is largely a spreader with strong resilience to contagion.

Figures 3, 8, 13, 18, and 21 depict that the GIIPS countries’ (i.e. Greece, Italy, Ireland, Portugal, Spain) markets are very sensitive to events contributing to global contagion. These markets are less characterised by local shocks and the shocks generated in the neighbouring nodes, except for Greece and Belgium. However, the MHD measure selects Greece and Austria as becoming more resilient as the eurozone crisis subsides, while Portugal and Ireland become more vulnerable. This can be attributed to investments moving out of Greece and Belgium and into Portugal and Ireland, making the latter deeply connected. Moreover, MHD captures Croatia remaining strongly resilient to shocks across the periods spanning our sample, which DY fails to detect.

Our transmission estimates for GIIPS countries and the transmission vulnerability mechanism are in line with what we provided in the first principle. As Portugal becomes more vulnerable to global contagion more recently, it is of no surprise to find that Portugal and Ireland transmit stronger shocks in the past. This suggests Portugal and Ireland remain deeply connected with the other peripheries since before the GFC. Moreover, with dropping vulnerability coupled with ‘excess volatility’, Croatia emerges as a strong transmitter during the eurozone crisis.

Figure 21 shows the volatility jumps unique to Greece and Ireland, in which the excess vulnerability also sets off network transmissions to other markets. In contrast, transmissions emerging from Portugal and Austria that correspond to excess vulnerability are coming from volatility and, hence, are short-lived. Notably, there is little risk of spillover over-identification for Belgium and Croatia.

The figures concerning OED countries’ (i.e. the USA, Canada, Russia, Norway, Japan and New Zealand ) markets depict that stochastic local volatility predominantly affects the vulnerabilities of the USA, Norway and Mexico (Figs. 4, 9, 14, 19, and 21). In fact, the recent degree of risks stemming from the USA and Russia is emanating mostly from ‘excess volatility’. In contrast, exceeding return spillovers following the onset of export crisis for Norway, Japan and New Zealand suggests these markets are especially contagious. The spread falls for Canada and, very recently, for Mexico, suggesting the spillovers in these markets are driven less by local volatility and more by their dominance in the holistic network.

Taking a more granular view with our MHD and DY comparison, the Japanese and New Zealand transmissions provide further reassurance as to the nature of these markets’ vulnerabilities. Japanese volatility transmission is depicted as contagion transmission, which corresponds with Japan emerging as a highly connected market out of its long-lasting economic stagnation in early 2000. Neutral to dampening volatility transmissions stemming from the USA, but also a curving up of its transmission swings with a shifting regime, gives credence to BIS (1998) suggestion that both the USA and Japan are ‘conduits’ for contagion transmission. Conversely, the upheavals in the global oil market influence the nature of New Zealand’s contagion, more so than for other global events.

Comparing DY and MHD estimates, we further find that the USA and Japan are more susceptible to contagion risk transmissions than to the degree of risks they transmit themselves. The exaggeration of risk susceptibility is overlain with risks transpiring within, especially for the USA and Japan. Moreover, dismissing what is gauged from DY estimates regarding Russia, MHD substantiates Russian resilience spanning across the entire sample period. Additionally, Russian transmissions pick up in all major events. To a much lesser extent, this holds true for Norway as well.

Finally, turning to OEE countries’ (i.e. Saudi Arabia, Israel, Iraq, Kuwait, Nigeria and Venezuela) markets, we conjecture these markets are not at all contagious by examining Figs. 5, 10, 15, 20 and 21. Although the countries in this cluster dominate the global oil market, an upheaval in the oil market increases market strength in these markets. Consequently, they demonstrate strong resilience in phases of price or supply shocks in the oil market.

In several occasions for the OEE cluster, DY estimates fail to produce convincing evidence that aligns with MHD. DY fails to capture the amplifications in vulnerability for Saudi Arabia corresponding to the advent of the GFC and the diminishing systemic risks emitting from Iraq. MHD captures this successfully. Further, more recently, DY fails to capture the increases in vulnerability for Venezuela, which is more sensible given the heightening of the Venezuelan economic crisis, but is depicted in the MHD curves. With MHD, we disentangle the spikes in volatility transmissions for Kuwait, which naturally responds to the Iraq invasion and oil supply shock. In both cases, confidence build-up occurs dramatically in the Kuwait market. Again, DY fails to capture the dampening of Nigerian systemic risk transmission with the oil price crash following the Iraq invasion. On balance, we provide evidence of MHD better capturing larger effects on the economy than DY.

In Sects. 5.1 and 5.2, we discuss the insights into a global economic crisis facing the Covid-19 pandemic. The insights are generated using proposed methods in the current paper, and we provide a rationale regarding the recent surge in speculation around china as a potential crisis source and explore whether there is enough evidence aligning with these postulations. Due to the strong connection between speculations around these areas of discussion, it is reasonable to argue that our models simultaneously focus on the following two related areas of study.

5.1 Covid-19 and crisis transmission

The Covid-19 trends are nested with parent risk dynamics presented in Figs. 1, 2, 3, 4, 5, 6, 7, 8, 9 and 10. From the DY dynamics, spikes emerge during June 2019 financial year for India, Malaysia and Thailand that dampens in June 2020. The Philippines transmission is consistently high since 2018, which has also slowed down recently. The South Asian crisis markets show extreme vulnerability since 2018 that has spiked again recently. South Koran transmission was relatively controlled, while it remained highly vulnerable. However, MHD demonstrates a consistently high transmission from South Korea, as opposed to DY. This unveils an increasingly risky South Asian market dynamics since 2018.

In contrast, as we shift our attention to global exporters, DY shows China remaining both high transmitter of shocks and yet the most vulnerable, similar to France. While Australia and the other major global exporters demonstrate a dampening shock transmission, vulnerability spikes since the beginning of the 2020 financial year. With MHD analysis, we uncover that China and Germany show negative vulnerability in the 2020 financial year. On the other hand, UK and Australia both exhibit a spike in both transmission and vulnerability to shocks from other stock markets.

Turning to GIIPS, interestingly, with DY we identify vulnerability drops for all except for Italy, while Greece and Ireland remain the highest transmitter of shocks in the most recent years. MHD detects a recent positive spike in vulnerability for Greece and Ireland, while significant positive spikes in vulnerability for Portugal and Spain are detected with MHD.

With DY, the developed markets demonstrate increasing vulnerability, that is especially true for the USA, Norway and Japan in 2020. In contrast, Russian resilience increases significantly during the same time. However, the results do not change with MHD for Japan. However, The USA and Canada depict a dampening in vulnerability in 2020 fiscal year and a decreasing Russian resilience.

The Middle eastern markets, especially the Saudi Arabia, Venezuela and Kuwait, show similar trend to the South Asian markets with DY, which demonstrates increasing vulnerability. Interestingly, with MHD, we detect negative vulnerability for the markets in Saudi Arabia, Kuwait and Iraq, with strong transmissions from these markets.

Overall, the markets mentioned above do not show aberrations to their risk transmission patterns identified prior to the grisly economic reality emerging with the Covid-19 scenario. Therefore, a drastic change in ‘contagion’ transmission dynamics is not expected. A detailed transmission and vulnerability pattern for the above markets can be found in Tables 1 and 2.

5.2 Identifying ‘contagion’

A key contribution of the current paper is ‘contagion’ identification in the pool of markets from interconnection, for which crisis demarcation is not a necessary condition. While all interconnections and amplifications in the systemic risk that is found within this sample markets do not lead to contagion, contagion poses the unique threat of a financial pandemic. Hence, contagion is a necessary condition for a widespread crisis to ensue. We propose a tractable and simple technique to identify excessively contagious markets while the condition remains dynamic. Thus, a key question at this stage is, ‘How diabolic is a contagious market today compared to the past?’ In other words, are we going to experience a global meltdown similar to that of the GFC if a crisis is triggered from a contagious market?

From Fig. 21, we separate out Singapore, China, Australia and Japan as more contagious markets than the rest, especially in more recent times. Despite observing that the 2016 Chinese stock market crash sends shocks tumbling globally, the carnage is not as pronounced as in the GFC.

The models presented here shows that the Chinese stock market crash unfolding in January 2016 sets off a global rout, dragging down the stocks across the USA, Germany and rest of Europe and Brazil to 2 to 3%. Chinese economic growth plunges to 25-year low. Leading up to this, speculations and warnings reflected engendered fears of a global meltdown, including warnings issued by the International Monetary Fund (Mauldin 2017; Liang 2016; Mao 2009; Elliott 2017; Cheng 2017). The Chinese authority responded by imposing new trading curbs and devaluing currency. While commentators, including the China Securities Regulatory Commission, blamed surging speculation and irrational investment behaviour for sourcing the crisis, Mao (2009) suggested that the colossal shadow banking industry was responsible for heightening the risks in the Chinese markets much earlier. Presumably, potential risks are predominant in the shadow banks in China, which have quadrupled at an annual rate of 34% since 2008, and at that time the size of the Chinese shadow banks (US $8 trillion) is equal to 4.3% of Chinese GDP (Mao 2009). Liang (2016) asserted that the burgeoning shadow economy, amidst the goal of boosting productivity against an overall drop in the labour market, posed a high risk to the financial stability of China given its current regulatory framework.

We do not experience a replay of the 2008 GFC. Recently, Dungey et al. (2020) provided evidence of no new systemic crises emerging from China to other global markets given the resurgence in systemic risk. While our study purports to identify sources of crisis, the case for China is particularly interesting. Generally, the results capture a unique case of shadow banking and securitisation. There is a plethora of studies showing bank securitisation leads to higher systemic risks, while increasing bank profitability and ensuring a buffer of liquidity for the bank (Adrian and Shin 2009; Uhde and Michalak 2010; Nijskens and Wagner 2011; Nadauld and Weisbach 2012; Georg 2013; Battaglia et al. 2014; Bakoush et al. 2019). Although securitisation allows banks to shed their own idiosyncratic risks into financial markets and confirms a buffer of liquid assets coupled with higher profitability, a vicious cycle forms as banks’ exposure to credit risk intensifies. The shadow banking industry is evolving to retain risks while pursuing regulatory arbitrage by means of retaining rollover risks pertaining to maturity mismatch. These pose a significant threat for the sponsors assuming these risks. In effect, conduits are attributed with systemic risk involving commercial banks, insurance institutions and equity market components. This also explains the USA or other advanced markets posing no significantly new threat in recent times, partly because the post-2008 credit crisis saw several restrictions imposed on banking securitisation, particularly in advanced economies. The Association for Financial Markets in Europe (2017) reported a significant reduction in securitisation activities within 10 years, especially for the USA and European banks. Evidently, this has impaired the capital and profitability of these banks, as suggested by the Bank for International Settlement (2018).

Moreover, we do not observe a re-emergence of global meltdown from China or other contagious markets because of the structural differences between cross-border capital diffusion to what was occurring with the USA during the GFC. Shirai and Sugandi (2018) reported that Hong Kong, Japan and Singapore are the major financiers of cross-border capital in the Asia–Pacific economies. While Singapore has the largest financial centres and is also the largest equity investor to the People’s Republic of China (PRC), Japan, Republic of Korea (ROK), and others in the Association of Southeast Asian Nations, Japan invests largely in Australian debt securities. Conversely, Hong Kong invests mostly in the equities issued by the PRC.

Issuing US$3.5 trillion cross-border portfolio assets, Japan’s exposure to the Asia– Pacific region is mostly through Australia (US$572 billion) and vice versa. Despite this, the Asian Bond Funds administered and managed by banks for international settlement exclude Australia, Japan and New Zealand. The Asian Bond Funds ABF1 and ABF2 were introduced to develop the sovereign and quasi-sovereign bond markets dominated by the USA dollar and local markets, respectively. However, these countries are the main pathway for the USA and EU to invest in the region. Hence, 60% of the total shares issued in the USA and EU forms the cross-border portfolio for Japan, Australia and the ROK in the region establishing a strong bridge between the continents. Singapore is the largest investor in shares issued by the USA and EU. While the cross-border portfolio assets of Hong Kong, China, sum up to US$1.1 trillion, its portfolio shares mostly concentrate on the PRC (50%) followed by the Association of Southeast Asian Nations-5 (37%). The USA and EU shares constitute only 24% of the cross-border portfolio trading in Hong Kong, China. Hong Kong invests US$404 billion in the PRC-issued shares, compared with US$235 billion by Japan and US$218 billion by Singapore. Hong Kong has only US$99 billion invested in USA assets and US$165 billion invested in EU assets. In contrast, Australian foreign assets include 42% USA-issued securities, with only 26% from the EU (Shirai and Sugandi 2018).

In terms of cross-border portfolio liabilities, 73% of Japan’s total cross-border portfolio liabilities (US$1.7 trillion) are financed by the USA and EU, while the USA and EU finances 33% and 29%, respectively, of total liabilities of Australia (US$966 billion). Interestingly, while the USA and EU finances 66% of the total cross-border portfolio liabilities of Hong Kong (US$390 billion), Hong Kong finances 42% of the total liabilities of the PRC (US$710 billion). As a net debtor of cross-border portfolio investments to the world, Australia remains highly exposed to the USA and EU, which account for over 70%. Since 2001, for Japan, Australia also remains its biggest investment destination, increasing investing into Australia by four times (US$118 billion) in the post-GFC. The foreign portfolio asset and liabilities of Hong Kong and Singapore exceed that of Japan in the post-GFC, and for Hong Kong these grow by 157% and 142%, respectively (Shirai and Sugandi 2018).

In summary, as highly contagious markets, Japan and Singapore are not causing widespread crisis, as no crisis is revealed in these markets, or in the USA or EU in more recent times. In fact, the restrictions applied in the USA securitisation induce calmness in these markets. Hence, we are also observing calmness in the Australian markets. However, given the degree of exposure to each other and connectivity between these markets, a large enough shock in any of these markets may destabilise the other. In contrast, Hong Kong, China, concentrates investments mostly in the PRC. As both the economies are part of the PRC, this creates a closed-circuit transmitting wealth within. This is also a reason why the 2016 crash was absorbed mostly within the circuit and did not turn diabolical, despite having all the potential. In fact, this allows the central Chinese authorities to apply new restrictions, such as short selling bans or bans on stock investments as appeared in 2015, without inciting a global response.

6 Conclusion

In this paper, we have identified excessively contagious and more volatile markets relying on time-varying systemic risk in an associated network of markets. We began by exploring the transmission of risks and vulnerability to risks spanning across the sample period of nearly 20 years with DY return measures (DY), a well-known method proposed by Diebold and Yilmaz (2012). Next, we estimated return spillovers with signed spillover measures computed with MHD proposed recently by Dungey et al. (2019) and concluded that signed spillover measures capture all or more information than DY spillover measures. Third, we estimated signed volatility transmissions and vulnerabilities computing from MHD and drew on realised variances from 5-min intraday returns. Finally, we plotted the differences between time-varying volatility and return spillover estimates, which showed the markets that are epidemic in the complex network structure and the markets that are endemic in nature but predominantly volatile with a higher core volatility. Hence, we have addressed the issue of over-identification in the degree of systemic risk, which the markets emit in calm and crisis periods

We found that misidentification of contagion issues is prevalent when explaining risk transmissions and the build-up of market resilience across time with the DY spillover method only. We addressed these issues by re-estimating systemic risks with MHD. In the absolute representation of time-varying DY spillover measure, we found that DY spillover overestimates the level of actual resilience building for South Korea, the Philippines, Singapore, Germany, China and Israel. This measure also overestimates the degree of risk transmissions coming from Iraq, Venezuela, the USA (prior to the GFC) and, more recently, Nigeria and Greece. While the DY underestimates Greek, Croatian and Russian resilience building in recent years, it also underestimates the risks emanating from Kuwait, South Korea and Germany. Severe changes in market micro-structure corresponding to profound economic degradation is rather misrepresented as resilience building with DY for its absolute representation of spillovers. We found this holds for both Iraq and Venezuela. The signed spillover estimates captures the convergence in the swings of systemic risks as the economies in both the countries collapse.

We showed the separated influence of stochastic local volatility as opposed to the actual degree of systemic risks within a market. First, a market is not likely to be transmitting shocks and remain vulnerable at the same time. Moreover, during high-risk transmissions, markets turn more resilient or vice versa. However, it is more likely that high transmissions lead to a phenomenal increase in vulnerability for the market to negative in-shocks transpiring within the network. Second, in the amplification of total risk generation with the accumulation of self-exciting intraday local volatility added to systemic risks coming from the network, markets respond by casting off ‘excess volatility’ onto others. In other words, it is likely that a highly volatile market gives strong episodes of risk transmission at the start of an event without becoming an epidemic market. Nevertheless, such spikes may accompany a fall in the local market, as outlined in Bates (2019).

Complementing the work of Dungey and Renault (2018), our technique identified the degree of systemic risks free of simultaneous volatility increases accompanying a rise in volatility in common factors and may have various contributions to the field of economics and machine learning. First, it may enable managers of risk to better rebalance portfolios, parsing information concerning epidemic and non-epidemic elements in the portfolio. Supervisors may find it useful to understand risks coming with big links, and to target issues amplifying risks. Machine-learning enthusiasts may find it interesting to feed forward networks of markets scaled with proper degrees of systemic risk indices. Further, Bayesian priors can be generated weighted with amplifications and dampening in signed risk estimates, and predictability of market risks can be improved. In all, the methods combined not only serve a purpose by producing comparisons, but produce better information regarding a market’s susceptibility to realised crashes and volatility evolution.

We attempted to explore complex market associations spanning across the last two decades, encapsulating major global events across many markets including the ongoing global economic crisis as a direct result of Covid-19 pandemic. The markets were selected to represent dynamic shifts that each subsequent event provides and were then grouped into a closed system. As with the precursors of systemic risk studies, limitations arose from the limited intraday data availability for the Middle Eastern markets. However, we substituted with additional markets that depicted a similar pattern. Alternatively, a target should be an investor sentiment analysis corresponding to risk patterns, leading to a better understanding of strong amplifications in risk propagation.

Notes

In Akhtaruzzaman et al. (2021), the authors produce evidence of China transmitting contagion to South Asia compared to the USA, considering trade intensity, economic downturns, and negative net equity capital outflows influencing dynamic conditional correlations (DCC) between US/Chinese and South Asian financial stock returns. However, Syriopoulos et al. (2015) disputes efficacy of DCC models quoting that, ‘despite the attractive properties of the DCC model, empirical estimation and interpretation can be seriously constrained by complexities due to excessive parameter requirements, biased estimates and convergence limitations over the estimation process, especially whenever additional exogenous variables are introduced into the conditional mean and variance specifications’.

Seth and Panda (2018) produces a taxonomy of contagion that spans the articles publishing from 1990 till 2015, encapsulating 151 papers among which only 4 concentrates on contagion, spillover and integration nested together.

An intercept is suppressed for simplicity and without loss of generality.

The data are sourced from Thompson Reuters, and we follow the mnemonics indexed in Pukthuanthong and Roll (2009).

Australia, Austria, Belgium, Canada, Chile, China, France, Germany, Greece, Italy, India, Iraq, Ireland, Israel, Japan, Kuwait, Malaysia, New Zealand, Nigeria, Norway, Portugal, Russia, Saudi Arabia, Singapore, South Korea, Spain, Sri-Lanka, Thailand, the Philippines, the USA and the UK.

Due to the limited availability of 5-min interval prices for important South Asian countries, such as Singapore, we trim the data down to fit vector sub-spaces within the specified matrix space, for all other vectors retaining Singapore. For similar reasons, we also remove Middle Eastern markets. We include Mexico in the sample, as it represent an important, emerging oil exporting market. We do not extend the data to fit Covid-19 period in the identification of ‘contagion’. While the identification of ‘contagion’ during Covid-19 is not a major concern for this paper, as we have identified the dynamics in excessively contagious markets remaining consistent for decades, it might present a scope for a future study to investigate this issue.

References

Acemoglu D, Ozdaglar A, Tahbaz-Salehi A (2015) Systemic risk and stability in financial networks. Am Econ Rev 105:564–608

Acharya V, Bisin A (2014) Counterparty risk externality: centralized versus over-the-counter markets. J Econ Theory 149:153–182

Adrian T, Shin HS (2009) The shadow banking system: implications for financial regulation. FRB of New York Staff Report 382

AFMEA (2017) Annual review 2017. Association of Financial Markets in Europe

Akhtaruzzaman MD, Boubaker S, Sensoy A (2021) Financial contagion during Covid-19 crisis. Financ Res Lett 38:101604

Allen F, Carletti E (2006) Credit risk transfer and contagion. J Monet Econ 53:89–111

Allen F, Gale D (1998) Optimal financial crises. J Financ 53:1245–1284

Allen F, Gale D (2000) Financial contagion. J Polit Econ 108:1–33

Atsalakis GS, Valavanis KP (2009) Surveying stock market forecasting techniques-part II: soft computing methods. Expert Syst Appl 36:5932–5941

Bakoush M, Gerding EH, Wolfe S (2019) Margin requirements and systemic liquidity risk. J Int Financ Markets Inst Money 58:78–95

Bank for International Settlements (2018) 88st Annual report: June 2018. Bank for International Settlements

Bates DS et al (2019) How crashes develop: intradaily volatility and crash evolution. J Finance 74:193–238

Battaglia F, Gallo A, Mazzuca M (2014) Securitized banking and the euro financial crisis: evidence from the Italian banks risk-taking. J Econ Bus 76:85–100

Battiston S, Puliga M, Kaushik R, Tasca P, Caldarelli G (2012) Debtrank: too central to fail? Financial networks, the fed and systemic risk. Sci Rep 2:541

Baur D, Schulze N (2005) Coexceedances in financial markets—a quantile regression analysis of contagion. Emerg Mark Rev 6:21–43

Bekaert G, Harvey CR, Lundblad CT, Siegel S (2013) The European union, the Euro, and equity market integration. J Financ Econ 109:583–603

Belo F, Collin-Dufresne P, Robert GS (2015) Dividend dynamics and the term structure of dividend strips. J Financ 70:1115–1160

Benoit S, Colliard JE, Hurlin C, Pérignon C (2017) Where the risks lie: a survey on systemic risk. Rev Finance 21:109–152

Billio M, Pelizzon L (2003) Contagion and interdependence in stock markets: have they been misdiagnosed? J Econ Bus 55:405–426

Billio M, Getmansky M, Lo AW, Pelizzon L (2012) Econometric measures of connectedness and systemic risk in the finance and insurance sectors. J Financ Econ 104:535–559

BIS (1998) 68th annual report. Bank for International Settlements 1998 CH-4002 Basle, Switzerland. http://www.bis.org

Bisias D, Flood M, Lo AW, Valavanis S (2012) A survey of systemic risk analytics. Annu Rev Financ Econ 4:255–296

Bratis T, Laopodis NT, Kouretas GP (2020) Systemic risk and financial stability dynamics during the eurozone debt crisis. J Financ Stab 47:100723

Brown SJ, Warner JB (1985) Using daily stock returns: the case of event studies. J Financ Econ 14:3–31

Brunnermeier MK, Garicano L, Lane PR, Pagano M, Reis R, Santos T, Thesmar D, Van Nieuwerburgh S, Vayanos D (2016) The Sovereign-bank diabolic loop and esbies. Am Econ Rev 106:508–12

Cheng E (2017) People and companies are piling on debt at level last seen just before the financial crisis, according to the imf. https://www.cnbc.com/2017/10/11/non-bank-leverage-surpasses-pre-financial-crisis-high-imf-warns.html

Chinazzi M, Fagiolo G (2015) Systemic risk, contagion, and financial networks: a survey. Working Paper Series, 2013/08. Institute of Economics, Scuola Superiore Sant’Anna, Laboratory of Economics and Management (LEM)

Cont R (2001) Empirical properties of asset returns: stylized facts and statistical issues. Quant Finance 1:223–236

Corhay A, Rad AT (1994) Statistical properties of daily returns: evidence from European stock markets. J Bus Finance Account 21:271–282

Covitz D, Liang N, Suarez G (2009) The anatomy of a financial crisis: the evolution of panic-driven runs in the asset-backed commercial paper market. Finance and Economics Discussion Series Working Paper 36

Darolles S, Gourieroux C (2015) Contagion phenomena with applications in finance. Elsevier, Amsterdam

Demirer M, Diebold FX, Liu L, Yilmaz K (2018) Estimating global bank network connectedness. J Appl Econ 33:1–15

Demirer M, Gokcen U, Yilmaz K et al (2018b) Financial sector volatility connectedness and equity returns. Technical Report 1803. Koc University-TUSIAD Economic Research Forum

Diamond DW, Raghuram RG (2011) Fear of fire sales, illiquidity seeking, and credit freezes. Q J Econ 126:557–591

Diebold FX, Liu L, Yilmaz K (2017) Commodity connectedness. Technical report. National Bureau of Economic Research

Diebold FX, Yilmaz K (2009) Measuring financial asset return and volatility spillovers, with application to global equity markets. Econ J 119:158–171

Diebold FX, Yilmaz K (2012) Better to give than to receive: predictive directional measurement of volatility spillovers. Int J Forecast 28:57–66

Diebold FX, Yilmaz K (2014) On the network topology of variance decompositions: measuring the connectedness of financial firms. J Econ 182(1):119–134

Diebold FX, Yilmaz K (2015) Financial and macroeconomic connectedness: a network approach to measurement and monitoring. Oxford University Press, New York

Duffie D, Eckner A, Horel G, Saita L (2009) Frailty correlated default. J Financ 64:2089–2123

Dungey MH, Harvey J, Siklos PL, Volkov V (2017a) Signed spillover effects building on historical decompositions. UTAS Working Paper

Dungey M, Gajurel D (2015) Contagion and banking crisis-international evidence for 2007–2009. J Bank Finance 60:271–283

Dungey M, Renault E (2018) Identifying contagion. J Appl Economet 33:227–250

Dungey M, Matei M, Luciani M, Veredas D (2017) Surfing through the GFC: systemic risk in Australia. Econ Rec 93:1–19

Dungey M, Harvey J, Volkov V (2019) The changing international network of sovereign debt and financial institutions. J Int Financ Markets Inst Money 60:149–168

Dungey M, Islam R, Volkov V (2020) Crisis transmission: visualizing vulnerability. Pac Basin Financ J 59:101255

ECB (2009) Annual report 2009. European Central Bank

Elliott L (2017) Imf warns China over ‘dangerous’ growth in debt. https://www.theguardian.com/business/2017/aug/15/imf-warns-china-debt-slowdown-financial-crisis

Elliott M, Golub B, Jackson MO (2014) Financial networks and contagion. Am Econ Rev 104:3115–53

Engle R (2018) Systemic risk 10 years later. Annu Rev Financ Econ 10:125–152

Eugene FF (1976) Foundations of finance: portfolio decisions and securities prices. Basic Books (AZ)

Fama EF, French KR (1988) Permanent and temporary components of stock prices. J Polit Econ 96:246–273

Farhi E, Tirole J (2017) Deadly embrace: Sovereign and financial balance sheets doom loops. Rev Econ Stud 85:1781–1823

Fernández-Rodríguez F, Gómez-Puig M, Sosvilla-Rivero S (2016) Using connectedness analysis to assess financial stress transmission in emu Sovereign bond market volatility. J Int Finan Markets Inst Money 43:126–145

Field P (2003) Modern risk management: a history. Risk Books

Forbes KJ, Rigobon R (2002) No contagion, only interdependence: measuring stock market comovements. J Financ 57:2223–2261

Friedman G (2016) The export crisis: the 10 worst hit countries and the 5 most at risk. https://geopoliticalfutures.com/the-export-crisis-the-10-worst-hit-countries-and-the-5-most-at-risk/

Fry-McKibbin R, Hsiao CYL, Martin VL (2021) Measuring financial interdependence in asset markets with an application to eurozone equities. J Bank Finance 122:105985

Gai P, Kapadia S (2010) Contagion in financial networks. Proc R Soc A Math Phys Eng Sci 466:2401–2423

Georg CP (2013) The effect of the interbank network structure on contagion and common shocks. J Bank Finance 37:2216–2228

Gorton G, Metrick A (2012) Securitized banking and the run on repo. J Financ Econ 104:425–451

Haldane AG (2013) Rethinking the financial network. In: Fragile stabilität–stabile fragilität. Springer, pp 243–278

Hanson SG, Kashyap AK, Stein JC (2011) A macroprudential approach to financial regulation. J Econ Perspect 25:3–28

Holmstrom B, Tirole J (1996) Modeling aggregate liquidity. Am Econ Rev 86:187–191

Holmstrom B, Tirole J (1997) Financial intermediation, loanable funds, and the real sector. Q J Econ 112:663–691

Jolly D, Bradsher K (2015) Greece’s debt crisis sends stocks falling around the globe. https://www.nytimes.com/2015/06/30/business/international/daily-stock-market-activity.html

Joseph K, Wintoki BM, Zhang Z (2011) Forecasting abnormal stock returns and trading volume using investor sentiment: evidence from online search. Int J Forecast 27:1116–1127

Joseph A, Turner C, Jeremiah R (2016) Comparative analyses of stock returns properties and predictability. Proc Comput Sci 95:272–280

Joseph A, Larrain M, Turner C (2017) Daily stock returns characteristics and forecastability. Proc Comput Sci 114:481–490

Joseph A, Larrain M (2008) Relative performance of neural networks on standard and poor’s 500 index prediction of aggregate sales. In: Intelligent engineering systems through artificial neural networks, vol 8. ASME Press

Khan S, Park KKW (2009) Contagion in the stock markets: the Asian financial crisis revisited. J Asian Econ 20:561–569

Khandani AE, Andrew WL (2011) What happened to the quants in august 2007? Evidence from factors and transactions data. J Financ Mark 14:1–46

Khandani AE, Lo AW, Merton RC (2013) Systemic risk and the refinancing ratchet effect. J Financ Econ 108:29–45

Kim MJ, Nelson CR, Startz R (1991) Mean reversion in stock prices? A reappraisal of the empirical evidence. Rev Econ Stud 58:515–528

Kindleberger CP (1978) Manias, panics and crashes: a history of financial crises. Springer, Berlin

King M, Sentana E, Wadhwani S (1994) Volatility and links between national stock markets. Econometrica 62:32

Kiyotaki N, Moore J (1997) Credit cycles. J Polit Econ 105:211–248

Koop G, Pesaran MH, Potter SM (1996) Impulse response analysis in nonlinear multivariate models. J Econom 74:119–147

Kremer M, Schäfer R (2016) Impact of nonstationarity on estimating and modeling empirical copulas of daily stock returns. J Risk 19

Krishnamurthy A, Tyler M (2017) How credit cycles across a financial crisis. Technical report. National Bureau of Economic Research

Ladley D (2013) Contagion and risk-sharing on the inter-bank market. J Econ Dyn Control 37:1384–1400

Liang Y (2016) Shadow banking in china: implications for financial stability and macroeconomic rebalancing. Chin Econ 49:148–160

Longin FM (1996) The asymptotic distribution of extreme stock market returns. J Bus 383–408

Longstaff FA, Wang J (2012) Asset pricing and the credit market. Rev Financ Stud 25:3169–3215

Lucey BM, Voronkova S (2008) Russian equity market linkages before and after the 1998 crisis: evidence from stochastic and regime-switching cointegration tests. J Int Money Financ 27:1303–1324

Mao D (2009) Macroeconomic situations and policy adjustments in china. Int J Bus Manag 4:97

Masson PR (1998) Contagion: monsoonal effects, spillovers, and jumps between multiple equilibria. International Monetary Fund

Mauldin J (2017) China’s growth driven by shadow banking is a potential trigger for the next global recession. http://www.mauldineconomics.com/editorial/chinas-growth-driven-by-shadow-banking-is-a-potential-trigger-for-the-next